No CrossRef data available.

Article contents

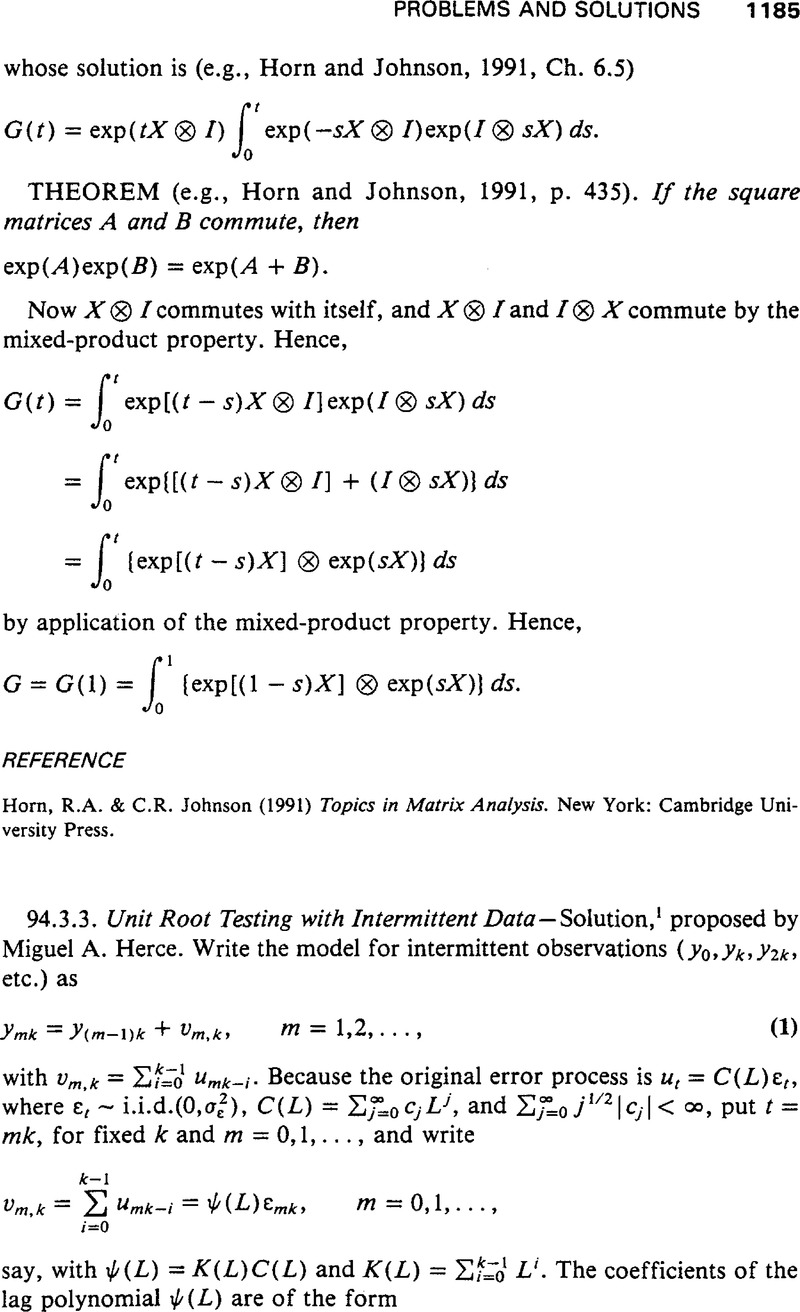

Unit Root Testing with Intermittent Data

Published online by Cambridge University Press: 11 February 2009

Abstract

An abstract is not available for this content so a preview has been provided. Please use the Get access link above for information on how to access this content.

- Type

- Solutions

- Information

- Copyright

- Copyright © Cambridge University Press 1995

References

REFERENCES

Andrews, D.K.W. & Monahan, J.C. (1992) An improved heteroskedasticity and autocorrelation consistent covariance matrix estimation. Econometrica 60, 953–966.CrossRefGoogle Scholar

Herrndorf, N. (1984) A functional central limit theorem for weakly dependent sequences of random variables. Annals of Probability 12, 141–153.CrossRefGoogle Scholar

Newey, W.K. & West, K.D. (1987) A simple positive definite heteroskedasticity and autocorrelation consistent covariance matrix estimator. Econometrica 55, 703–708.CrossRefGoogle Scholar

Phillips, P.C.B. (1987) Time series regression with a unit root. Econometrica 55, 277–301.CrossRefGoogle Scholar