Multilatinas are companies of Latin American origin that engage in foreign direct investment (FDI). There is no single well-recognised and readily available source to facilitate an in-depth quantitative analysis of the internationalisation strategies of multilatinas. In fact, the difficulty in identifying this class of companies is probably the main reason why our current understanding of the internationalisation strategies of multilatinas is based predominantly on case studies. This chapter describes how we identified the multilatinas discussed in this book and uncovered their internationalisation strategies.

Identifying multilatinas

We relied on several existing rankings of Latin American companies to identify the location of the key decision-makers in the process of internationalisation, including: the 500 largest Latin American companies in 2009 and 2010; the most global Latin American multinationals (LAMNEs) in 2012; the 500 largest Chilean companies in 2011, selected by AméricaEconomíaFootnote 1; the 500 most important Mexican companies in 2011 from the CNN magazine Expansion; and the 1,000 largest Colombian companies in 2012 from Semana. Fundação Dom Cabral publishes a ranking of Brazilian multinationals; however, the majority of the companies appear in the AméricaEconomía ranking, so the added value of this source was only modest. AméricaEconomía also publishes a ranking of Peruvian companies, but an exhaustive review of this ranking in 2012 showed that the participation of Peruvian companies in FDI is very limited. All of these sources draw heavily on information available from the companies’ websites, from the financial supervisory bodies of different Latin American countries and from surveys of executives.

We inspected these pooled data to identify Latin American Multinational Enterprises. Our approach has an obvious bias towards identifying large multilatinas and does not include micro-multinationals and Latin American born-global companies. In fact, we excluded all companies with sales less than US$100 million. This threshold is significant because traditionally companies with sales volumes of this magnitude have the resources necessary to make direct investments in foreign markets.Footnote 2 Although it has recently been recognised that firms with small national markets have incentives to become international very fast, because of the small scale and lower domestic opportunities,Footnote 3 empirical evidence suggests that these firms do not engage in FDI but rely on specialised international networks instead.Footnote 4 For example, exporting and leveraging independent intermediaries helps Latin American born-global companies international operations become flexible without paying the cost of direct investments abroad. Therefore, we expect only a small number of multilatinas – that is, companies that use FDI in their overseas operations – to fall outside the selected pool of companies.

Our next step was to reject companies that were subsidiaries of firms from outside Latin America, companies that had only domestic operations and businesses in the insurance and banking industries, which are highly regulated and subject to considerable restrictions regarding internationalisation. We also discarded purely state-owned enterprises (SOEs) that were not publicly traded, on the assumption that their internationalisation process would obey not only a market but also and mainly a political logic. The behaviour of SOEs frequently responds to political pressures that make comparisons with the internationalisation strategies of other companies questionable. However, at this stage we retained Petrobras, Ecopetrol and Grupo ISA in our sample because they were publicly traded SOEs. The 2015 corruption scandal at Petrobras illustrates vividly the risks of this approach. The sophisticated scheme of interdependencies and transfers in which Petrobras was involved and which benefitted individuals and political parties, worsened the economic crisis in Brazil and undermined the international credibility of the country while stigmatising one of the champion multilatinas. As SOEs, the uniqueness of Petrobras, Ecopetrol and Grupo ISA stands out in many aspects of their operations, including their internationalisation strategy, so much so that their exclusion would have hampered our overall understanding of the internationalisation strategy of multilatinas. Ecopetrol was the only Colombian multinational company in the Fortune Global 500 list in 2015, in which Petrobras ranked twenty-eighth.

The resulting pool of companies was revised and double-counted entities were eliminated, to arrive at 247 firms. Because business groups are a pervasive organisational form in emerging economies,Footnote 5 we had to examine ownership relationships among these 247 multilatinas. Using Standard and Poor’s (S&P) and Reuters’ databases and the firms’ websites, we identified 71 conglomerates or headquarters of business groups, 57 subsidiaries of other Latin American companies and 125 standalone enterprises. We classified firms as conglomerates if S&P or Reuters described their economic activity as ‘business conglomerate or holding’, they presented themselves as a business group on their website, or they had several clearly identifiable affiliate companies. Firms were classified as ‘subsidiaries’ if S&P and Reuters identified them as such or their website indicated that they were controlled by another Latin American company.

We subsequently eliminated fourteen conglomerate headquarters whose subsidiaries were already included in the list: CGE, Empresas COPEC, Femsa, Grupo Alfa, Grupo Bal, Grupo Camargo Correa, Grupo Carso, Grupo Casa Saba, Grupo Elektra, Grupo Salinas, Grupo Xignux, Norberto Odebrecht, Techint and Vale. This decision was made for two reasons: (1) a parent and a subsidiary share important features, especially resources; and (2) the international business literature suggests that subsidiaries’ behaviour reflects the business group’s strategy;Footnote 6 and we therefore risked double-counting some companies as their strategic decision-making processes overlapped. We also omitted six conglomerate headquarters that were in essence pure holdingsFootnote 7 and whose only economic activity, described by S&P, was to provide administrative and financial support to members of the group without being involved in strategic decision-making.

We expect the firms that are part of a conglomerate and the stand-alone firms in our sample to be largely comparable even when they have a distinct resource base. Conglomerates, like independent firms, are characterised by unitary management and administrative coordination. In independent firms, the unitary management is in the hands of the general manager, who defines strategies and supervises the different business activities of the company. In business groups, unitary management is possible because the responsibility for defining long-term strategies and control, in the form of monitoring and supervising any affiliated companies, are in the hands of the managers of the parent company or the owner in the case of a family group. Also, in a business group, the parent company coordinates the administrative function of any subsidiaries to achieve mutual adjustments and (ideally) synergies in planning and decision-making, standardise processes and procedures and exert direct supervision over subsidiaries – much like a general manager does in an independent firm.

The decisions made about internationalisation by stand-alone firms and business groups are also comparable in terms of their purpose and the role played by resources. Decisions about internationalisation are made to improve the position of the group as a whole as well as improving the competitive position of individual entities. As for resources, internationalisation decisions are comparable because for both firms and groups they are related to the resources that control viable business operations abroad or are required for creating them. That said, we acknowledge that business groups and their affiliates share resources that might not be available for standalone firms, such as internal capital markets, for example, which can provide the financial resources to invest abroad.Footnote 8 Table 1.1 summarises the process of identifying the companies for this study.

Table 1.1 Summary of the process of identification of multilatinas

| Ranking source of data | Firms in the ranking | Step 1 | Step 2 | Step 3 | Step 4 | Step 5 | Steep 6 | Step 7 | Step 8 | Final sample |

|---|---|---|---|---|---|---|---|---|---|---|

| 500 largest LACs (2009 to 2010) | 583 | 0 | 218 | 161 | 0 | 41 | 0 | 12 | 5 | 144 |

| 65 Most global Latin American companies (2012) | 65 | 0 | 0 | 0 | 0 | 1 | 54 | 2 | 1 | 9 |

| 500 largest Mexican firms (2011) | 500 | 0 | 219 | 131 | 76 | 1 | 49 | 0 | 0 | 24 |

| 500 largest Chilean firms (2011) | 500 | 102 | 75 | 220 | 41 | 0 | 32 | 0 | 0 | 30 |

| 1,000 largest Colombian firms (2012) | 1000 | 582 | 234 | 147 | 8 | 0 | 9 | 0 | 0 | 20 |

| Final multilatina population | 226 |

A group of nineteen firms included in the initial list of companies shared a parent company with other firms in the sample. In these cases, we decided to retain the firms if each subsidiary belonged to a different industry.Footnote 9 We made this decision because empirical evidence has shown that although firms share some resources within a business group, each also has a unique set of resources that it uses to achieve its business purposes.Footnote 10 These differences naturally tend to be larger when entities within a business group belong to unrelated industries. When the process of selection was complete, we had a list of 226 multilatinas, full details of which, including their industries and country of origin, are shown in Table 1.2.

Table 1.2 The population of multilatinas

Unit of analysis

Our unit of analysis is the most recent foreign investment project undertaken by the Latin American multinationals in a foreign country. We chose this unit of analysis because it is at the transaction level that internal organisational resources and competences and contextual variables, such as the interaction between home and host country institutional factors, shape firms’ strategies abroad.Footnote 11 We purposefully and explicitly invited the executives surveyed for this study to answer questions about their most recent approach to internationalisation in relation to their companies’ most recent project involving FDI.

By using this unit of analysis we aimed to diminish recall bias and rely on managers remembering recent experiences more vividly and easily than older ones.Footnote 12 We also aimed to reduce the confusion of respondents when responding to specific quantitative questions about the process of making foreign direct investments.

Strategising about internationalisation

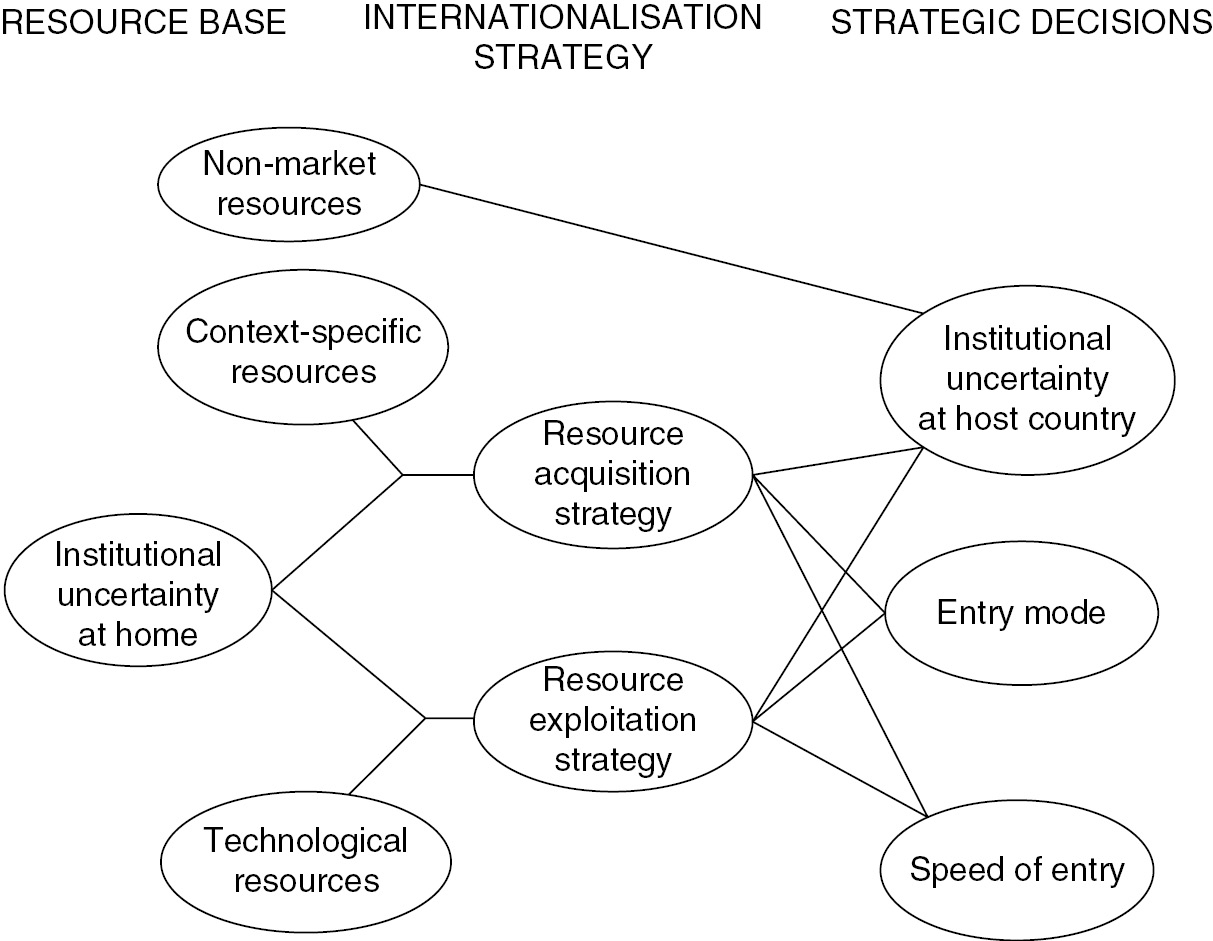

We built a unique dataset to explore the conceptual model of strategic decision-making represented in Figure 1.1. According to this framework, the internationalisation strategy of multilatinas cannot be understood without identifying the most important resources on which their competitive position at home is built.

Figure 1.1 Conceptual model of strategic internationalisation decision- making.

Resources

We adopted a wide definition of resources that includes all assets, capabilities, organisational processes, firm attributes, information, knowledge, and so on, that a firm controls and that allow it to conceive and implement strategies in foreign markets.Footnote 13 Resources can be of two types: market or non-market.Footnote 14 Market resources are those that firms use to compete against each other in the market; they include efficient production facilities, brand names and product innovations. Non-market resources are the tangible and intangible assets firms develop that allow them to manage the formal and informal institutions that surround their business activities in the home country (for example, the exchange of favours and bribes).

Additionally, for the purposes of this research, we classified market resources as either technological or context-specific. Transferable technological resources are knowledge-intensive resourcesFootnote 15 that allow firms to create superior products, improve existing products and gain effectiveness and efficiency in production processes. Examples of these resources are R&D, patents and advanced production technologies. Context-specific resources, on the other hand, are developed by firms to fit their country-of-origin markets; their benefits, as a source of competitive advantage, are restricted to a specific country or a region.Footnote 16 Examples of these resources are business networks, brands and managerial market knowledge. The value of organisational resources is determined by the institutional environment in the home country, and this contextual element determines many of the differences between developed country multinationals and multilatinas.

Institutional uncertainty

We define institutions as the formal and informal rules of the game for doing business inside the borders of a specific country.Footnote 17 The institutional weakness of emerging countries, such as those in Latin America, is manifested in many characteristics of governance, including weak legal systems to protect intellectual property rights,Footnote 18 political instability,Footnote 19 risk of intervention by the home government through taxation, pricing, exchange rates, production and ownership requirements,Footnote 20 or corruption and abuse (or misuse) of public power for private benefit.Footnote 21 While these characteristics of a weak institutional context tend to be more or less acute in all emerging countries, the institutional uncertainty is particularly damaging for business transactions. These institutional weaknesses interact with the unique resources and core competences of multilatinas to shape their internationalisation strategies.

Strategies

By ‘strategies’ we mean firms’ attempts to identify, protect and exploit their unique resources in order to gain a competitive advantage in the marketplace.Footnote 22 Following this definition, and considering the relationship between institutional uncertainty in the home country and firms’ resources, we expect multilatinas to follow predominantly one of two generic internationalisation strategies: resource exploitation, which uses the firm’s home-grown resources in its foreign markets to create competitive advantage;Footnote 23 and resource acquisition, which broadens the resource base of the firm through foreign investments in new resources and competences.Footnote 24 Each of these strategies gives rise to a specific set of strategic decisions that affect the where, when and how of internationalisation.

Strategic decisions

Internationalisation obliges firms to make at least three strategic decisions: choose a host market, select an entry mode, and determine the speed of investment.Footnote 25 Market choice refers to the selection of a foreign country in which to invest. Entry mode refers to the choice of greenfield investment, mergers, acquisitions or joint ventures as a contractual or organisational arrangement for operating abroad.Footnote 26 Speed of investment refers to how quickly organisations execute a plan for FDI, from initial consideration of alternatives to the commitment of resources abroad.Footnote 27

Data collection

Data collection consisted of a telephone interview based on a structured questionnaire. All invited respondents fell into one of the following categories: vice-president of corporate planning, financial chief or chief of international operations, and respondents were identified in specialised databases such as Standard & Poor’s, Reuters and Bloomberg. A cover letter and questionnaire written in Spanish and Portuguese were sent via email to the key informants. In the following four months, market researchers, all Spanish and Portuguese native speakers, contacted the selected respondents or their assistants by phone and made appointments for the interviews. We received responses from sixty-two executives, one per company. The far-right column in Table 1.2 identifies the participating companies. In seven of the questionnaires returned, data relating to the speed of undertaking FDI were incomplete. These questionnaires noted only the year in which firms identified investment opportunities or started legal procedures in the host market to prepare for investment. In these cases, we took a conservative approach and assumed January as the month in which the opportunity was discovered or the legal procedures began. Additionally, some of the aspects about which we would ideally have liked information could not be fully explored because fewer than 60% of the respondents provided valid answers. Areas for which we could not access information with enough detail include aspects of ownership structure, drivers of perceived competition in the domestic market, business unit sales of the previous year and ownership participation in joint venture agreements.

Characteristics of the sample

Of the sixty-two participating multilatinas, forty-seven reported that they were entering a new host market. The participating companies belong to twenty-four industrial sectors, of which 30% are Brazilian multinationals, followed in frequency by Mexican, Colombian and Chilean. The sample consists of large multilatinas of which seven have more than 20,000 employees. Table 1.3 presents a detailed description of the data.

Characteristics of the multilatinas sample

| Frequency | % | |

|---|---|---|

| a. Number of firms that invest in a new host country | ||

| New | 45 | 72.6 |

| Old (reinvesting) | 17 | 27.4 |

| Total | 62 | 100 |

b. Country of origin of firms in the sample

| Origen country | Frequency | % |

|---|---|---|

| Argentina | 4 | 6.5 |

| Brazil | 19 | 30.6 |

| Chile | 10 | 16.1 |

| Colombia | 12 | 19.4 |

| Mexico | 15 | 24.2 |

| Peru | 2 | 3.2 |

| Total | 62 | 100 |

c. Age of the firms in the sample

| Age | Frequency | % |

|---|---|---|

| < 20 years | 7 | 11.3 |

| > 20 < 40 | 9 | 14.5 |

| > 40 < 60 | 17 | 27.4 |

| > 60 < 80 | 14 | 22.6 |

| > 80 < 100 | 7 | 11.3 |

| > 100 years | 8 | 12.9 |

| Total | 62 | 100 |

d. Size of the firms in the sample

| Number of employees | Frequency | % |

|---|---|---|

| < 5,000 | 36 | 58.06 |

| > 5,000 < 20,000 | 19 | 30.65 |

| > 20,000 | 7 | 11.29 |

| Total | 62 | 100 |

e. Economic activities of the firms in the sample

| Economic activity | Frequency |

|---|---|

| Aerospace | 1 |

| Agroindustry | 5 |

| Aqua farming | 1 |

| Automotive | 5 |

| Beverages | 1 |

| Cellulose/paper | 2 |

| Cement | 1 |

| Chemical | 2 |

| Construction | 1 |

| Electronics | 2 |

| Energy | 1 |

| Entertainment | 2 |

| Food | 10 |

| Healthcare | 1 |

| Logistic and transport | 2 |

| Manufacturing | 2 |

| Mass media | 1 |

| Mining | 1 |

| Multisector | 3 |

| Oil and gas | 7 |

| Pharmaceutical | 3 |

| Retailer | 3 |

| Siderurgical | 3 |

| Technology | 2 |

The subsequent chapters of Part I of this book present the most critical macroeconomic, social and institutional aspects of Argentina, Brazil, Chile, Colombia, Mexico and Peru, as these are seen as indispensable for understanding the internationalisation strategies of the multilatinas featured in the book. The contextual analysis in these chapters is focused almost entirely on the period of 2000 to 2015, a time period that allows us to examine the environmental context immediately before the FDI process we studied and some years following it. The understanding of the macro environment is essential for the building of a holistic understanding of the internationalisation strategies of multilatinas. However, expanding the detailed description of the context beyond 2015 will introduce facts and forces that were not part of the decision-making consideration of multilatinas and will introduce a substantial cognitive bias in the interpretation of the results. The phone interviews, which revealed the internationalisation strategies of the multilatinas featured, took place between August 2012 and April 2013.