INTRODUCTION

Technology innovation, the source of competitive advantage, enhances profitability (Bayus, Erickson, & Jacobson, Reference Bayus, Erickson and Jacobson2003) and spurs the growth (Cho & Pucik, Reference Cho and Pucik2005) of firms. Understanding the impact of the institutional environment on firm innovative performance could benefit firms in forming innovative strategy and building competitive advantage. However, research about the comprehensive impact of formal and informal institutions on firm innovative performance is limited. Existing research about the influence of the institutional environment on innovation mainly focuses on the macro level, examining how national or regional institutional systems shape the innovativeness of firms within that particular territory (Augier, Guo, & Rowen, Reference Augier, Guo and Rowen2016; Laursen, Masciarelli, & Prencipe, Reference Laursen, Masciarelli and Prencipe2012). While a number of recent studies investigate the impact of specific institutional factors on firms’ innovative strategy and performance, they mainly focus on formal institutions (e.g., Barasa, Knoben, Vermeulen, Kimuyu, & Kinyanjui, Reference Barasa, Knoben, Vermeulen, Kimuyu and Kinyanjui2017; Luo & Wang, Reference Luo and Wang2011; Zhu, Wittmann, & Peng, Reference Zhu, Wittmann and Peng2012). Informal institutions such as bribery and informal financing are less studied in the literature. Moreover, while this stream of literature tends to emphasize the moderating effects of institutions (Mueller, Rosenbusch, & Bausch, Reference Mueller, Rosenbusch and Bausch2013), it should be noted that institutions are not merely the background – they can exert direct influence on firm strategy and performance (Peng, Li, Pinkham, & Chen, Reference Peng, Li, Pinkham and Chen2009). Yet, the knowledge of such direct impact is still lacking.

To address the aforementioned gaps, and to respond to the call for bringing institutions to the fore in the innovation literature (Lu, Tsang, & Peng, Reference Lu, Tsang and Peng2008), our study explores the impact of both formal and informal institutions, independently and jointly, on firms’ innovation decision making and innovator type tendency. Different from previous research's focus on macro-level institutional environments, we emphasize firm-level heterogeneity in perception and experience of formal and informal institutions. Specifically, we analyze how and why particular formal and informal institutions perceived and/or experienced by firms can serve to potentially stimulate and/or constrain a firm's decision and efforts to innovate.

To capture the impact of formal institutions, following the tradition of new institutional economics, we examine the governmental system, the legal system, and formal financial institutions (Cui, Reference Cui2016; North, Reference North1990). We argue that all these formal institutions will affect the likelihood that a firm will become a certain type of innovator. Formal institutions exert such influence through shaping the costs and benefits of innovation and the allocation of critical resources that firms need for their innovative activities (Cheng & Huang, Reference Cheng, Huang, Lewin, Murmann and Kenney2016; van Waarden, Reference van Waarden2001). While previous research mainly suggests that formal institutional constraints will hinder firm innovation, we argue that some institutions that are commonly perceived as obstacles to firms’ general operation and development can indeed stimulate firms to innovate more so as to increase their competitive advantage.

To capture the impact of informal institutions, we investigate bribery in business practice and informal financial institutions. We suggest that informal financial institutions have a similar impact as formal financial institutions on firms’ innovation decisions and innovator type tendency. In contrast, we argue that the impact of bribery on firms’ innovation decisions and performance is complex; while pervasive bribery reduces firms’ incentive to invest in innovative activities, paying bribes can help firms in extracting value from existing resources and activities to more effectively transform their innovation input into output.

We further investigate the joint influence of formal and informal institutions on firm innovation decisions and innovator type tendency. Research addressing different institutional forces has acknowledged the importance and challenges of establishing whether the joint impact of formal and informal institutions on organizational outcomes is likely to be complementary or substitutive (Ang, Benischke, & Doh, Reference Ang, Benischke and Doh2015; Cui, Reference Cui2016; Horak & Restel, Reference Horak and Restel2016; North, Reference North1990). In our study, we explicitly examine such joint effects on firm innovation efforts and performance. We argue that the joint effects of formal and informal institutions can be either complementary or substitutive depending upon firms’ tendency to become certain types of innovators.

Our article has at least three major contributions. First, it enriches institutional theory and innovation research by establishing a framework that encompasses multidimensional, formal, and informal institutional forces, with a focus on their independent and joint impacts on firms’ innovation decisions and performance. Second, it addresses firms’ heterogeneity in their perception and experience of various institutions. This perspective allows us to disentangle the complex impact of different institutional forces at the firm level, and thus obtain a more fine-grained understanding of institutional impact. Third, we develop more comprehensive measures of firm innovation decisions and performance. We categorize firms into four types of innovators according to the combination of their innovation input and output. This typology of firms in terms of their innovation activities and performance allows us to consider innovation input and output simultaneously. It also enables us to systematically conceptualize the mechanism through which different formal and informal institutions perceived and/or experienced by firms influence firms’ tendency to eventually become a certain type of innovator.

China provides a suitable context to develop and test our hypotheses, given its complex and ever-evolving institutional environments (Zhang, Zhao, & Zhang, Reference Zhang, Zhao and Zhang2016). More importantly, we use World Bank's Enterprise Survey on Chinese private firms in 2012 as our data source. The institutional context of China in 2012 is particularly appropriate for our study. From the beginning of the 11th Five Year Plan in 2006, China has made innovation a national policy, as indicated by the promulgation of the ‘Outline of the National Plan for Medium – and Long-term Scientific and Technological Development (2006–2020)’ by the State Council. Since then, China's R&D expenditures have been growing at a compound annual rate of about 20 percent (Lewin, Kenney, & Murmann, Reference Lewin, Kenney, Murmann, Lewin, Murmann and Kenney2016; World Bank & Development Research Center of the State Council P. R. C., 2013). The number of Chinese patents granted by domestic and international patent offices has also increased remarkably since then (Cheng & Huang, Reference Cheng, Huang, Lewin, Murmann and Kenney2016). 2012 is the second year of the 12th Five Year Plan, during which time period Chinese private enterprises were active in innovation activities (Lewin et al., Reference Chiu, Liou, Kwan, Lewin, Murmann and Kenney2016). The national, provincial, and even city-level governments have also been actively involved in providing support to firm innovation. Despite the efforts, many scholars found that China's institutions are still not well-developed enough to provide incentives for firms to pursue effective innovation (Cheng & Huang, Reference Cheng, Huang, Lewin, Murmann and Kenney2016; Fuller, Reference Fuller, Lewin, Murmann and Kenney2016a; Redding, Reference Redding, Lewin, Murmann and Kenney2016). However, much of the existing literature neglects firm heterogeneity in the perceived and experienced institutional forces, with the exception of Fuller (Reference Fuller2016b), and mainly focuses on either formal institutions or informal institutions separately. Our article thus contributes to providing a comprehensive theoretical explanation and empirical analysis that explores the independent and joint effects of formal and informal institutions on firm innovation decisions and performance. The institutional context of China in 2012 allows us to probe the questions of which institutional factors will lead to firm innovation input, and under what conditions will the innovation input be effectively transformed into innovation output.

In the following sections we first develop our hypotheses and test them using a sample of 1207 Chinese manufacturing firms. Results of the empirical analysis will be presented in the subsequent section, followed by a discussion and conclusion.

THEORETICAL BACKGROUND AND HYPOTHESES DEVELOPMENT

Institutions, Innovation, and Types of Innovators

The new institutional economics (NIE) posits that institutions provide incentive structures that affect firms’ decision making through their cost-benefit calculation (North, Reference North1990). While stable, well-developed, and market-supportive institutions enable firms to develop competitive advantages, unstable and underdeveloped institutions can pose constraints on firm development. Institutional constraints are those ‘institutions and institutional enforcement mechanisms that cause or increase uncertainty, and thus costs, for firms in their economic activities’ (Meyer & Peng, Reference Meyer and Peng2016). Such constraints can come from formal and informal institutions. Formal institutional constraints include obstacles in governmental, legal, and financial systems, where government plays the dominant role in monitoring business activities, especially in emerging economy contexts (Meyer & Peng, Reference Meyer and Peng2016). Informal institutional constraints include obstacles in customs, values, norms of behaviors, and informal networks that create or increase costs for firms in certain economic activities (Horak & Restel, Reference Horak and Restel2016). According to NIE, organizational decisions and activities such as innovation are responses to the formal and informal institutional constraints facing organizations (North, Reference North1990, Reference North2005).

While the NIE approach primarily views institutions as constraints on firm behaviors and strategies, the extensive historical institutional and comparative capitalism tradition posits that national institutions not only constrain firm behavior and strategies but also provide resources and bolster specific firm-level capabilities that lead to institutional competitive advantage (Butzbach, Fuller, & Schnyder, Reference Butzbach, Fuller and Schnyder2020; Jackson & Deeg, Reference Jackson and Deeg2008; Whitley, Reference Whitley2007; Witt & Jackson, Reference Witt and Jackson2016). National institutions in the comparative capitalism approach shape the collective supply of input (e.g., skills, capital) for firms and establish the legitimate way in which such input should be used (Jackson & Deeg, Reference Jackson and Deeg2008, Reference Jackson and Deeg2019). These two approaches to institutions have both been adopted in the innovation literature (as discussed in the following paragraph). In this article, we follow the NIE approach in differentiating institutions into formal and informal ones but adopt a more balanced view of the impact of institutions on firm behaviors and strategies by acknowledging that some seeming institutional constraints may actually provide resources and capabilities for firms to establish their competitive advantages.

The innovation literature has extensively examined how institutions impact firm innovation. Most of them focus on macro-level institutions. Research in the comparative capitalism tradition investigates how national or regional institution shapes the innovativeness of firms within that particular territory (Augier et al., Reference Augier, Guo and Rowen2016; Cooke, Gomez Uranga, & Etxebarria, Reference Cooke, Gomez Uranga and Etxebarria1997; Redding, Reference Redding, Lewin, Murmann and Kenney2016). Studies following the NIE approach largely focus on formal institutions; scholars have found that better innovation performance of firms is associated with effective and transparent governmental systems, effectively enforced intellectual property rights protection systems, fair and effective legal systems, or mature and supportive formal financial systems in their regions or countries (Barasa et al., Reference Barasa, Knoben, Vermeulen, Kimuyu and Kinyanjui2017; Kwan & Chiu, Reference Kwan and Chiu2015; Shi & Wu, Reference Shi and Wu2017; Watkins, Papaioannou, Mugwagwa, & Kale, Reference Watkins, Papaioannou, Mugwagwa and Kale2015; Wu, Wang, Hong, Piperopoulos, & Zhuo, Reference Wu, Wang, Hong, Piperopoulos and Zhuo2016; Zhu et al., Reference Zhu, Wittmann and Peng2012). Research on the impact of informal institutions is still limited compared to those on formal institutions. This stream of literature has focused on societal trust (Brockman, Khurana, & Zhong, Reference Brockman, Khurana and Zhong2018; Redding, Reference Redding, Lewin, Murmann and Kenney2016), informal networks such as guanxi (Gao, Xu, & Yang, Reference Gao, Xu and Yang2008), and history (Liou, Kwan, & Chiu, Reference Liou, Kwan and Chiu2016), arguing that a low level of social trust, lack of managerial ties, and a historical memory of external threats are detrimental to firm innovation performance.

While previous studies have focused on macro-level institutional conditions, it is unlikely that individual firms are all the same in their perception and experience of different institutional forces. For instance, facing the same under-developed national financial institutions, firms with governmental ties or business ties may perceive and/or experience fewer constraints because they have better access to bank loans or venture capital than those that do not have such ties (Fuller, Reference Fuller, Lewin, Murmann and Kenney2016a). Therefore, it is important to address firm-level heterogeneity in their perceived and experienced institutional conditions when examining their influence on firm innovation.

Furthermore, informal institutions such as bribery norms in business practice and informal financing that prevail in many emerging economies are less studied in the literature. More importantly, although research has emphasized the importance of the joint effects of formal and informal institutions in shaping organizational behaviors and outcomes (Cui, Reference Cui2016; Horak & Restel, Reference Horak and Restel2016), there are still few studies that theoretically and empirically examine such joint impact.

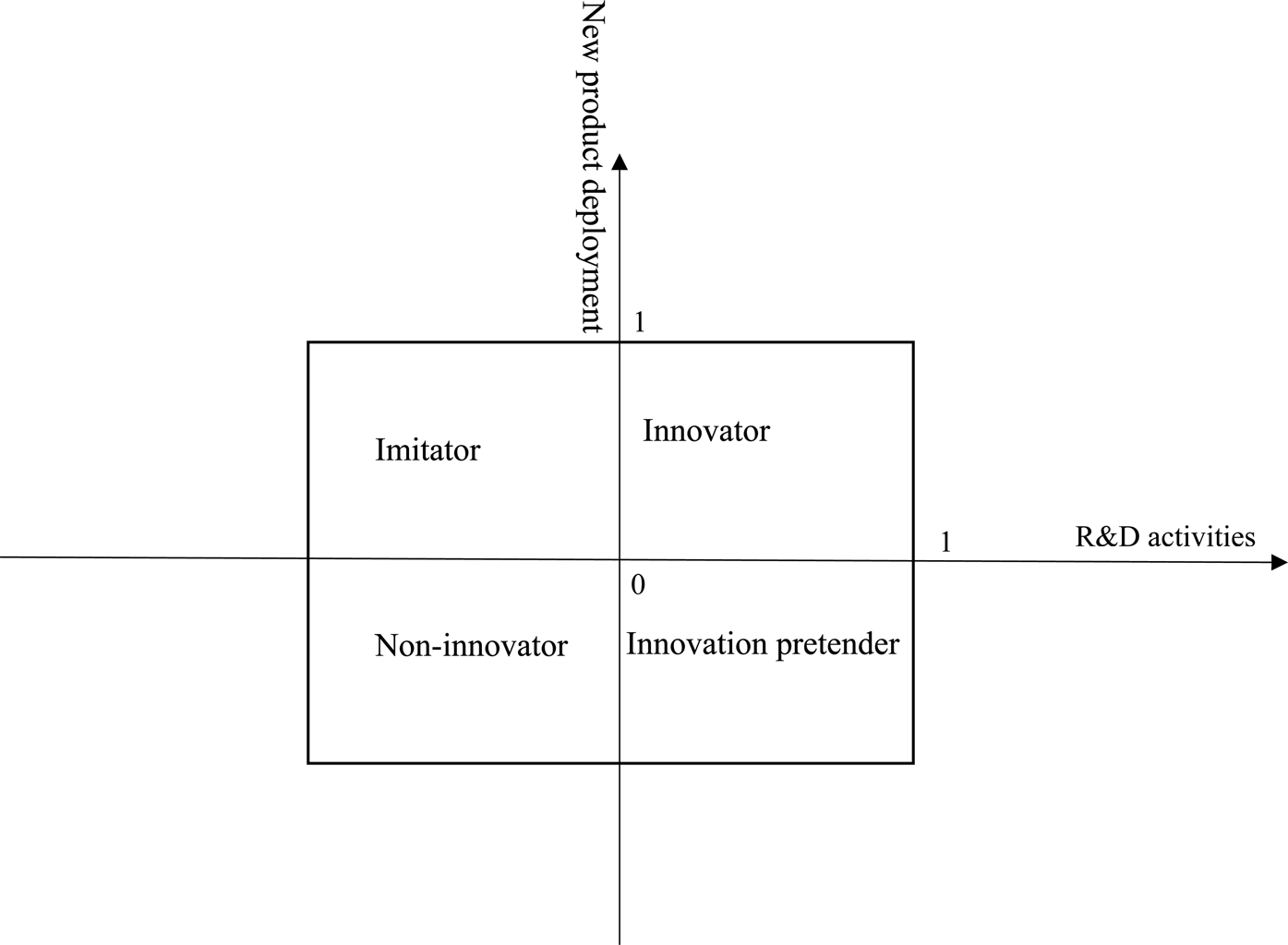

Our article aims to address the above-mentioned gaps by examining how firms’ perceived and/or experienced formal and informal institutions independently and jointly influence firm innovation decisions and performance. We categorize firms into four types of innovators according to the combination of their innovation input and output (Figure 1). We adopt R&D activities and new product deployment to represent firms’ innovation input and output respectively. New product deployment does not have to be innovative to the industry or to the world; it could be just new to the firm (Freel, Reference Freel.2003; Shinkle & McCann, Reference Shinkle and Mccann2014). Innovators are firms that both invest in R&D activities and deploy new products or services. Imitators are firms that produce new products or offer new services with limited-to-none R&D effort. Innovation pretenders are those firms making R&D effort but have not yet produced any new products or offered new services. Non-innovators have neither R&D investment nor new products or services. This categorization of firms enables us to further examine how institutions influence firms’ innovation input and output simultaneously. We argue that institutional factors have heterogeneous, independent, and joint impact on the propensity of firms to be different types of innovators.

Figure 1. Four types of innovator

Formal Institutions and Firm Innovation

In this section we examine firms’ perception of constraints from three formal institutions, namely, governmental, legal, and formal financial systems, in terms of their influence on firm innovation respectively. Government, as the foremost type of formal institution, establishes and enforces a set of regulatory framework, laws, and property rights (Fogel, Hawk, & Yeung, Reference Fogel, Hawk, Morck, Yeung, Basu, Casson, Wadeson and Yeung2006). Constraints from the governmental system include heavy tax burdens, low efficiency in administrative approval (Luo & Junkunc, Reference Luo and Junkunc2008), and governmental corruption (Doh, Rodriguez, Uhlenbruck, Collins, & Eden, Reference Doh, Rodriguez, Uhlenbruck, Collins and Eden2003). These activities can hinder firm growth (Aidis, Estrin, & Mickiewicz, Reference Aidis, Estrin and Mickiewicz2008) by increasing the cost of getting through the governmental administration process (Fogel & Zapalska, Reference Fogel and Zapalska2001; Geiger & Hoffman, Reference Geiger and Hoffman1998). However, while constraints from the governmental system could be obstacles to firms' general operations, they can also stimulate firms to invest more on innovation to compensate for the disadvantages generated by such constraints (Shinkle & McCann, Reference Shinkle and Mccann2014). Following existing literature, we examine three main aspects of governmental systems that will affect firm behavior. These aspects are taxation or tax burdens (tax rate and tax administration), administrative permits, and corruption. The efficiency, transparency, and accountability of the governmental systems are embedded in these aspects.

Tax burdens perceived by firms come from two main sources, one is high tax rate, and the other is a complex and opaque tax administration process. When managers of a firm perceive the tax rate imposed on them as burdensome, increasing the operation costs and impeding the firm's competitive advantage, they will be incentivized to allocate more firm revenues and resources to R&D activities. There are mainly two reasons for so doing. First, by investing in R&D activities, firms can report lower pre-tax profits (due to higher R&D expenses) and thus reduce the tax base. Moreover, as many governments in developing economies provide tax breaks to encourage innovation, investing in R&D for tax purposes is even more attractive to firms when they think that the tax rate is an obstacle to their business. For example, firms can enjoy a 150% tax deduction for their R&D investment in China (Dong & Gou, Reference Dong and Gou2010). R&D tax credits and other forms of R&D tax incentives in the US, Sweden, Canada, and the UK increase industrial R&D investment and innovation output (Czarnitzki, Hanel, & Rosa, Reference Czarnitzki, Hanel and Rosa2011; Dechezleprêtre, Einiö, Martin, Nguyen, & van Reenen, Reference Dechezleprêtre, Einiö, Martin, Nguyen and van Reenen2016; Mansfield, Reference Mansfield1986). Second, if firms perceive a high tax rate as an obstacle to their business development and their competitiveness in the market, they are more likely to turn to activities that contribute to their core competency so as to compensate for this institutional constraint. R&D activities are those activities contributing to firms’ long-term value creation and hence, competitive advantage.

In addition to a high tax rate, complicated procedure of tax administration is resource-consuming for firms (Ahlstrom & Bruton, Reference Ahlstrom and Bruton2010; Aidis & Adachi, Reference Aidis and Adachi2007). A heavy burden of tax administration, such as intensive governmental inspection and opaque, prolonged procedures will thus increase firms’ operation costs, reduce their profits, and will be detrimental to their competitiveness in the market. Therefore, if firms perceive that tax administration becomes a burden to their business development, they will be more likely to invest more in innovation activities to strengthen their core competencies and to overcome such a negative impact of the governmental system.

Low efficiency in administrative approval, such as granting government permits to conduct certain business activities, is another constraint in governmental systems that is time- and money-consuming for firms. The time and money spent in application procedures cost firms financial resources and potential business opportunities. If managers of a firm perceive that administrative procedures such as license applications become a severe obstacle to the firm's competitiveness, they will likely allocate more resources to activities such as R&D that can enhance the firm's competitive advantage.

The constraints from low efficiency and opaqueness in the administration process, such as tax administration and license approval, will be even worse if government corruption is prevalent. Prevalent government corruption implies that firms have to find guanxi and/or pay bribes to government officials to navigate complex and inefficient administration processes (Estrin & Prevezer, Reference Estrin and Prevezer2011), obtain government services more quickly (Paunov, Reference Paunov2016), or gain access to government research and development subsidies (Xie, Qi, & Zhu, Reference Xie, Qi and Zhu2018). All these activities generate extra burdens on firms in their business operations. Moreover, given the illegal nature of corruption, paying bribes to government officials does not necessarily guarantee that firms can obtain what they want. Bribing government officials is like establishing an illegal contract between firms and officials and its enforcement is not protected by the legal system. When firm managers perceive that government corruption is an obstacle to their business, corruption becomes a source of institutional uncertainty, which increases costs and risks to the firms’ business. Under such circumstances, firms will be more likely to turn to the market mechanism for long-term development. Investing in R&D activities can contribute to firms’ competitive advantage in market competition.

Therefore, when firm managers perceive governmental system constraints as a severe obstacle to the firm's development and even survival, they will be more likely to invest in R&D activities to compensate for the adverse institutional impact. Such firms will thus be more likely to become innovators than non-innovators or imitators.

While perceived governmental system constraints can motivate firm managers to invest in R&D activities, such perception will not necessarily affect R&D outcomes. This is because R&D resource transformation efficiency depends on firms’ transformation and exploitation capability, which includes internalization, conversion, use, and implementation of R&D resources (Zahra & George, Reference Zahra and George2002). The firm, rather than the institutional environment, dominates the innovation transformation process when infrastructure is ready. Thus, when perceived governmental system constraints are more severe, firms are more likely to be innovators than imitators or non-innovators. However, such constraints do not necessarily make firms more likely to be effective innovators.

Hypothesis 1a: Perceived constraints from the governmental system make firms more likely to be innovators than to be imitators.

Hypothesis 1b: Perceived constraints from the governmental system make firms more likely to be innovators than to be non-innovators.

The legal system is considered another important aspect of formal institutions because it ensures contract enforcement, offers property rights protection, helps to build transactional trust, and maintains financial stability. The transparency, fairness, and efficiency of courts are vital in institutional support to firm development (Aidis et al., Reference Aidis, Estrin and Mickiewicz2008), innovation (Chaudhry & Garner, Reference Chaudhry and Garner2007), foreign direct investment (Ali, Fiess, & Macdonald, Reference Ali, Fiess and MacDonald2010), and economic growth (North, Reference North2005).

Legal systems constrain firms’ innovative activities by making unfair court decisions and failing to punish criminals. First, the formal institution of law affects firms’ innovation acquisition activities through the strength of intellectual property rights protection (Dushnitsky & Shaver, Reference Dushnitsky and Shaver2009). When formal intellectual property rights protection is weak, imitation gains more advantages, as the costs of imitators are relatively low (Luo & Wang, Reference Luo and Wang2011). The larger the technology gap between the imitator and the innovator, the easier it is for the imitator to observe successful ideas (Grabowski, Vernon, & Thomas, Reference Grabowski, Vernon and Thomas1978) and copy them. Therefore, when firm managers perceive the low quality of the court system as a severe obstacle to the firm, they lack the incentive to invest in R&D activities. This is because imitators can copy the firm's products without paying the high cost of purchasing the patent, implementing R&D activities, or being punished.

Moreover, firms in a high criminal environment will face more risks in their daily operation. From a macro perspective, research shows that crimes decrease firms’ competitiveness in Latin America (Gaviria, Reference Gaviria2002). At the micro level, the criminals in the surrounding environment deteriorate the climate for initiative and the psychological safety of employees, and further negatively affect firms' process innovations (Baer & Frese, Reference Baer and Frese2003). As a result, firms will allocate more resources in ensuring worker and property safety and guarantee daily production. When the legal system cannot punish criminal behavior, the increase in environmental uncertainty will decrease firms’ incentive to invest in R&D activities.

To summarize, constraints in the legal system decrease market fairness and increase firms’ risks of losing their intellectual property and other properties. As a result, firms have to devote more resources to dealing with the unfair and inefficient legal system and are not able or willing to invest in R&D activities. Therefore, a higher degree of perceived constraints from the legal system will make firms less likely to become innovators than imitators or non-innovators.

Hypothesis 2a: Perceived constraints from the legal system make firms less likely to be innovators than to be imitators.

Hypothesis 2b: Perceived constraints from the legal system make firms less likely to be innovators than to be non-innovators.

Formal financial institutions are the formal capital market, including the banking system and securities and debt markets (Buckley, Clegg, Cross, Liu, Voss, & Zheng, Reference Buckley, Clegg, Cross, Liu, Voss and Zheng2007). In developing countries, the banking system is a firm's primary source for external capital (Beck, Demirgüç-Kunt & Maksimovic, Reference Beck, Demirgüç-Kunt and Maksimovic2008). The banking system is regulated by the central bank, which imposes strict standards for granting loans (Cull & Xu, Reference Cull and Xu2003; Firth, Lin, Liu, & Wong, Reference Firth, Lin, Liu and Wong2009; García-Herrero, Gavilá, & Santabárbara, Reference García-Herrero, Gavilá and Santabárbara2006 ). Although China's banking system is rife with bad loans, compared to informal financing such as loans from relatives or even illegal loans from loan sharks, the banking system is formally regulated. Financial capital is a critical resource for firms to conduct innovation activities. R&D activities involves high risks and need considerable and continuous investment. Firms with sufficient financial capital are more likely to invest in R&D activities. Research has found that access to external financing such as bank financing is conducive to firm innovation (Ayyagari, Demirguc-Kunt, & Maksimovic, Reference Ayyagari, Demirgüç-Kunt and Maksimovic2011).

However, in less developed economies, formal financial institutions are usually inefficient at serving firms. In China particularly, the banking sector is heavily dominated by the state share and not in favor of private firms in terms of access to and interest of loans (Buckley et al., Reference Buckley, Clegg, Cross, Liu, Voss and Zheng2007). In 2012, the venture capital industry was still in its early stage of development in China. However, even after the industry was more mature in later years, venture capital is largely linked to the state and prefers to invest in firms that have linkage to the state (Fuller, Reference Fuller, Lewin, Murmann and Kenney2016a). The imperfection of the capital market also limits firms’ external financing for innovation (Hyytinen & Toivanen, Reference Hyytinen and Toivanen2005).

Therefore, when managers of firms perceive a lack of formal finance, they believe that their firms have fewer external financial resources for innovation investment. Thus, firms will be less likely to be innovators than to be imitators or non-innovators.

Hypothesis 3a: Lack of formal finance makes firms less likely to be innovators than to be imitators.

Hypothesis 3b. Lack of formal finance makes firms less likely to be innovators than to be non-innovators.

Informal Institutions and Firm Innovation

Informal institutions, as mentioned earlier, can also influence firm innovation through affecting the incentive structures for firm activities. Due to the difficulties in finding appropriate data to measure informal institutions, research on the impact of informal institutions on firm innovation is still at an early stage, and mostly conceptual (Child, Reference Child, Lewin, Murmann and Kenney2016; Redding, Reference Redding, Lewin, Murmann and Kenney2016). There is little empirical analysis on such impact at the firm level (Brockman et al., Reference Brockman, Khurana and Zhong2018). This emerging stream of literature provides important insights regarding the influences of different informal institutions on firm innovation. For instance, scholars have argued that a number of informal institutions in China have impeded firm innovation activities and performance. These informal institutional constraints include ‘personalism’ and lack of social trust (Redding, Reference Redding, Lewin, Murmann and Kenney2016), overreliance on informal networks (Child, Reference Child, Lewin, Murmann and Kenney2016), and group centrism (Chiu, Liou, & Kwan, Reference Chiu, Liou, Kwan, Lewin, Murmann and Kenney2016). To further our understanding of the impact of informal institutions, in this study we examine two different informal institutions, namely bribery norms in business practice and informal financial sources.

Bribery in this context is giving informal payment or gifts to non-governmental organizations in transactions with them. Bribery to private actors can be viewed as a form of networking. Firms that adopt open network strategies tend to pay more bribes to seek rents in competition (Krueger, Reference Krueger1974), avoid potential loss of resources and capability, and to overcome ineffective institutional arrangements (Huang & Rice, Reference Huang and Rice2012). However, the informal payment and gift giving can potentially increase firms’ costs in dealing with other organizations and decrease the resources that could have been invested in firm innovation activities. Furthermore, according to some research, networking in China tends to benefit innovation less compared to firms elsewhere (Jensen & Schøtt, Reference Jensen and Schøtt2014). As a combined consequence, commercial bribery activities negatively affect firms’ innovation activities by reducing firms’ resources.

On the other hand, in the business context, giving gifts means more than cultural respect. Gift giving is a part of networking or guanxi, for building trust, caring, and commitment between transaction partners such as suppliers, buyers, competitors, and other business intermediaries (Luo, Huang, & Wang, Reference Luo, Huang and Wang2012; Park & Luo, Reference Park and Luo2001; Peng & Luo, Reference Peng and Luo2000). By giving gifts, firms can enjoy priorities in concrete deeds (Steidlmeier, Reference Steidlmeier1999). Informal payment could increase the efficiency of transactions in the inefficient public sector (Nguyen, Doan, Nguyen, & Tran-Nam, Reference Nguyen, Doan, Nguyen and Tran-Nam2016). The resources in infrastructure and construction directly relates to firms’ operation and R&D activities, because telecommunication, water, and electricity are necessities for the modern manufacturing industry. In the Chinese context, commercial bribery is also a form of guanxi practice that can help firms build trust with other firms (Burt & Burzynska, Reference Burt and Burzynska2017; Park & Luo, Reference Park and Luo2001; Peng & Luo, Reference Peng and Luo2000). Such practice not only brings access to critical resources, but also enables relationship learning through information sharing and business interactions (Selnes & Sallis, Reference Selnes and Sallis2003). Relationship learning allows firms to obtain knowledge useful for innovation and is thus conducive to firms’ innovation output (Chen, Lin, & Chang, Reference Chen, Lin and Chang2009; Fang, Fang, Chou, Yang, & Tsai, Reference Fang, Fang, Chou, Yang and Tsai2011). Hsu and Saxenian (Reference Hsu and Saxenian2000) argued that the factors for technological improvements may not be embedded in guanxi, as ethnic networks and strong ties may lead to the lock-in effect of outdated technology. However, the transnational technical community connection discussed in Hsu and Saxenian (Reference Hsu and Saxenian2000) is different from the connections between firms and government. Thus, commercial bribery could increase the efficiency of R&D transformation, making firms more likely to be innovators than to be the innovation pretenders.

In lieu of the above argument, we propose that, in general:

Hypothesis 4a: Commercial bribery makes firms less likely to be innovators than to be imitators.

Hypothesis 4b: Commercial bribery makes firms less likely to be innovators than to be non-innovators.

Hypothesis 4c: Commercial bribery makes firms more likely to be innovators than to be innovation pretenders.

According to Sagrario and Ray (Reference Sagrario Floro and Ray1997), informal financial institutions are moneylenders such as relatives, friends, and credit associations who are not under the supervision of the central bank. Formal and informal financial institutions have both horizontal and vertical interplays, but the roles formal and informal sector play in financial institutions vary. The informal way of monitoring is efficient in decreasing information asymmetry. For example, provision of labor or the sales of the output are often tied with the private loans (Sagrario & Ray, Reference Sagrario Floro and Ray1997). Small firms use informal financial institutions as the source of a large share of investment; however, informal financial sources sometimes charge a rate higher than the formal financial institutions for risk compensation. Moreover, even in fast-growing economies, the reputation- and relationship-based informal financial institutions are limited and unlikely to substitute the formal financial institutions in supporting firms’ growth (Beck & Demirgüç-Kunt, Reference Beck and Demirgüç-Kunt2008). Lack of informal finance decreases firms’ financial resources for innovative activities. Without financial support from the informal financial institutions, firms have fewer resources for investment in innovation. Instead of doing the original innovation, firms are only capable of imitating other products or not engaging in innovation.

Hypothesis 5a: Lack of informal finance makes firms less likely to be innovators than to be imitators.

Hypothesis 5b: Lack of informal finance makes firms less likely to be innovators than to be non-innovators.

Joint Effect of Formal and Informal Institutions on Firm Innovation

Formal and informal institutions do not operate in isolation but work jointly when influencing firm behavior (Ang et al., Reference Ang, Benischke and Doh2015; Holmes, Miller, Hitt, & Salmador, Reference Holmes, Miller, Hitt and Salmador2011; North, Reference North2005). In this section we examine how informal institutions, namely, bribery and lack of informal finance, moderate the relationships between formal institutions and firms’ propensity to become a certain type of innovator.

Bribery, formal institutions, and firm innovator type

In the previous section we argue that perceived severe constraints from the governmental system will stimulate firms to increase their innovation input so as to compensate for the disadvantages derived from such institutional constraints. The positive impact of perceived governmental system constraints will be stronger if firms also experience commercial bribery. As argued above, bribery can increase the efficiency of firms’ R&D transformation by building trust and securing access to critical resources and knowledge that contribute to transforming innovation input into output (Chen et al., Reference Chen, Lin and Chang2009; Child, Reference Child, Lewin, Murmann and Kenney2016; Fang et al., Reference Fang, Fang, Chou, Yang and Tsai2011). When experiencing commercial bribery, firms can expect relatively stable and secured inflow of resources and knowledge critical for their innovation. Thus, facing governmental system constraints, as firms that experience commercial bribery will have more confidence in their innovation transformation efficiency, they will be more likely to invest more in their innovation activities.

Furthermore, when firms’ innovation input is mainly a response to severe governmental system constraints, it is likely that such innovation efforts could be ineffective if firms lack sufficient capabilities, resources, and knowledge to transform the input into output (Chen et al., Reference Chen, Lin and Chang2009; Li, Chen, & Shapiro, Reference Li, Chen and Shapiro2015). Therefore, when firms have innovation input, higher levels of governmental system constraints will increase firms’ innovation output if firms also experience commercial bribery, which can provide critical resources and knowledge (Fu, Revilla Diez, & Schiller, Reference Fu, Revilla Diez and Schiller2013). On the other hand, without commercial bribery, when firms have innovation input, severe governmental system constraints will hinder firm innovation output. Therefore, we hypothesize the following moderating effects of commercial bribery on governmental system constraints and firm innovator type.

Hypothesis 6a: Commercial bribery moderates the relationship between governmental system constraints and a firm's likelihood to be innovator than to be imitator or non-innovator such that the presence of commercial bribery strengthens the positive impact of governmental system constraints on a firm's likelihood to be innovator than to be imitator or non-innovator.

Hypothesis 6b: Commercial bribery moderates the relationship between governmental system constraints and a firm's likelihood to be innovator than to be innovation pretender such that the impact of governmental system constraints is positive with the presence of commercial bribery and become negative when commercial bribery is absent.

Similarly, we also argue that commercial bribery will moderate the effects of perceived legal system constraints on firm innovator type. As discussed above, perceived constraints from the legal system will decrease the likelihood of firms to become innovator rather than imitator or non-innovator, due to the system's failure in protecting intellectual property and other firm properties. However, the presence of commercial bribery may compensate for such institutional failure or ‘institutional void’ (Krammer, Reference Krammer2017; Luo et al., Reference Luo, Huang and Wang2012). Bribery, as a form of informal networking or guanxi practice, can reduce firms’ risk of losing intellectual property by building trust between firms and their suppliers, buyers, and other industry intermediaries (Peng & Luo, Reference Peng and Luo2000). Business trust can serve as informal contracting to prevent opportunistic behavior and thus mitigate the negative impact of an unfair, ineffective legal system on firm innovation (Brockman et al., Reference Brockman, Khurana and Zhong2018; Redding, Reference Redding, Lewin, Murmann and Kenney2016; F. Xie, Zhang, & Zhang, Reference Xie, Zhang and Zhang2018). Therefore, we hypothesize that the negative impact of perceived legal system constraints on firms’ likelihood of becoming innovator is weaker if firms also experience commercial bribery.

Hypothesis 7: Commercial bribery moderates the relationship between legal system constraints and a firm's likelihood to be innovator than to be other types of innovator (i.e., imitator, non-innovator, and innovation pretender) such that the presence of commercial bribery weakens the negative impact of legal system constraints on a firm's likelihood to be innovator than to be other types of innovator.

Bribery can also moderate the impact of formal financial constraints on firm innovator type. Innovation activities require extensive investment and firms are very likely to rely on external finance (Brown, Martinsson, & Petersen, Reference Brown, Martinsson and Petersen2012). As previously discussed, bribery, by building networks and trust, can provide firms access to resources and knowledge from their business partners. Such resource inflow can mitigate to some extent the resource constraints imposed by formal financial institutions (Burt & Burzynska, Reference Burt and Burzynska2017; Levine, Lin, & Xie, Reference Levine, Lin and Xie2018). Therefore, we posit that the presence of commercial bribery can reduce the negative impact of perceived lack of formal finance on firms’ likelihood of becoming innovator.

Hypothesis 8: Commercial bribery moderates the relationship between lack of formal finance and a firm's likelihood to be innovator than to be other types of innovator (i.e., imitator, non-innovator, and innovation pretender) such that the presence of commercial bribery weakens the negative impact of lack of formal finance on a firm's likelihood to be innovator than to be other types of innovator.

Lack of informal finance, formal institutions, and firm innovator type

Similar to bribery, lack of informal finance also moderates the relationships between formal institutional constraints and firm innovator type. The mechanisms of these moderating effects are relatively straightforward compared to that of bribery. As argued before, while firms may want to compensate for the institutional disadvantages derived from governmental system constraints by making more innovation efforts, they need sufficient capabilities, resources, and knowledge to effectively conduct and transform such innovation activities (Li et al., Reference Li, Chen and Shapiro2015). As informal financial institutions can serve as a substitute for formal financial institutions, the absence of support from such informal financing channels will further hinder firms’ innovation efforts despite their willingness to enhance competitive advantages through innovation.

Hypothesis 9: Lack of informal finance moderates the relationship between governmental system constraints and a firm's likelihood to be innovator than to be other types of innovator (i.e., imitator, non-innovator, and innovation pretender) such that the presence of lack of informal finance weakens the positive impact of governmental system constraints on a firm's likelihood to be innovator than to be other types of innovator.

Moreover, constraints from informal financial institutions will exacerbate the detrimental impact of legal system constraints on firm innovation. Facing high risks of losing intellectual property or other properties, firms that fail to gain resources from informal financing are less likely to innovate, compared to those that have support from informal finance. Likewise, while informal financing could serve as a substitute for formal finance, if firms are constrained in obtaining capital from both channels, they will be even less likely to innovate. Therefore, we hypothesize that:

Hypothesis 10: Lack of informal finance moderates the relationship between legal system constraints and a firm's likelihood to be innovator than to be other types of innovator (i.e., imitator, non-innovator, and innovation pretender) such that the presence of lack of informal finance strengthens the negative impact of legal system constraints on a firm's likelihood to be innovator than to be other types of innovator.

Hypothesis 11: Lack of informal finance moderates the relationship between lack of formal finance and a firm's likelihood to be innovator than to be other types of innovator (i.e., imitator, non-innovator, and innovation pretender) such that the presence of informal financial institutional constraints strengthens the negative impact of lack of formal finance on a firm's likelihood to be innovator than to be other types of innovator.

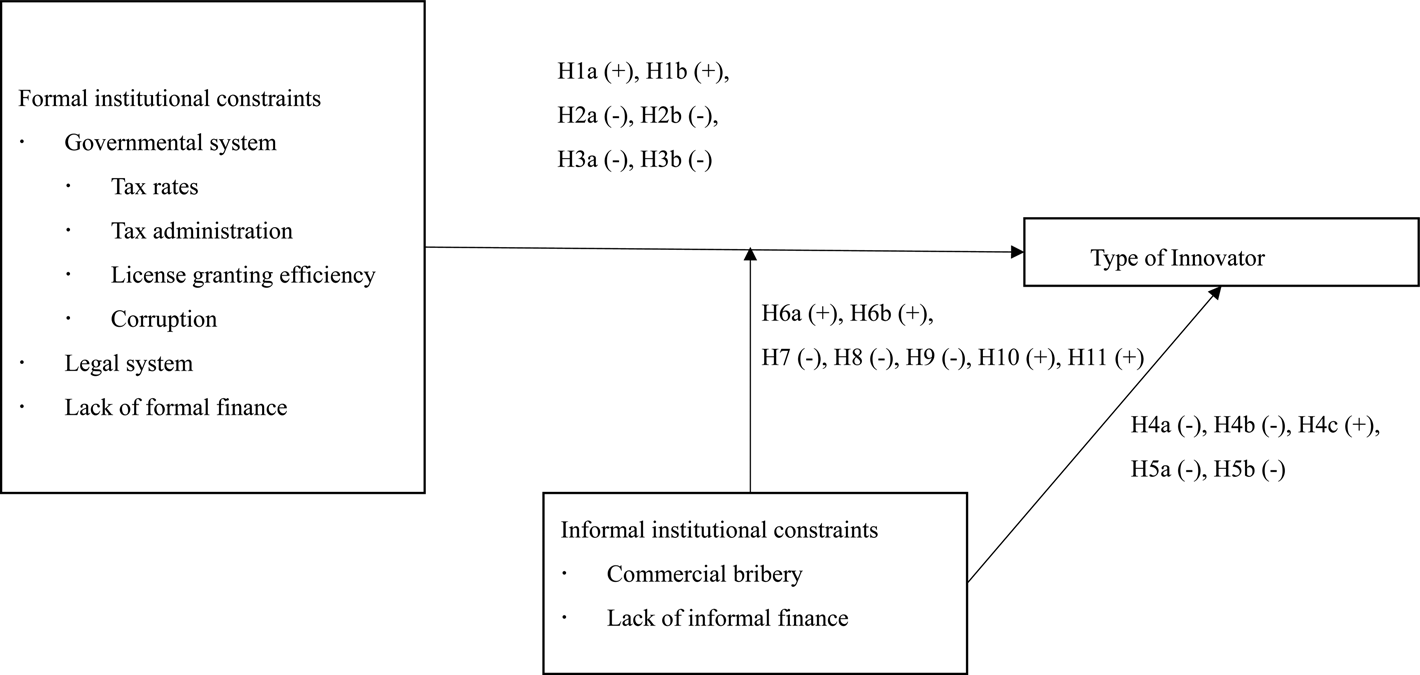

Figure 2 summarizes our theoretical framework and the proposed hypotheses.

Figure 2. Theoretical framework and hypotheses

METHODS

Data

We used the 2012 Enterprise Survey Data collected by the World Bank on 2848 Chinese firms. The survey collects the information of randomly selected firms from 25 cities in 2011. This article reserves 1207 manufacturing firms from the 2848 firms because manufacturing module survey is more comprehensive and complete, and relevant to firm innovation. Missing values in control variables are deleted. We recorded the ‘Don't know’ and ‘Does not apply’ answers as missing values in all variables except for the competition intensity variable.

Measures

Dependent variables

Innovator. When R&D dummy is 1 and new product deployment dummy is 1.

Imitator. When R&D dummy is 0 and new product deployment dummy is 1.

Innovation pretender. When R&D dummy is 1 and new product deployment dummy is 0.

Non-innovator. When R&D dummy is 0 and new product deployment dummy is 0.

Innovator vs. imitator. Innovator vs. imitator is coded ‘1’ if the firms are innovators. The variable is coded ‘0’ if the firms are imitators.

Innovator vs. innovation pretender. Innovator vs. innovation pretender is coded ‘1’ if the firms are innovators. The variable is coded ‘0’ if the firms are innovation pretenders.

Innovator vs. non-innovator. Innovator vs. non-innovator is coded ‘1’ if the firms are innovators. The variable is coded ‘0’ if the firms are non-innovators.

Independent variables

Perceived constraints from the governmental system. The level of perceived constraints from the governmental system is the average of the sum of firms’ perception of government tax rate, government tax administration, government permits, and government corruption. Reliability was satisfactory (Cronbach's alpha = 0.81). Each of the items is graded from zero to four to evaluate the degree the item is an obstacle to the current operation of the establishment with Likert-type scales ranging from ‘no obstacle’ (0) to ‘very severe obstacle’ (4).

Perceived constraints from the legal system. The perceived constraints from the legal system variable are graded from zero to four to evaluate the degree courts’ unfairness and inefficiency is an obstacle to the current operation of the establishment with Likert-type scales ranging from ‘no obstacle’ (0) to ‘very severe obstacle’ (4).

Lack of formal finance. Firms reported not ‘getting financial support from formal financial institutions in purchasing working capital or fixed assets’ are coded ‘1’, otherwise ‘0’.

Commercial bribery. Firms being expected or requested to give informal gifts or payment in order to get electricity, water, telephone connection, construction permits are coded ‘1’, otherwise ‘0’. Different from government corruption, which is imposed by the government, commercial bribery comes from the extortion of private actors.

Lack of informal finance. Firms reported not getting financial support from informal financial institutions in purchasing working capital or fixed assets are coded ‘1’, otherwise ‘0’.

Control variables

First, we considered regional business environment by controlling the crime variable. The incomplete specification and inconsistent enforcement of property right protection hinders innovation and productivity growth (Jefferson & Rawski, Reference Jefferson and Rawski1994). The crime obstacle variable is graded from zero to four to evaluate the degree property loss is an obstacle to the current operation of the establishment with Likert-type scales ranging from ‘no obstacle’ (0) to ‘very severe obstacle’ (4).

Second, we considered firms’ absorptive ability by controlling the skilled worker percentage variable and licensed technology dummy. Skilled worker is a form of human capital that increases the efficiency of knowledge transformation (Audretsch & Feldman, Reference Audretsch and Feldman1996). Skilled worker percentage is defined as the percentage of skilled workers to total full-time workers at the end of 2011. Licensed technology dummy measures firms’ technology capability in using licensed technology excluding office software from the foreign-owned company. Licensed technology could bring firms instantaneous profits from the new products but also incur costs (Yang & Maskus, Reference Yang and Maskus2001). Firms that use licensed technology from a foreign-owned company are coded ‘1’, otherwise ‘0’.

In addition, we considered some firms’ characteristics by controlling for firm age, revenue growth rate, and firm size. When engaging in innovative activities, SMEs have limitations in information on policy instruments, capital, management qualifications, technology, and qualified employees (Kleinknecht, Reference Kleinknecht1989). This article follows Lin, Lin, and Song's (Reference Lin, Lin and Song2010) measurement of firm age by using 2011 minus the year this establishment begin operations. This article also follows Chadee and Roxas (Reference Chadee and Roxas2013) in the measurement of revenue growth. The firms’ revenue growth rate is calculated as the total annual sales in 2011 divided by the average annual sales three years ago and then minus 1. Firm size variable is categorized by the number of employees. Firms with more than 100 employees are large firms. Firms with more than 20 but less than 99 employees are medium firms, while firms with less than 19 employees are small firms.

Moreover, we controlled for the variable of top manager's experience by measuring years of experience the firms’ top manager has in the sector. Work experience could affect top managers’ cognitive thinking and further affect strategic decision making (Hambric & Mason, Reference Hambrick and Mason1984). We also controlled for the state bank loan, which refers to the log value of the most recent loan obtained from State-owned banks or government agencies to further address formal financing experienced by the focal firm. We considered the industrial effects by controlling for industrial competition dummy and industry dummy. This article follows Jaworski and Kohli (Reference Jaworski and Kohli1993) in measuring the industrial competition dummy variable by comparing the number of similar products of competitors to measure the competition intensity. If the firms’ product faces ‘too many to count’ similar products of competitors, this variable is coded as 1. If the firms’ product faces countable similar products of competitors, this variable is coded as 0. For industry dummy variable, we coded 20 different industries ranging from food industry to recycling industry as 19 different industry dummies.

Regression Model

We used four models to examine the impact from perceived institutional constraints to the firms’ tendency to become a certain type of innovator. Model 1 regressed control variables. Model 2 added the independent variables to Model 1. Model 3 and Model 4 added the moderators of commercial bribery and lack of informal finance to Model 2 respectively. All the dummy dependent variables are regressed in Probit regressions with robust standard error.

RESULTS

Descriptive Statistics

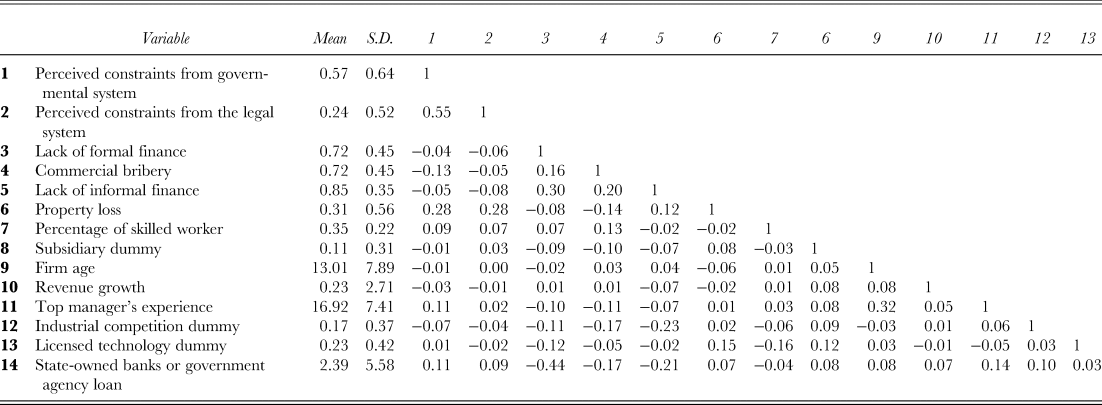

Table 1 shows the means, standard deviations, and Pearson correlations of perceived items of institutional constraints and control variables. The mean of perceived constraints from the governmental system and legal system are lower than 0.6, indicating that most sample firms believe that formal institutional constraints from governmental system and legal system are not serious.

Table 1. Means, standard deviations, and Pearson correlations of key variables

Notes: Correlations with an absolute value equal or larger than 0.05 are significant at the 0.1 level.

Hierarchical Regression Analysis

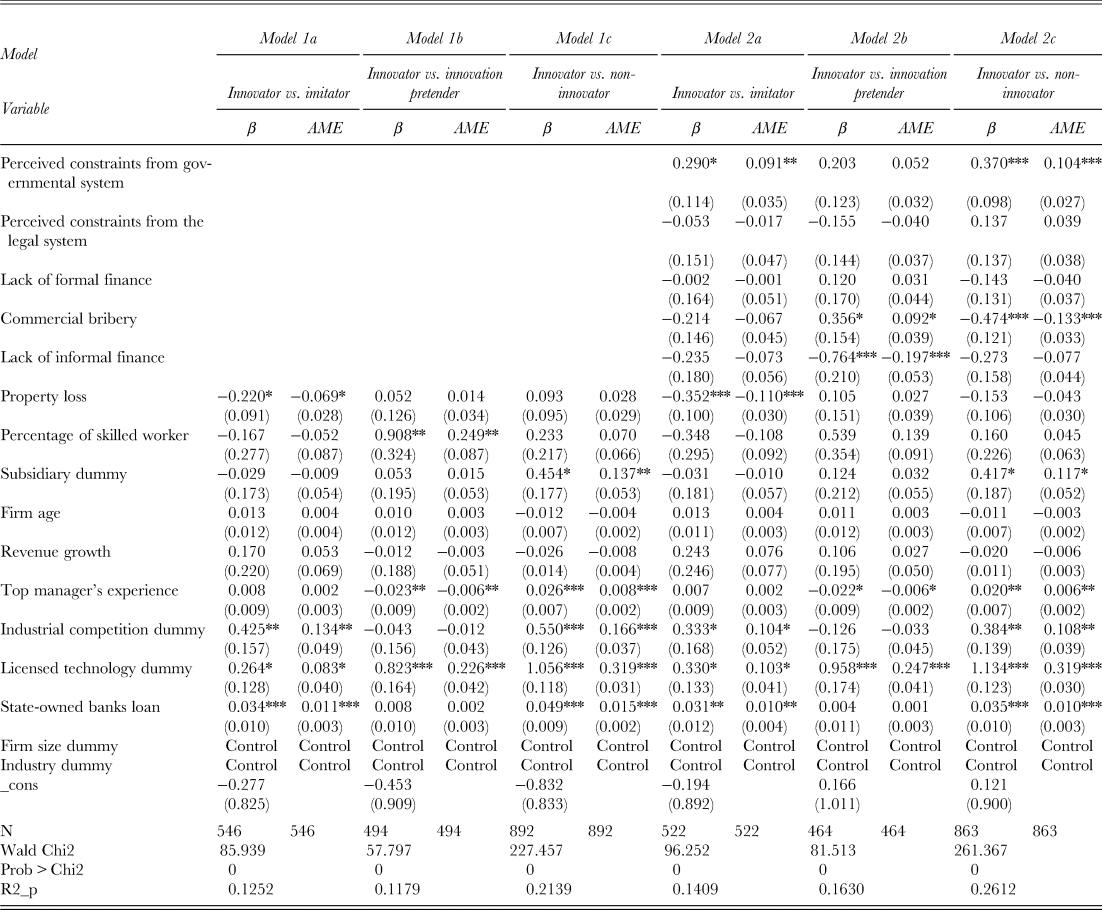

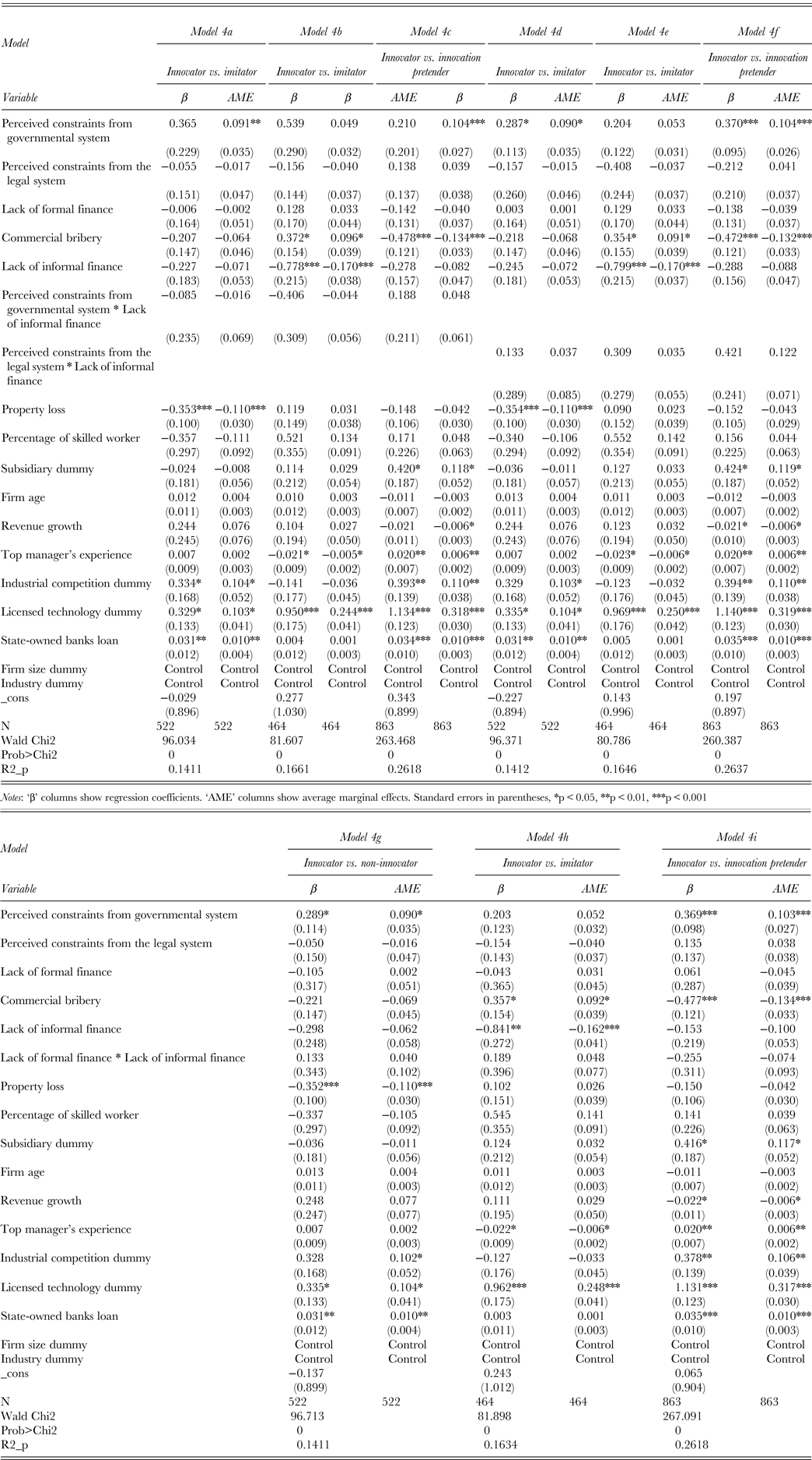

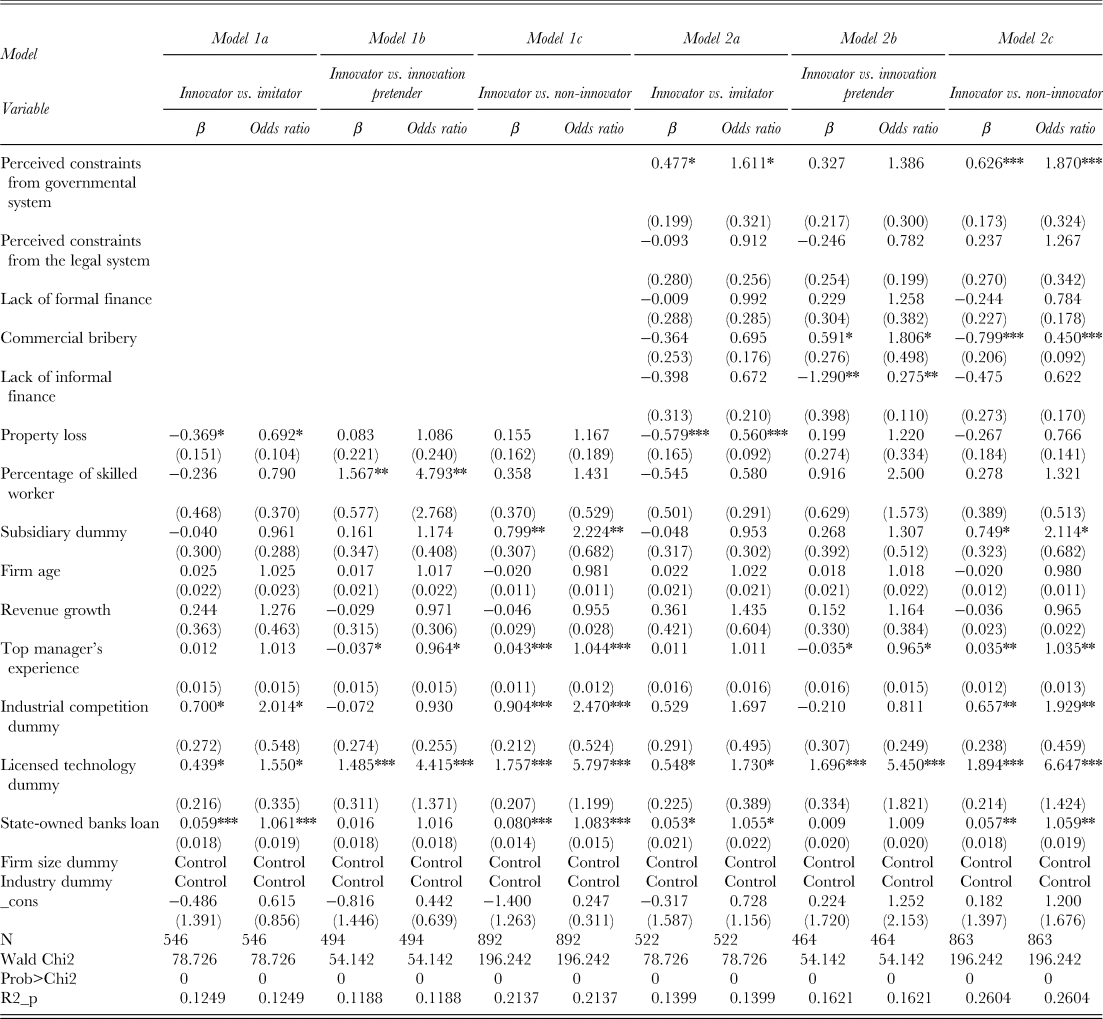

Table 2 shows the regression results of Model 1 and Model 2. Table 3 shows the regression results of Model 3 with the moderating variable of commercial bribery. Table 4 shows the regression results of Model 4 with the moderating variable of lack of informal finance. The Wald test of each regression from Model 1 to Model 4 indicates that the null hypothesis stating that the coefficients are simultaneously equal to 0 can be rejected (Prob > Chi2 = 0.00). Table 2 shows that perceived constraints from the governmental system is positively and significantly correlated to firms’ likelihood of becoming an innovator rather than an imitator (Model 2a, β = 0.290, p < 0.05) and a non-innovator (Model 2c, β = 0.370, p < 0.001). One unit increase in perceived constraints from the governmental system, on average, increases the firm's likelihood of being innovators instead of being imitators by 9.1% (Model 2a, AME = 0.091, p < 0.01) and the firms’ likelihood of being innovators instead of being non-innovators by 10.4% (Model 2c, AME = 0.104, P < 0.001). Thus, H1a and H1b are both supported. From the same table, we can find that perceived constraints from the legal system is not significantly correlated to firms’ likelihood of becoming an innovator rather than an imitator (Model 2a, β = −0.053, p > 0.05) or a non-innovator (Model 2c, β = 0.137, p > 0.05). Therefore, H2a and H2b are not supported.

Table 2. Institutional constraints and types of innovator

Notes: ‘β’ columns show regression coefficients. ‘AME’ columns show average marginal effects. Standard errors in parentheses, *p < 0.05, **p < 0.01, ***p < 0.001

Table 3. Interaction effects of formal institutional constraints and commercial bribery

Notes: ‘β’ columns show regression coefficients. ‘AME’ columns show average marginal effects. Standard errors in parentheses, *p < 0.05, **p < 0.01, ***p < 0.001

Table 4. Interaction effects of formal institutional constraints and lack of informal finance

Notes: ‘β’ columns show regression coefficients. ‘AME’ columns show average marginal effects. Standard errors in parentheses, *p < 0.05, **p < 0.01, ***p < 0.001

For the impact of lack of formal finance, Table 2 shows that lack of formal finance does not significantly relate to innovator vs. imitator (Model 2a, β = −0.002 p > 0.05) or innovator vs. non-innovator (Model 2c, β = −0.143, p > 0.05) The inability in getting financial resources directly affects firms’ investment in R&D activities and R&D input transformation efficiency. Thus, H3a and H3b are not supported. For the impact of commercial bribery, Table 2 shows the significant positive relationship between commercial bribery and innovator vs. innovation pretender (Model 2b, β=0.356, p < 0.05) and the significant negative relationship between commercial bribery and innovator vs. non-innovator (Model 2c, β = −0.474, p < 0.001). One unit increase in commercial bribery, on average, increases the firm's likelihood of being innovators rather than being innovation pretenders by 9.2% (Model 2b, AME = 0.092, p < 0.05) but decreases firms’ likelihood of being innovators rather than being non-innovators by 13.3% (Model 2c, AME = 0.133, p < 0.001). However, commercial bribery is not significantly related to innovator vs. imitator (Model 2a, β = −0.214, p > 0.05). Commercial bribery increases financial cost for firms and decreases their investment R&D activities. Thus, H4a is not supported, but H4b and H4c are supported. Table 2 shows lack of informal finance insignificantly negatively relates to innovator vs. non-innovator (Model 2c, β = −0.273, p > 0.05) and innovator vs. imitator (Model 2a, β = −0.235, p > 0.05). Thus, H5a and H5b are not supported.

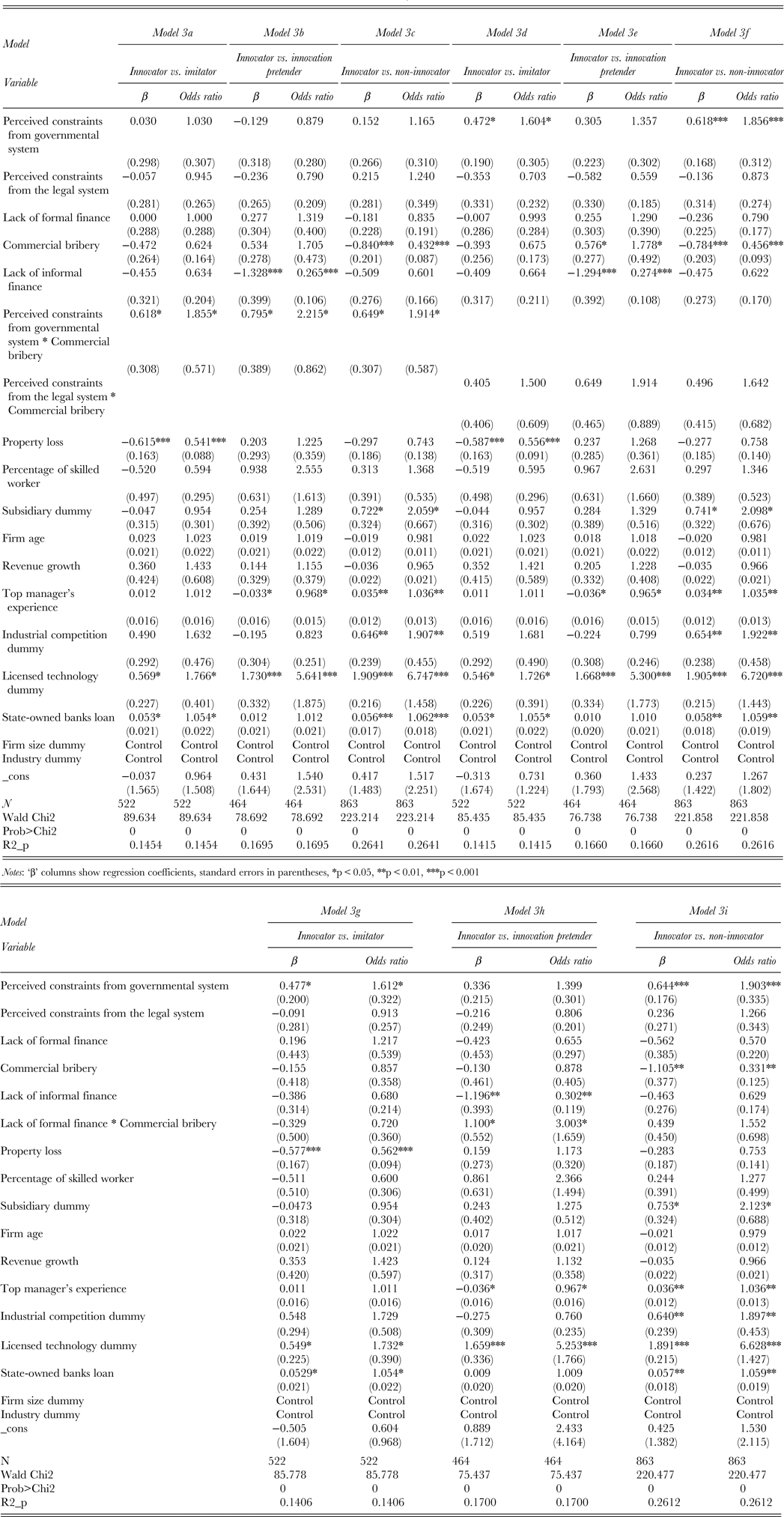

Table 3 shows that the interaction term of perceived constraints from the governmental system and commercial bribery is significantly positively related to innovators vs. imitators (Model 3a, β = 0.374, p < 0.05) and innovators vs. non-innovators (Model 3c, β = 0.370, p < 0.05). One unit increases in perceived constraints from the government system for firms committed commercial bribery, on average, increases the firm's likelihood of being innovators rather than being imitators by 12% (Model 3a, AME = 0.120, p < 0.05) and firm's likelihood of being innovators rather than being non-innovators by 10% (Model 3c, AME = 0.100, p > 0.05). Thus, H6a is supported. The interaction term of the government system constraints and commercial bribery significantly positively relates to innovator vs. innovation pretender (Model 3b, β = 0.466, p < 0.05). One unit increases in perceived constraints from the government system for firms committed commercial bribery, on average, increases the firm's likelihood of being innovators rather than being innovation pretenders by 11.3% (Model 3b, AME = 0.113, p > 0.05). Thus, H6b is supported. The positive effect of the interaction term of perceived constraints from the legal system and commercial bribery on innovator vs. imitator (Model 3d, β = 0.223, p > 0.05), innovator vs. non-innovator (Model 3f, β = 0.251, p > 0.05), or innovator vs. innovation pretender (Model 3e, β = 0.394, p > 0.05) are not significant in Table 3. Thus, H7 is not supported. The interaction term of lack of formal finance and commercial bribery is positively related to innovator vs. innovation pretender (Model 3h, β = 0.623, p < 0.05) but not significantly related to innovator vs. imitator (Model 3g, β = −0.212, p > 0.05) or innovator vs. non-innovator (Model 3i, β = 0.236, p > 0.05). Thus, H8 is not supported.

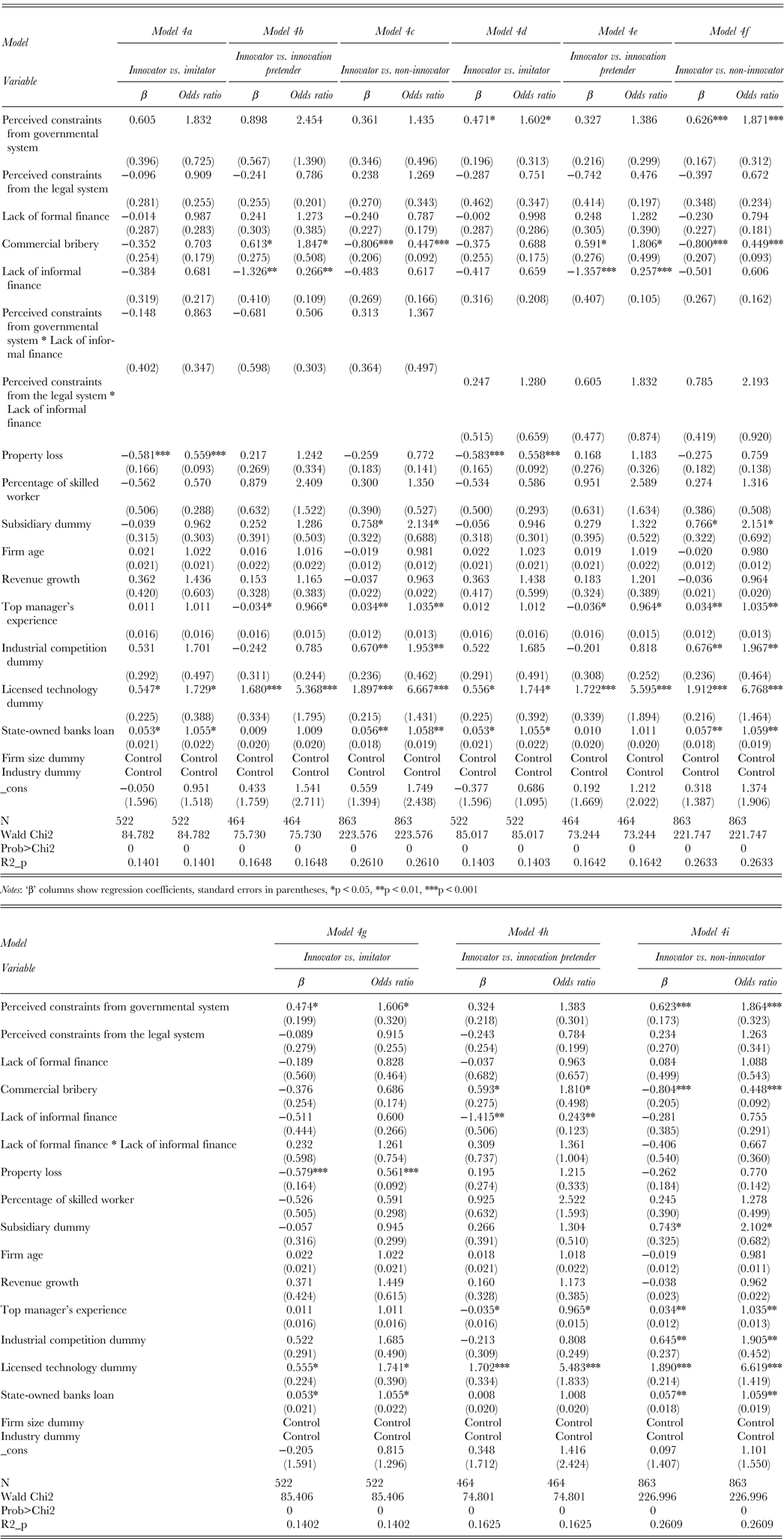

As shown in Table 4, for the impact of lack of informal finance, interaction term of lack of informal finance and government system constraints interaction is not significantly related to innovator vs. imitator (Model 4a, β = −0.085, p > 0.05), innovator vs. innovation pretender (Model 4b, β = −0.406, p > 0.05), or innovator vs. non-innovator (Model 4c, β = 0.188, p > 0.05). Thus, H9 is not supported. The positive effect of the interaction of perceived constraints from the legal system and lack of informal finance is not significant on innovator vs. imitator (Model 4d, β = 0.133, p > 0.05), innovator vs. innovation pretender (Model 4e, β = 0.309, p > 0.05), or innovator vs. non-innovator (Model 4f, β = 0.421, p > 0.05). Thus, H10 is not supported. Table 4 further shows that the interaction term of lack of formal finance and lack of informal finance is not significantly related to innovator vs. imitator (Model 4g, β = 0.133, p > 0.05), innovator vs. innovation pretender (Model 4h, β = 0.189, p > 0.05), or innovator vs. non-innovator (Model 4i, β = −0.255, p > 0.05). Thus, H11 is not supported.

Robustness Check

To check the overall robustness of the empirical results, we applied the logistic regression model to the same set of variables. We reported the regression results and odds ratios from Table 5 to Table 7. The Wald test of each regression from Model 1 to Model 4 indicates that the null hypothesis stating that the coefficients are simultaneously equal to 0 can be rejected (Prob > Chi2 = 0.00). The results obtained from the logistic regression model are overall consistent with the Probit model estimations, indicating robustness of the results.

Table 5. Institutional constraints and types of innovator

Notes: ‘β’ columns show regression coefficients, standard errors in parentheses, *p < 0.05, **p < 0.01, ***p < 0.001

As shown in Table 5, perceived constraints from the governmental system is significantly positively related to innovator vs imitator (β = 0.477, p < 0.05) and innovator vs. non-innovator (β = 0.626, p < 0.001). One unit increase in perceived constraints from the governmental system increases the odds of being innovators rather than being imitators by 1.611 (odds ratio = 1.611, p < 0.05) and firms’ odds of being innovators rather than being non-innovators by 1.870 (odds ratio = 1.870, p < 0.001). Thus, H1a and H1b are supported. Perceived constraints from the legal system are not significantly related to innovators vs. imitator (β = −0.093, p > 0.05) or innovator vs. non-innovator (β = 0.237, p > 0.05). Thus, H2a and H2b are not supported. Lack of formal finance is not significantly related to innovator vs. imitator (β = −0.009, p > 0.05) or innovator vs. non-innovator (β = −0.244, p > 0.05). Thus, H3a and H3b are not supported. Commercial bribery is significantly positively related to innovator vs. innovation pretender (β = 0.591, p < 0.05), but negatively related to innovator vs. non-innovator (β = −0.799, p < 0.001). However, commercial bribery is insignificantly related to innovator vs. imitator (β = −0.364, p > 0.05). One unit increase in commercial bribery increases firms’ odds of being innovators rather than being innovation pretenders by 1.806 (odds ratio = 1.860, p < 0.05), but it decreases firms’ odds of being innovators rather than being non-innovators by 0.450 (odds ratio = 0.450, p < 0.001). Thus, H4b and H4c are supported, but H4a is rejected. Lack of informal finance is not significantly related to innovator vs. imitator (β = −0.398, p > 0.05) or innovator vs. non-innovator (β = −0.475, p > 0.05). Thus, H5a and H5b are not supported.

As shown in Table 6, the interaction term between commercial bribery and perceived constraints from the governmental system significantly positively relates to innovator vs. imitator (β = 0.618, p < 0.05), innovator vs. innovation pretender (0.795, p < 0.05), and innovator vs. non-innovator (β = 0.649, p < 0.05). For firms that committed commercial bribery, one unit increase in perceived constraints from the governmental system increases firms’ odds of being innovators rather than being imitators by 1.855 (odds ratio = 1.855, p < 0.05), firms’ odds of being innovators rather than being innovation pretenders by 2.215 (odds ratio = 2.215, p < 0.05), and firms’ odds of being innovators rather than being non-innovators by 1.914 (odds ratio = 1.914, p < 0.05). Thus, H6a and H6b are supported. The interaction term between perceived constraints from the legal system constraints and commercial bribery is not significantly related to innovator vs. imitator (β = 0.405, p > 0.05), innovator vs. innovation pretender (β = 0.649, p > 0.05), or innovator vs. non-innovator (β = 0.496, p > 0.05). Thus, H7 is not supported. The interaction term between lack of formal finance and commercial bribery is not significantly related to innovator vs. imitator (β = −0.329, p > 0.05) or innovator vs. non-innovator (β = 0.439, p > 0.05). The interaction term between lack of formal finance and commercial bribery is significantly positively related to innovator vs. innovation pretender (β = 1.100, p < 0.05), but it is insignificantly related to innovator vs. imitator (β = −0.329, p > 0.05) and innovator vs. non-innovator (β = −0.439, p > 0.05). Thus, H8 is not supported.

Table 6. Interaction effects of formal institutional constraints and commercial bribery

Notes: ‘β’ columns show regression coefficients, standard errors in parentheses, *p < 0.05, **p < 0.01, ***p < 0.001.

In Table 7, the interaction term of perceived constraints from the governmental system and lack of informal finance is not significantly related to innovator vs. imitator (β = −0.148, p > 0.05), innovator vs. innovation pretender (β = −0.618, p > 0.05), and innovator vs. non-innovator (β = 0.313, p > 0.05). Thus, H9 is not supported. The interaction term of perceived constraints from the legal system and lack of informal finance is not significantly related to innovator vs. imitator (β = 0.247, p > 0.05), innovator vs. innovation pretender (β = 0.605, p > 0.05), and innovator vs. non-innovator (β = 0.785, p > 0.05). Thus, H10 is not supported. The interaction terms of lack of formal finance and lack of informal finance is not significantly related to innovator vs. imitator (β = 0.232, p > 0.05), innovator vs. innovation pretender (β = 0.309, p > 0.05), and innovator vs. non-innovator (β = −0.406, p > 0.05). Thus, H11 is not supported.

Table 7. Interaction effects of formal institutional constraints and lack of informal finance

Notes: ‘β’ columns show regression coefficients, standard errors in parentheses, *p < 0.05, **p < 0.01, ***p < 0.001

DISCUSSION

By using the World Bank sample of Chinese manufacturing firms, this article examines the impacts of formal and informal institutions on firms’ likelihood of becoming a certain type of innovator. The results show that, for formal institutions, perceived constraints from the governmental system positively affect firms’ likelihood of being innovators than other types of innovators. In addition, lack of formal finance negatively affects firms’ likelihood of being innovators rather than being non-innovators. In terms of informal institutions, commercial bribery negatively affects firms’ likelihood of being innovators rather than being non-innovators, but positively affects firms’ likelihood of being innovators rather than being innovation pretenders.

Firms in different business domains apply for different licenses, and the difficulty in applying the licenses and permissions varies. In terms of the legal system, unfair and inefficient courts positively but not significantly affect firm innovation. Unfair and inefficient courts increase firms’ cost in protecting their intellectual property through legal processes if the innovative products are in patent forms. Firms that invest in R&D activities without applying for patent certification are one of the possible causes for the positive but insignificant regression results. We infer that because of the export orientation, these firms still keep on investing in R&D to make the products competitive in the global market.

Commercial bribery has a moderating effect on the impact of the governmental system constraints on firms’ likelihood of being innovators rather than other types of innovators. The presence of commercial bribery strengthens the positive effect of governmental system constraints on firms’ likelihood of being innovators rather than other types of innovators. Lack of informal finance does not moderate the impact of formal institutions significantly. The insignificance of this moderating effect can be possibly explained by the small scale of informal finance in our sample.

This article has three major contributions. First, this article enriches the institutional theory and innovation research by stating a framework that includes multidimensional institutions and two levels of innovative performance. Second, this article examined the moderating effect of informal institutions on the relationship between formal institutions and firms’ likelihood of being innovators rather than being other types of innovators. Third, this article uses both the perceived and experienced items to measure institutional constraints. The measurements allow us to compare the constraints that firms perceived and the constraints that are actually imposed on firms.

This article also provides some implications for building the institutional environment. The research result addresses the importance of developing formal institutional support in both the government and the legal system. In addition, policies such as offering formal financial institutional support, decreasing bribery, and organizing the informal institutional financial resources are beneficial for firms’ innovative performance.

Limitations and Future Research Directions

There are some limitations. First, our measures of innovation are limited due to data constraint. Second, the constraints reported by the respondents may have bias because of variation within individual firms’ evaluation standards. Third, the hypotheses about governmental and legal systems are largely not supported by the regression results. Fourth, the effect size detected by the current empirical models is relatively weak for the independent variables of perceived constraints from the governmental system and commercial bribery. Notwithstanding the given explanation in the discussion part, future study could further research on the causes of insignificance in results and the relatively weak effect size. Last but not least, this research found the association between institutions and firm innovative types. However, we cannot rule out the reverse causality due to the data limitation. We leave to future research to address such limitations.