Introduction

Corporate political activity (CPA), defined as “corporate attempts to shape government policy” (Hillman et al., Reference Hillman, Keim and Schuler2004: 837), has been an active field of scholarship over the past two decades (Hadani et al., Reference Hadani, Bonardi and Dahan2017a, Brown, Reference Brown2016). Several factors have contributed to this research. First, evidence exists to support the idea that CPA investments can lead to monopolistic rents. For example, Stratmann (Reference Stratmann1991) estimated that $192,000 contributed to politicians by the sugar industry in 1985 brought more than $5 billion in value in sugar subsidies over a five-year period, an impressive return on investment to be sure. Second, since the regulatory era began in the 1960s, the impact of government on business has increased dramatically (Shaffer, Reference Shaffer1995), and at this point, regulation appears to impact just about every aspect of modern business activity (Lester et al., Reference Lester, Hillman, Zardkoohi and Cannella2008). Third, CPA is controversial. Many American executives dislike government and politics and find CPA distasteful (Frynas et al., Reference Frynas, Mellahi and Pigman2006, Schuler et al., Reference Schuler, Rehbein and Cramer2002, Shaffer, Reference Shaffer1995, Shaffer and Hillman, Reference Shaffer and Hillman2000, Pearce et al., Reference Pearce, De Castro and Guillén2008), the public views the American campaign finance system negatively (Pew Research Center, 2023), and scholars have generally struggled to show that CPA leads to higher firm performance (Hadani et al., Reference Hadani, Bonardi and Dahan2017a). These factors have likely encouraged the development of a robust academic literature on CPA.

One notable gap in this stream has been the lack of research about CPA’s antecedents (Lawton et al., Reference Lawton, McGuire and Rajwani2013), a remarkable problem given the fact that research has often found a negative relationship between CPA and firm performance (Hadani and Schuler, Reference Hadani and Schuler2013, Lux et al., Reference Lux, Crook and Leap2012, Hadani et al., Reference Hadani, Bonardi and Dahan2017a). Indeed, even to the extent that research has delved into CPA antecedents, this research has produced such anemic results, generally only explaining 2–4 percent of the variance on average (Lux et al., Reference Lux, Crook and Woehr2011). Consequently, a number of scholars have called for additional research into this question (Lux et al., Reference Lux, Crook and Woehr2011, Hillman et al., Reference Hillman, Keim and Schuler2004, Lawton et al., Reference Lawton, McGuire and Rajwani2013, De Villa et al., Reference De Villa, Rajwani, Lawton and Mellahi2019, Combs et al., Reference Combs, Gentry, Lux, Jaskiewicz and Crook2020). More specifically, scholars have sought more focused inquiry exploring not only whether specific CEO characteristics influence firm CPA (Rudy and Johnson, Reference Rudy and Johnson2019) but also what factors impact the choices a firm makes regarding specific CPA tactics as opposed to simply engaging in CPA in the first place (Eun et al., Reference Eun, Lee and Jung2023, Jia, Reference Jia2018). With this article, we seek to add to both those literatures.

In this research, we seek to link aspects of CEO personality with firm CPA activity. Rather than relying on one characteristic of CEOs to explain CPA, such as narcissism (Greiner et al., Reference Greiner, Kim and Cordon Thor2023b), what they value (Greiner et al., Reference Greiner, Kim and Cordon Thor2023a), or their demographics (Rudy and Johnson, Reference Rudy and Johnson2019), we rely on the most widely accepted and most comprehensive measure of individual personality, the five-factor model (Ozer and Benet-Martinez, Reference Ozer and Benet-Martinez2006). Similarly, rather than simply treating all CPA the same, we distinguish between CPA that benefits the firm versus CPA that represents a form of CEO opportunism (Greiner et al., Reference Greiner, Kim and Cordon Thor2023b). Relying on upper echelons theory (UET), we posit five hypotheses regarding the direct relationship between CEO personality and firm CPA that is more opportunistic in nature. To test these hypotheses, we rely on the research of Yarkoni (Reference Yarkoni2010) and Harrison et al. (Reference Harrison, Thurgood, Boivie and Pfarrer2019) to measure CEO personality from quarterly earnings conference calls that occurred in 2011 for S&P 500 Industrial firms (Rogers, Reference Rogers2000). We then combined this analysis with data regarding the CPA of those firms, as well as archival data on the firms’ operations and performance. Then, for our final hypotheses, we test a potential boundary condition that moderates the ability of CEOs to engage in opportunistic CPA and managerial discretion (Hadani et al., Reference Hadani, Dahan and Doh2015). On conducting empirical analysis of our data, we find support for most of these hypotheses.

This research contributes to management research in at least three ways. First, it adds nuance to management research into UET, identifying a heretofore untested input, CEO personality as measured by the Big Five traits, and linked it to a previously untested output, CPA (Hambrick, Reference Hambrick2007). Second, it contributes to the stream of research in the management literature into the antecedents to non-market activities and particularly CPA (Combs et al., Reference Combs, Gentry, Lux, Jaskiewicz and Crook2020, Hadani and Coombes, Reference Hadani and Coombes2015, Lawton et al., Reference Lawton, McGuire and Rajwani2013, Lux et al., Reference Lux, Crook and Woehr2011, Hillman et al., Reference Hillman, Keim and Schuler2004). Third, it contributes to a growing stream of research exploring the impact on firm outcomes of different traits of CEOs, including their narcissism (Al-Shammari et al., Reference Al-Shammari, Rasheed and Al-Shammari2019, Al-Shammari et al., Al-Shammari et al., Reference Al-Shammari, Rasheed and Banerjee2021, Buchholz et al., Reference Buchholz, Lopatta and Maas2020, Chatterjee and Hambrick, Reference Chatterjee and Hambrick2007, Cragun et al., Reference Cragun, Olsen and Wright2020, Engelen et al., Reference Engelen, Neumann and Schmidt2016, Gerstner et al., Reference Gerstner, Konig, Enders and Hambrick2013, Greiner et al., Reference Greiner, Kim and Cordon Thor2023b), their hubris (Arena et al., Reference Arena, Michelon and Trojanowski2018, Hayward and Hambrick, Reference Hayward and Hambrick1997, Hiller and Hambrick, Reference Hiller and Hambrick2005, Li and Tang, Reference Li and Tang2010, McManus, Reference McManus2018, Tang et al., Reference Tang, Qian, Chen and Shen2015, Zhang et al., Reference Zhang, Ren, Chen, Li and Yin2020), their values (Greiner et al., Reference Greiner, Kim and Cordon Thor2023a, Briscoe et al., Reference Briscoe, Chin and Hambrick2014), and either their political ideology (Chin et al., Reference Chin, Hambrick and Treviño2013, Chin and Semadeni, Reference Chin and Semadeni2017, Gupta et al., Reference Gupta, Briscoe and Hambrick2018, Gupta et al., Reference Gupta, Fung and Murphy2020) or their organization’s (Gupta and Briscoe, Reference Gupta and Briscoe2019, Gupta and Wowak, Reference Gupta and Wowak2017). In this way, this article makes a significant contribution to management research.

Theory

Antecedents to CPA

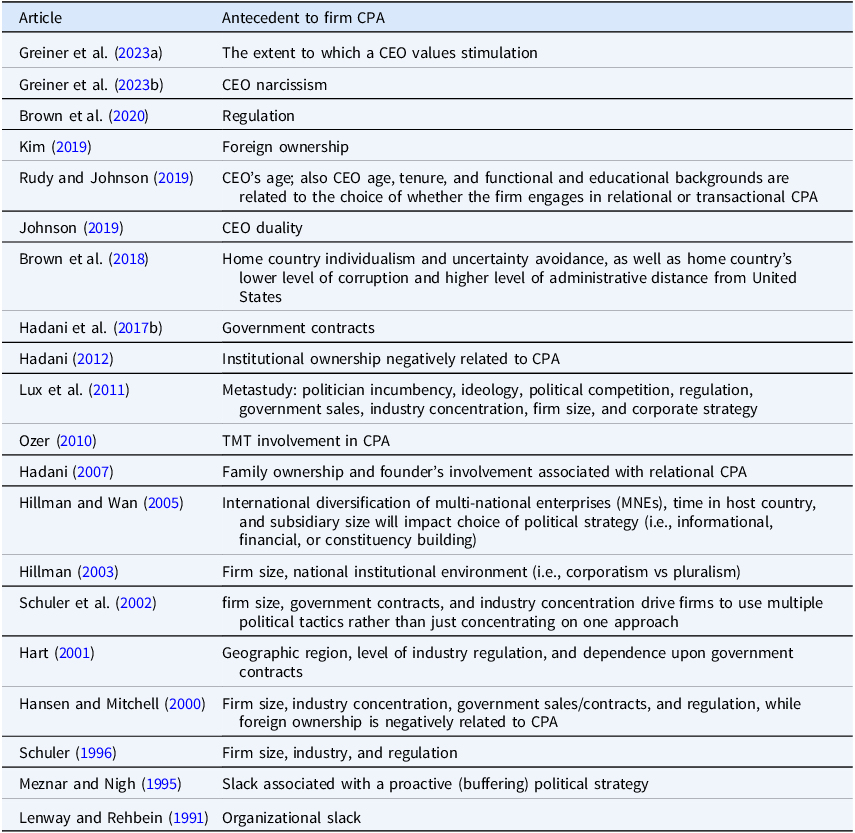

One of the motives for CPA is the widespread belief that it can be a good investment for firms (Lux et al., Reference Lux, Crook and Woehr2011, Mellahi et al., Reference Mellahi, Frynas, Sun and Siegel2016, Hillman et al., Reference Hillman, Keim and Schuler2004). Yet, most firms do not engage in CPA (Ansolabehere et al., Reference Ansolabehere, de Figueiredo and Snyder2003), raising the question of what differentiates politically active firms from those that are not. As Lawton et al. (Reference Lawton, McGuire and Rajwani2013) pointed out, there must be some unidentified antecedents that drive firms to engage in CPA. In table 1, we detail the findings of prior research into this question, which has focused on firms’ material interest, size, and issue salience as antecedents to CPA (Oliver and Holzinger, Reference Oliver and Holzinger2008). In a meta-analysis, Lux et al. (Reference Lux, Crook and Woehr2011) found that institutional-, market industry-, and firm-level factors had only a limited ability to explain firm CPA. None of these antecedents, however, included CEO characteristics, and the authors suggested that future research should examine the effect of top management team characteristics on CPA (Lux et al., Reference Lux, Crook and Woehr2011). Thus, current research into CPA ignores the insights provided by UET, namely, that top manager values influence firm behavior (Abatecola and Cristofaro, Reference Abatecola and Cristofaro2018, Hambrick, Reference Hambrick2007).

Table 1. Prior research identifying CPA antecedents

Upper echelons theory

First proposed by Hambrick and Mason (Reference Hambrick and Mason1984), UET has evolved into an active field of research (Abatecola and Cristofaro, Reference Abatecola and Cristofaro2018). The integrated model that has emerged from this research breaks down top management team (TMT) decision-making into several parts (Abatecola and Cristofaro, Reference Abatecola and Cristofaro2018, Hambrick, Reference Hambrick2007). Drawing on contingency theory (Child, Reference Child1972), UET starts from the idea that to establish fit with their firm’s environment managers must gather, interpret, and respond to incoming data (Tang et al., Reference Tang, Qian, Chen and Shen2015). Although early UET research focused on the top management team to investigate the results of this process, recent research has focused on the individual characteristics of firm CEOs (Bilgili et al., Reference Bilgili, Campbell, O’Leary-Kelly, Ellstrand and Johnson2020, Chatterjee and Hambrick, Reference Chatterjee and Hambrick2007, Garcia-Sanchez et al., Reference Garcia-Sanchez, Aibar-Guzman, Aibar-Guzman and Azevedo2020, Momtaz, Reference Momtaz2020, Resick et al., Reference Resick, Whitman, Weingarden and Hiller2009), given their leadership role. CEO assessments are influenced by their personal values, experiences, and personalities (Hambrick, Reference Hambrick2007) since, based on the executives’ bounded rationality, these individual characteristics determine where the executives direct their attention and which options will most appeal to them (Abatecola and Cristofaro, Reference Abatecola and Cristofaro2018, Benischke et al., Reference Benischke, Martin and Glaser2019, Petrenko et al., Reference Petrenko, Aime, Ridge and Hill2016). These assessments are centrally important since they then lead the executives to direct the organization to take actions in response (Julian and Ofori-Dankwa, Reference Julian and Ofori-Dankwa2008, Obstfeld et al., Reference Obstfeld, Sutcliffe and Weick2005).

CEO personality and CPA

One important CEO antecedent to CPA that has received relatively little attention among scholars is CEO personality (Hillman et al., Reference Hillman, Keim and Schuler2004, Lawton et al., Reference Lawton, McGuire and Rajwani2013). We have reason to think that this is an important characteristic to consider. Ansolabehere et al. (Reference Ansolabehere, de Figueiredo and Snyder2003) explained political participation as a form of consumption. Just as some corporate social responsibility (CSR) has been shown to be motivated by CEOs’ need for recognition (Petrenko et al., Reference Petrenko, Aime, Ridge and Hill2016), so too does political participation bring personal benefits to the firm CEO. The most potent benefit is the personal satisfaction of supporting candidates and causes the donor to find ideologically congenial (Gimpel et al., Reference Gimpel, Lee and Pearson-Merkowitz2008). Indeed, as Hart (Reference Hart2004) pointed out, when a CEO has strong ideological beliefs and takes an interest in politics, the firm’s positions will likely mirror the CEO’s ideology. Thus, just as CEOs might seek to access firm resources to enjoy the personal benefits associated with CSR, so too might they advocate CPA to enjoy the personal satisfaction Ansolabehere et al. (Reference Ansolabehere, de Figueiredo and Snyder2003) described.

UET predicts that CEOs’ cognitive biases will affect organizational outcomes. One of the fundamental cognitive processes associated with decision-making is an individual’s personality (Benischke et al., Reference Benischke, Martin and Glaser2019, Jiang et al., Reference Jiang, Wang, Chu and Zheng2019). Research has shown personality to be highly stable throughout an individual’s lifetime, and indeed personality appears to be largely heritable (Gerber et al., Reference Gerber, Huber, Doherty and Dowling2011). Furthermore, Gow et al. (Reference Gow, Kaplan, Larcker and Zakolyukina2016) showed that CEO personality is related to a number of specific firm outcomes, such as R&D intensity, firm growth, and performance. In meta-analyses, Judge et al. (Reference Judge, Bono, Ilies and Gerhardt2002) showed that personality is highly related to leadership, and Bell (Reference Bell2007) found personality related to team effectiveness. This is just a partial list of the relationships research has established with personality, clearly showing that personality has important consequences (Ozer and Benet-Martinez, Reference Ozer and Benet-Martinez2006). Particularly relevant to this research, personality appears to form the basis of an individual’s political ideology (Kam and Palmer, Reference Kam and Palmer2008). Indeed, personality is a more important predictor of political ideology than demographic variables such as age, gender, education, and socioeconomic status (Blais and Pruysers, Reference Blais and Pruysers2017). As well, political science research has already established that one’s decision to become politically involved is related to personality traits (Cooper et al., Reference Cooper, Golden and Socha2013, Mondak et al., Reference Mondak, Hibbing, Canache, Seligson and Anderson2010). We thus have a strong basis to assume that CEO personality affects CPA.

Psychology has developed a tool that is widely accepted (Gerber et al., Reference Gerber, Huber, Doherty and Dowling2011) and is earning greater currency in other fields including economics (Gow et al., Reference Gow, Kaplan, Larcker and Zakolyukina2016), political science (Cooper et al., Reference Cooper, Golden and Socha2013), and management (Benischke et al., Reference Benischke, Martin and Glaser2019): the five-factor model of personality (Abatecola and Cristofaro, Reference Abatecola and Cristofaro2018). Sometimes referred to as the “Big Five,” these five personality traits—agreeableness, conscientiousness, extraversion, neuroticism, and openness to experience—are seen as “broad domains, collectively organizing and summarizing the vast majority of subsidiary traits” (Mondak et al., Reference Mondak, Hibbing, Canache, Seligson and Anderson2010: 86). These personality traits have been found to be predictive across nations, cultures, and languages (Mondak et al., Reference Mondak, Hibbing, Canache, Seligson and Anderson2010). To understand how these personality dimensions can affect CPA, we now unpack some of the characteristics of ideological CPA.

Ideological CPA

Williamson (Reference Williamson1985) famously defined opportunism as “self-interest seeking with guile” (30). We argue that ideological CPA (iCPA) is opportunistic because they bring some personal benefit to the CEO rather than being focused on delivering results for the firm. Ideological CPA features several distinguishing and relevant characteristics. The three characteristics we identify that are inherent in ideological CPA as opposed to other forms of CPA are that it is personally satisfying to the CEO, it generates unnecessary conflict, and it is less effective in delivering results for the firm.

For instance, ideological CPA can be considered opportunistic when it delivers certain personal benefits to the CEOs (Skaife and Werner, Reference Skaife and Werner2020). In effect, the CEO who feels entitled to behave opportunistically might view firm resources available for CPA as a means to satisfy his or her personal political goals, goals which may or may not also benefit the firm (Greiner and Lee, Reference Greiner and Lee2020). For instance, in supporting candidates who agree with them ideologically, CEOs receive a consumption benefit that manifests itself in the form of excitement and satisfaction from supporting their preferred contenders and issues (Aggarwal et al., Reference Aggarwal, Meschke and Wang2012). Ideological “purity” or “extremism” motivates political action more than ideological balance and moderation (Valentino et al., Reference Valentino, Brader, Groenendyk, Gregorowicz and Hutchings2011, Thomsen, Reference Thomsen2014). Indeed, top managers seem to be aware of this distinction, since when they make contributions from corporate funds, those contributions tend to be aimed at moderate incumbents. In contrast, however, when executives make contributions with their own personal funds, those contributions tend to favor candidates who reflect the CEOs’ personal ideology (Burris, Reference Burris2001).

Second, ideological CPA will tend to increase conflict both internal and external to the firm. Conflict is inherent to American politics with its winner-take-all approach (Baumgartner et al., Reference Baumgartner, Berry, Hojnacki, Leech and Kimball2009, den Hond et al., Reference den Hond, Rehbein, de Bakker and Lankveld2014). A CEO using firm resources to benefit candidates and causes other stakeholders might not support can create conflict with people of differing opinions (Brandt et al., Reference Brandt, Reyna, Chambers, Crawford and Wetherell2014). This ideological conflict will affect the firm relations both with its employees (Bermiss and McDonald, Reference Bermiss and McDonald2018) and consumers (Sandıkcı and Ekici, Reference Sandıkcı and Ekici2009).

Third, an ideological CPA is likely less effective at addressing the firm’s interests than a CPA that takes a non-ideological approach and is more focused on supporting moderate incumbents. Changing policy requires that firms build coalitions of politicians until they gain majority support. Majorities are achieved by wooing undecided politicians to your point of view, not by attacking or rewarding politicians who already have hardened positions (Stratmann, Reference Stratmann1991). The ideal targets of such CPA efforts are politicians who are persuadable, neither supportive of nor opposed to the business’s position. In other words, those who are not driven by ideology, since that is where the business will be able to turn undecided politicians into supporters, hopefully resulting in a majority. Indeed, Greiner and Lee (Reference Greiner and Lee2020) found that firms whose CPA tends to support more ideologically extreme candidates tend to have lower performance and further found evidence that those firms tend to have higher potential for opportunism on the part of the CEO. Thus, ideological CPA is likely opportunistic, conflictual, and ineffective, characteristics that are relevant to CEO personality.

Hypotheses

Agreeableness and CPA. We argue that the relationship between this personality trait and CPA is driven by the conflict that is characteristic of ideological CPA. “Agreeableness represents the degree to which someone shows personal warmth, a preference for cooperation over competition, and trust and acceptance of others” (Peterson et al., Reference Peterson, Smith, Martorana and Owens2003: 799). More useful for our analysis, however, is the description used for someone who is low in agreeableness or high in antagonism (McCrae and Costa, Reference McCrae and Costa1987). Such individuals have been described as Machiavellian, aggressive, stubborn, and always setting themselves against others (McCrae and Costa, Reference McCrae and Costa1987). Conflict is the nature of America’s “winner-take-all” political system (Reilly and Reynolds, Reference Reilly, Reynolds and Research Council2000), and this conflict is between the two sides each advocating their own ideology (Abramowitz and Saunders, Reference Abramowitz and Saunders2006). Such conflict inherently appeals to disagreeable CEOs and repels agreeable ones. Disagreeable CEOs inherently enjoy conflict with other people who hold different opinions and are likely to view politics, as they are likely to view many other realms, in warlike terms of battle, struggle, and combat. In a two-party system, one side’s gains are the other’s losses which produces a competitive arena that aligns with a disagreeable CEO’s tendency to view social interactions in terms of competition, victory, and defeat. However, agreeable individuals have been described as wishing to avoid conflict (Mondak and Halperin, Reference Mondak and Halperin2008) and are likely to look for compromise solutions to seemingly intractable disputes, not as ideological conflicts. Finding the partisan nature of extant American politics distasteful, agreeable CEOs are likely to show little interest in it and spend Political Action Committee (PAC) funds in an ideological fashion. Thus, CEOs who are low in agreeableness are likely to enjoy the ideological conflict inherent in politics and might view firm resources as an opportunity to engage in this activity, while agreeable CEOs will be repelled and thus not spend funds in an ideological way.

Hypothesis 1: CEO agreeableness will be related to lower levels of ideological CPA

Conscientiousness and CPA. We argue that this relationship is based on the opportunistic nature of ideological CPA. According to McCrae and Costa (Reference McCrae and Costa1987), this conscientiousness is characteristic of people who are habitually careful and self-disciplined and adhere scrupulously to a moral code (88). Such individuals demonstrate prudence or “concern with following established rules” (Peterson et al., Reference Peterson, Smith, Martorana and Owens2003: 798). Such carefulness and scrupulousness will likely direct such people to less opportunistic behavior, and thus less iCPA. Opportunism is against the rules and certainly a violation of the trust of the shareholders. Using firm resources to generate perquisites for the CEO diverts those resources from efforts that could produce additional value for the shareholders. More particularly, with ideological CPA, the perquisites received by the CEO could be the ideological consumption benefit of ideological CPA (Aggarwal et al., Reference Aggarwal, Meschke and Wang2012, Greiner and Lee, Reference Greiner and Lee2020). A conscientious CEO will desire to follow the rules and general expectations of the position, such as to scrupulously work to provide a return on investment for the shareholders, the task the CEO was hired to do (Friedman, Reference Friedman1970). As well, a careful CEO will avoid activities that might appear to be opportunistic, and iCPA can be. Furthermore, the discipline inherent in conscientiousness enables such a CEO to avoid the temptation to engage in such opportunism. A careless, indifferent CEO will not be inclined to keep to such scruples and, indeed, is unlikely to be deterred by them. Thus, we expect that a conscientious CEO would be less likely to take advantage of firm resources to engage in personally satisfying ideological CPA, leading us to our second hypothesis:

Hypothesis 2: CEO conscientiousness will be related to lower levels of ideological CPA

Extraversion and CPA. We argue that this relationship is based on the conflictual nature of ideological CPA. Extraversion is the personality trait most strongly associated with leadership, largely because these individuals are more interactive and energetic and, particularly relevant for us here, are more forceful in communicating their opinions (Judge et al., Reference Judge, Bono, Ilies and Gerhardt2002). Extraverted individuals enjoy expressing and acting on their views, particularly in debatable and controversial arenas. The conflictual and contentious nature of politics features sharp disagreement, disputation, and debate. Indeed, extraversion is quite different from agreeableness, and we would characterize extraversion as related to self-expression for gaining dominance in conflict (Grant et al., Reference Grant, Gino and Hofmann2011), while agreeableness is related to interpersonal tendencies for cooperation (Blake et al., Reference Blake, Luu, Petrenko, Gardner, Moergen and Ezerins2022). As a result, one can be highly extraverted and highly agreeable, as well as being highly extraverted with low agreeableness. Political conflict thus lures extraverted CEOs to participate as they desire to see their viewpoints gain the ascendency, if not by their expressing their views directly, then through supporting those that do. Indeed, a major characteristic associated with extraversion is dominance (Judge et al., Reference Judge, Bono, Ilies and Gerhardt2002, McCrae and Costa, Reference McCrae and Costa1987). Given their interest in leading, extraverted CEOs are likely to use a wide range of means toward supporting political figures with whose ideology they agree. The action-oriented nature of extraverts compels such CEOs to use what means are at hand, such as corporate PACs, as a means of expressing and promoting their values in contestable fields such as partisan politics. Ideological CPA is one such means, and so extroverted CEOs are likely to engage their firms in more of it. On the other hand, introverts are more reticent, more likely to keep their ideological views to themselves, as they do other views, and thus are less likely to take public or visible action to support ideological political candidates, such as through iCPA.

Hypothesis 3: CEO extraversion will be related to higher levels of ideological CPA

Neuroticism and CPA. We argue for a relationship between neuroticism and ideological CPA based on the conflict and ineffectiveness inherent in such CPA. Neuroticism is often viewed as a negative trait, especially in contrast to its counterpart emotional stability (Nga and Shamuganathan, Reference Nga and Shamuganathan2010). While “emotional stability is associated with optimism, self-confidence, self-assurance, decisiveness and success” (Gow et al., Reference Gow, Kaplan, Larcker and Zakolyukina2016: 6), neuroticism has been defined by such terms as worrying, insecure, self-conscious, and temperamental, with its central tendency being negative affect (McCrae and Costa, Reference McCrae and Costa1987).

Being of a less stable temperament to begin with, neurotic CEOs are likely to shy away from conflict if they can avoid doing so. Conflict and contention consume mental resources and can so drain both cognitive and emotional energy from an already overloaded consciousness. Activities that deplete already scarce resources will be seen in threatening terms, particularly by a CEO pre-sensitized to threats, and are thus seen as distractions to shun. Given that iCPA is inherently conflictual and thus consumptive of resources in short supply for neurotics, such CEOs are unlikely to pursue it. Their aversion to the associated costs of dispute and controversy makes conflictual activities such as iCPA unappealing. Further associated with this and in contrast, where more self-assured emotionally stable CEOs might see CPA as an excuse to behave opportunistically, neurotic ones will see such behavior as risky. iCPA courts potentially negative media attention as well as creates potential pushback from shareholders, thus increasing cognitively draining conflict (McDonnell and Werner, Reference McDonnell and Werner2016).

As well, the focus of neurotic CEOs on threats to the business produces an additional effect. Given that actions by politicians can create problems for the business (Baumgartner et al., Reference Baumgartner, Berry, Hojnacki, Leech and Kimball2009, Shaffer, Reference Shaffer1995), their priority will be to focus on types of CPA that are likely to be most effective for the firm in addressing such threats. Neurotics CEOs are more likely to perceive threats as unmanageable and will thus strongly prefer types of CPA that would directly address them, rather than a personal pursuit. Consequently, they are less interested in CPA that merely satisfies an ideological interest and thus is not primarily direction at protecting the business from such risks. As a result, a neurotic CEO will be less likely to be involved in ideological CPA.

Hypothesis 4: CEO neuroticism will be related to lower levels of ideological CPA

Openness to experience and CPA. Finally, we posit a relationship between openness and ideological CPA based on its conflictual nature and ineffectiveness. Individuals with the final personality trait, openness to experience, are “original, imaginative, having broad interests, and daring” (McCrae and Costa, Reference McCrae and Costa1987: 87). Such individuals crave new and exciting experiences (Peterson et al., Reference Peterson, Smith, Martorana and Owens2003). While research in general has shown that executives tend to be uncomfortable with politics and government (Pearce et al., Reference Pearce, De Castro and Guillén2008, Shaffer, Reference Shaffer1995), ideologically driven politics can be exciting due to its conflict over philosophical concerns regarding preferred values and ideals on societal organization and resource distribution (Ansolabehere et al., Reference Ansolabehere, de Figueiredo and Snyder2003), an intellectually stimulating activity to which people who are open to experience might be drawn. Indeed, openness has been linked to the neurotransmitter dopamine (Zajenkowski et al., Reference Zajenkowski, Jonason, Leniarska and Kozakiewicz2020), which is associated with sensation seeking, or looking for excitement (Derringer et al., Reference Derringer, Krueger, Dick, Saccone, Grucza, Agrawal, Lin, Almasy, Edenberg, Foroud, Nurnberger, Hesselbrock, Kramer, Kuperman, Porjesz, Schuckit and Bierut2010), and disputation and debate can be emotionally arousing and stimulating. As well, research has also found that openness to experience consistently predicts an individual’s political ideology (Joly et al., Reference Joly, Hofmans and Loewen2018) likely in part for this reason.

Furthermore, open individuals tend to feel less restricted by rules (Zajenkowski et al., Reference Zajenkowski, Jonason, Leniarska and Kozakiewicz2020), while closed individuals, those with low in openness to experience, tend to value obedience and deference to authority without question (McCrae and Sutin, Reference McCrae, Sutin, Leary and Hoyle2013). Thus, higher openness should be related to CEOs’ propensity to deemphasize the norm that the needs of shareholders be prioritized. In the same vein, open individuals, with their willingness to consider alternative perspectives (McCrae and Sutin, Reference McCrae, Sutin, Leary and Hoyle2013), will likely recognize the needs of various stakeholders, not just shareholders. As such, they may perceive a need to engage in political activities aligned with their personal view of what would better society as a whole even if such activities do not directly contribute to the firm’s bottom line. Thus, this personality trait can create a dynamic where the CEO gets enormous personal satisfaction from the ideological CPA while failing to provide him or her with the caution appropriate for this activity.

Hypothesis 5: CEO openness will be related to higher levels of ideological CPA

Managerial discretion as moderator. Managerial discretion has been defined as the extent to which options are available to managers (Rajagopalan, Reference Rajagopalan1997), both good and bad. Opportunism requires leeway, freedom to act, and existence of choices. Where managerial discretion is low (for reasons independent of shareholders or any interventions), CEOs face low means-end ambiguity and thus will not be able to pursue goals contrary to the interests of the shareholders (Hambrick, Reference Hambrick2007). Where managerial discretion is high, CEOs will have the ability to engage in opportunistic behavior that they prioritize. Therefore, building on the insights of UET as detailed by Finkelstein and Hambrick (Reference Finkelstein and Hambrick1990), we believe managerial discretion could be an important boundary condition limiting the ability of a CEO to impact firm CPA. For instance, where CEOs have higher managerial discretion, they will likely be able to adjust CPA to their desires. However, where the CEO has less discretion due to either firm-level or industry-level factors or both (Li and Tang, Reference Li and Tang2010), that CEO will be less able to divert CPA resources toward their personal priorities.

Since we argue that iCPA is a form of opportunism, based upon the above argumentation, more iCPA will require managerial discretion for CEOs to engage in it. The two personality traits we theorize will result in more iCPA are extraversion and openness. Thus, when CEOs high in these personality traits engage in more iCPA, they are behaving contrary to the objective interests of the shareholders. If these CEOs have low managerial discretion, they will find it harder to behave in this manner (Boyd, Reference Boyd1995, Ozer, Reference Ozer2023, Krause et al., Reference Krause, Semadeni and Cannella2014); the opposite is true if they have high managerial discretion. As a result, we argue that CEOs who are more receptive to external change or who are better at representing an internal perspective to the outside are more likely to engage in their preferred form of CPA when they have high levels of managerial discretion.

The above argumentation leads us to our final hypotheses:

Hypothesis 6: Managerial discretion will moderate the relationship between both (a) CEO extraversion and (b) CEO openness with ideological CPA such that higher levels of (a) CEO extraversion and (b) CEO openness will be related to higher levels of ideological CPA when managerial discretion is high.

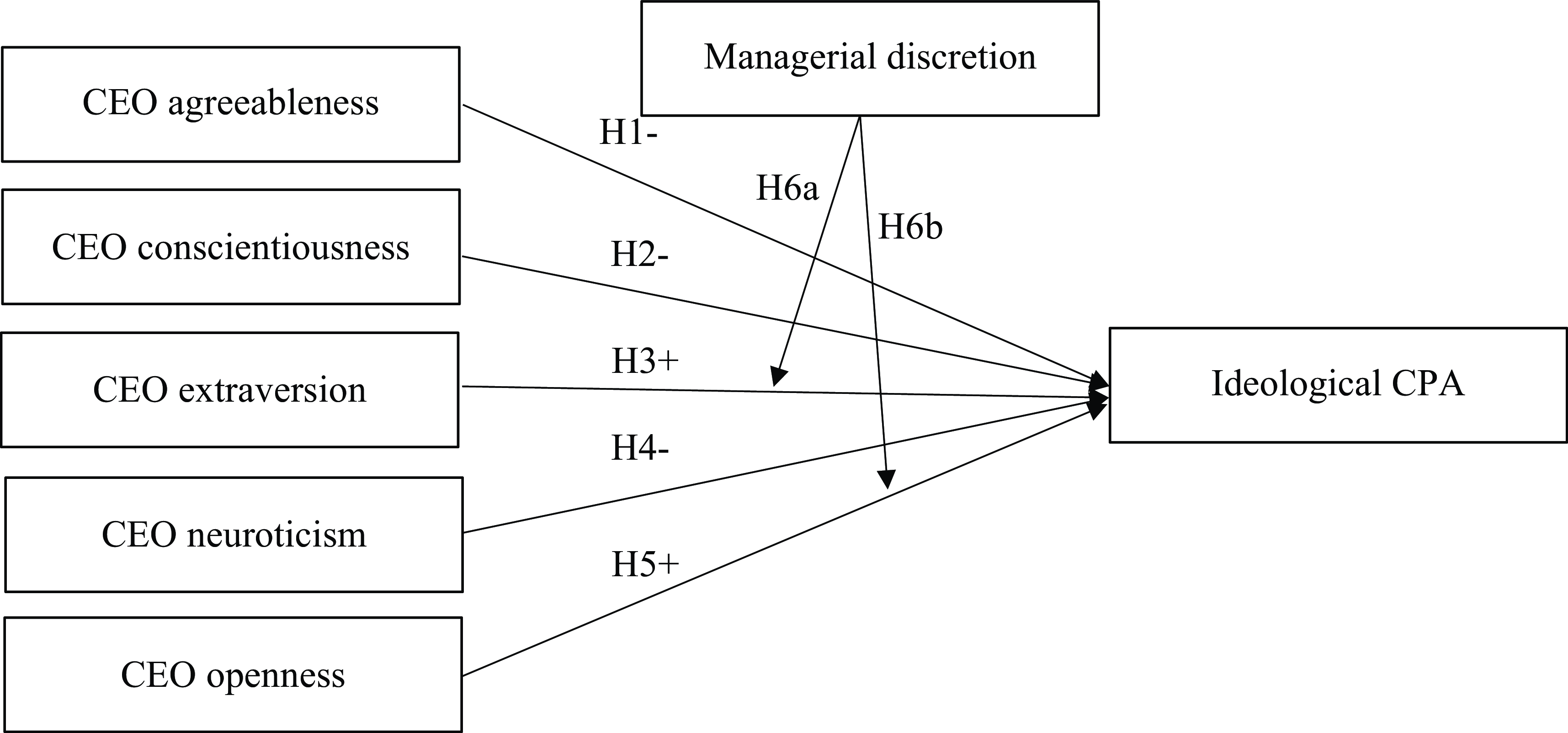

In figure 1, we present our conceptual model.

Figure 1. Conceptual model.

Methods

The data

Interestingly, research using the five-factor model to analyze CEO personality has been slow to gain traction. Early research into personality traits was conducted using questionnaires with participant self-assessment (McCrae & Costa, Reference McCrae, Costa and Busch1986). However, CEOs are “notoriously unwilling to submit themselves to scholarly poking and probing” (Hambrick, Reference Hambrick2007: 337). As a result, more comprehensive research on CEO personality would require the development of tools that can accomplish such analysis without relying on the responses from top executives (Harrison et al., Reference Harrison, Thurgood, Boivie and Pfarrer2019). Recently, methods of determining personality through computer analysis of texts has come into wider use (Yarkoni, Reference Yarkoni2010, Harrison et al., Reference Harrison, Thurgood, Boivie and Pfarrer2019, Benischke et al., Reference Benischke, Martin and Glaser2019, Abatecola and Cristofaro, Reference Abatecola and Cristofaro2018). Such analysis has been applied to transcripts of the question and answer sections of quarterly earnings conference calls (Malhotra et al., Reference Malhotra, Reus, Peng Cheng and Roelofsen2018). The question and answer sections are particularly useful for analyzing CEO personality because, unlike the initial presentation section, they are largely unscripted (Matsumoto et al., Reference Matsumoto, Pronk and Roelofsen2011). Following recent literature, we engage in linguistic text analysis of CEO comments during the question and answer sections of quarterly earnings conference calls from 2014 for 329 publicly traded firms from the S&P 500 for which we had complete records. Then, following Greiner and Lee (Reference Greiner and Lee2020), we combined this data with other archival data regarding each firm’s CPA for the ten-year period of 2011 until 2020, ensuring that the CEO for each year was the same CEO for whom we conducted the personality analysis. Finally, we combined that data with data from the Compustat, Execucomp, and KLD/MSCI databases to create our overall database of 63,142 records of firm-candidate combinations over the five election cycles that occurred during that period. We standardized all our variables except for our dummy variables and the iCPA dependent variable, which was instead log-transformed to address skewness.

Variables

Dependent variables. To thoroughly test our hypotheses, we propose a measure aiming to capture whether the CPA is oriented to benefit the firm or the CEO’s personal agenda, which we call ideological CPA (iCPA). Broadly, individuals, including those guiding PACs, will make political contributions for two reasons, either to gain access to politicians or to receive the consumption benefits of such activism (Ansolabehere et al., Reference Ansolabehere, de Figueiredo and Snyder2003). Access is a euphemism for giving enough money that the politicians are willing to dedicate some of their limited time to consider the donor’s arguments (Austen-Smith, Reference Austen-Smith1995, Hadani et al., Reference Hadani, Bonardi and Dahan2017a, Hadani et al., Reference Hadani, Doh and Schneider2018, Apollonio and La Raja, Reference Apollonio and La Raja2004). Prioritizing political donors is one way politicians can distinguish between those worth paying attention to and those whose input can be deemphasized. Making contributions for the purpose of gaining access to politicians is a form of non-opportunistic CPA, since it enables CEOs to make their case for policies that will benefit the firm, and research has shown that this is one of the most effective forms of CPA (Lord, Reference Lord2000). Typically, contributions aimed at gaining access will be given to more moderate politicians, since extreme ideologues located at the ideological margins of Congress will be less effective at shepherding policy through Congress (Burris, Reference Burris2001, Baumgartner et al., Reference Baumgartner, Berry, Hojnacki, Leech and Kimball2009, Hall and Deardorff, Reference Hall and Deardorff2006). On the other hand, contributions aimed at generating a consumption benefit could be characterized as perquisites secured by the CEOs. These contributions will likely go to more ideologically extreme candidates (Gimpel et al., Reference Gimpel, Lee and Pearson-Merkowitz2008) since ideology is a strong motivator (Bermiss and McDonald, Reference Bermiss and McDonald2018, Boone and Özcan, Reference Boone and Özcan2014, Chin et al., Reference Chin, Hambrick and Treviño2013). Our dependent variable, iCPA, is characterized by contributions to more ideologically extreme candidates. If the personal benefit individuals get from political activism is the satisfaction of supporting candidates who agree with the person’s ideology (Gimpel et al., Reference Gimpel, Lee and Pearson-Merkowitz2008, Ansolabehere et al., Reference Ansolabehere, de Figueiredo and Snyder2003), then there should be greater satisfaction generated by supporting more extreme candidates than less extreme ones.

Based on our dependent variable, each observation represents one relationship between a firm’s PAC and a candidate for Congress. For each observation, the firm’s variables will not change, while the amount contributed to that candidate and the candidate’s ideology will. To measure the ideology of the members of Congress receiving donations, we used an objective measure is well accepted in political science research: the NOMINATE dimension 2 scores from Voteview.com (Lewis et al., Reference Lewis, Poole, Rosenthal, Boche, Rudkin and Sonnet2018). This score, which is relied upon in scholarship, pedagogy, and journalism (Boche et al., Reference Boche, Lewis, Rudkin and Sonnet2018, Bonica, Reference Bonica2018), is calculated based on the member of Congress’s voting record (Boche et al., Reference Boche, Lewis, Rudkin and Sonnet2018). The second dimension that we rely upon addresses social issues, as opposed to the first that focuses on economic policy (Boche et al., Reference Boche, Lewis, Rudkin and Sonnet2018). Given that there might be a basis to argue that the CEO believes the firm might benefit from CPA supporting candidates who have extreme positions on economic issues, there is less basis to argue that the firm will benefit from contributions aimed at supporting candidates who take extreme positions on social issues. As a result, we argue that CPA aimed at politicians who take extreme positions on social issues would tend to be more opportunistic.

This scale is reported as follows: a number close to zero represents moderate ideology, while negative numbers describe liberal ideology, and positive ones are conservative. As a result, to develop our measure of ideological extremism, we simply calculated the absolute value of this measure. The resulting variable has a minimum value of zero and a maximum value of 0.994. Next, we multiplied the resulting number for each recipient of the contributions by the amount received from each firm. In this way, we account for circumstances where a firm might make very large contributions to more moderate candidates and smaller contributions to more extreme ones, and vice versa. Since a firm might make multiple contributions to a single candidate and thus represent multiple observations, we combined all the contributions from each firm to each candidate. Thus, if the firm made multiple contributions in the electoral cycle to a single candidate, something we saw in our data, we would combine those contributions into one observation. As a result, a higher contribution to a more extreme candidate versus a smaller one results in a larger number in our measure, and our level of analysis is at the firm-candidate level. We log-transformed this variable to minimize potential skewness in the data (Oh et al., Reference Oh, Chang and Kim2016). The range of this variable is from 0 to 9.824.

Independent variables. For our independent variable, we calculated the level of CEO personality with respect to each of the five-factor model traits: agreeableness, conscientiousness, extraversion, neuroticism, and openness. We relied on the Linguistic Inquiry and Word Count (LIWC) 2001 dictionary (Pennebaker et al., Reference Pennebaker, Francis and Booth2001) as analyzed by the LIWC text analysis program (Pennebaker et al., Reference Pennebaker, Booth, Boyd and Francis2015), which has been validated and widely used in research (Pennebaker et al., Reference Pennebaker, Mehl and Niederhoffer2003, Pennebaker and King, Reference Pennebaker and King1999, Edwards and Holtzman, Reference Edwards and Holtzman2017, Carey et al., Reference Carey, Brucks, Küfner, Holtzman, große Deters, Back, Donnellan, Pennebaker and Mehl2015). The LIWC dictionary includes over 2200 words and word stems that are associated with one or more of the seventy-two dimensions of word use (Pennebaker and King, Reference Pennebaker and King1999). The program analyzes each text based on the count of each word or word stem in the dictionary as a percentage of the total words in the text. The software then aggregates these results by category. Yarkoni (Reference Yarkoni2010) had conducted an exploratory factor analysis using the LIWC 2001 program to analyze the word use of 576 blogs. The blog posts addressed a wide variety of subjects with the only requirement being that they were noncommercial in nature, thus helping improve the generalizability of his analysis. The writers of those blogs completed a questionnaire that included the International Personality Item Pool (IPIP) fifty-item representation of the NEO-FFI measure of the Big Five personality traits (Goldberg et al., Reference Goldberg, Johnson, Eber, Hogan, Ashton, Cloninger and Gough2006). By associating the personality assessments with the results of the blog word-use analysis, Yarkoni (Reference Yarkoni2010) was able to determine which LIWC categories were associated with each personality trait. Scholars have relied on quite similar approaches to measure the personality of chief marketing officers (Winkler et al., Reference Winkler, Rieger and Engelen2020), and the relationship between personality and the risk tolerance of CEOs and Chief Financial Officers (CFOs) (Hrazdil et al., Reference Hrazdil, Novak, Rogo, Wiedman and Zhang2020), as well as the potential for loan default (Netzer et al., Reference Netzer, Lemaire and Herzenstein2019). Indeed, in a review article, Eichstaedt et al. (Reference Eichstaedt, Kern, Yaden, Schwartz, Giorgi, Park, Hagan, Tobolsky, Smith, Buffone, Iwry, Seligman and Ungar2021) argued in a review article in Psychological Methods that the ideal method for analyzing texts is to combine the open and closed vocabulary approaches as did Yarkoni (Reference Yarkoni2010), and Giorgi et al. (Reference Giorgi, Nguyen, Eichstaedt, Kern, Yaden, Kosinski, Seligman, Ungar, Andrew, Schwartz and Park2021) found that “[m]any studies have identified language as a reliable source of personality cues” (4), while in a metanalysis, Ahmed and Feist, Reference Ahmed and Feist2021) found that “[l]inguistic analysis has become a technique for personality researchers to assess personality in a less biased and more reliable way” (3). Thus, unlike in the management sciences where researchers still rely upon subjective personality assessments (Benischke et al., Reference Benischke, Martin and Glaser2019), psychological research appears to prefer textual analysis, which is the approach we relied upon this this article. For this reason, Yarkoni’s report on the relationship between LIWC categories and each personality trait formed the basis for our analysis.

First, we analyzed the transcripts of the CEOs’ comments in the quarterly earnings conference calls, which provided the percentages of word use associated with each of the seventy-two word-use dimensions identified in the LIWC 2001 dictionary. Next, from these results we calculated five composite variables, one for each personality trait. To calculate these composite variables, we relied on a weighted sum scores approach (DiStefano et al., Reference DiStefano, Zhu and Mîndrilã2009), which has been shown to be superior to other methods of generating variables (Grice and Harris, Reference Grice and Harris1998). This calculation involves multiplying the word use associated with each LIWC dimension associated with each personality trait by the factor loading Yarkoni (Reference Yarkoni2010) found to be associated with that trait. Although not all seventy-two LIWC dimensions were related to each personality trait, each trait was associated with a large number of dimensions. Agreeableness was associated with thirty-three dimensions, conscientiousness with forty-one, extraversion with forty-two, neuroticism with thirty-four, and openness had the largest number of associations at 51. Then, we summed the results of those multiplications to generate each trait’s composite variable (DiStefano et al., Reference DiStefano, Zhu and Mîndrilã2009, Grice and Harris, Reference Grice and Harris1998). To determine the reliability of our measures, we calculated the McDonald’s omega for each one (Dunn et al., Reference Dunn, Baguley and Brunsden2014, McDonald, Reference McDonald1999, Trizano-Hermosilla and Alvarado, Reference Trizano-Hermosilla and Alvarado2016). McDonald’s omega reduces the bias inherent in Cronbach’s alpha when the assumption of tau-equivalence is violated, in other words when the factor loadings of all items in a model are not equal, as is the case with our data. The omega for all five of our personality variables suggests high scale reliability: agreeableness (α = 0.80), conscientiousness (α = 0.78), extraversion (α = 0.84), neuroticism (α = 0.87), and openness (α = 0.87). The resulting independent variables measure the extent to which each CEO exhibits a given level of each personality trait based on analysis of their comments in the 2014 quarterly earnings conference calls (Malhotra et al., Reference Malhotra, Reus, Peng Cheng and Roelofsen2018).

Moderator. To measure managerial discretion, we followed (Finkelstein and Boyd, Reference Finkelstein and Boyd1998), calculating the variable as follows: Munificence (market growth) + R&D intensity (R&D expense/sales) + Advertising intensity (Advertising expense/sales) – Capital intensity (Property, Plant, and Equipment Total (Net)/Employees) + Herfindahl index for the industry (as determined by four-digit SIC code). All elements were standardized before performing the calculation. Munificence was calculated by regressing industry performance over the entire ten-year period and determining the slope of that regression (Boyd, Reference Boyd1990).

Controls

Firm slack. Research has established firm slack as an antecedent to CPA (Adams and Hardwick, Reference Adams and Hardwick1998). We control for this factor by adding the two components that make up slack: absorbed slack and financial slack (Love and Nohria, Reference Love and Nohria2005). We calculated absorbed slack following Love and Nohria (Reference Love and Nohria2005) as the ratio of each firm’s sales, general, and administrative expenses to total sales. For financial slack Kim et al. (Reference Kim, Kim and Lee2008), we calculated financial slack as the ratio of quick assets (cash and marketable securities) to liabilities.

Partisan Voter Index (PVI). The goal of this article is to explore why firms make contributions to certain kinds of politicians and not others. A major driver of that choice should be the expectation on the part of the firm as to which candidate is most likely to be elected and thus be in a position to influence policy. Since the partisan make-up of districts across the country varies such that certain congressional districts and states are more friendly to Democrats or Republicans, it would make sense that most contributions in a more Republican district, for example, would go to Republicans. On the other hand, there are certain districts that are closely divided between the parties, creating a dynamic where it is less clear which candidate is likely to be elected and making the contributions of the PACs higher risk. A good CPA strategy might be to simply contribute to candidates facing easy campaigns since those individuals are more likely to end up in Congress than candidates with tougher races (Hillman et al., Reference Hillman, Keim and Schuler2004). Safer districts tend to be those where one party is so dominant that the nominee of that party is unlikely to lose the election. Thus, where district partisanship is higher, there is less potential for a competitive general election, and thus less need for campaign funds. District partisanship is measured by the Cook Political Report’s PVI report, which calculates the congressional district vote compared to the national vote to show whether each district is more Democratic or more Republican than the nation as a whole and by how much. This is the source of this variable.

Party dummy. The intense polarization of American politics has led Americans to identify with one party or the other (Gupta et al., Reference Gupta, Nadkarni and Mariam2019). Such partisan identification likely plays a major role in the decision by CEOs as to the candidates they support. We controlled for this factor by identifying whether each member of Congress who received a contribution was a Democrat or a Republican. We scored contributions to Democrats and to Republicans with a 1 and a 0, respectively.

Region dummy. Political science research has found that the United States actually has different regions, each with a distinct culture (McKee and Teigen, Reference McKee and Teigen2009). These cultural predispositions will impact the giving decision. As a result, we controlled for this factor with dummy variables for four of the five regions identified by McKee and Teigen (Reference McKee and Teigen2009). For each of the regions except for the Northeast, namely, the Midwest, Pacific, South, and West, there is a 1 in the appropriate column and a 0 otherwise.

Urban population percentage. As with a region, the level of urbanization of a congressional district has a significant impact upon who gets elected to represent that district (McKee and Teigen, Reference McKee and Teigen2009). As a result, decisions to support a candidate are likely also driven by the population density of the candidate’s state (McKee and Teigen, Reference McKee and Teigen2009). The source of this variable is the U.S. census bureau.

Regulation. One of the most consistent findings in CPA research has been the relationship between industry regulation and CPA investment (Hadani and Schuler, Reference Hadani and Schuler2013, Hansen et al., Reference Hansen, Mitchell and Drope2005, Fremeth et al., Reference Fremeth, Holburn and Bergh2016). As a result, firms in highly regulated industries have been shown to be more likely to engage in CPA than those in other industries. We argue, however, that the level of regulation will also impact the nature of the CPA. In other words, where firms must regularly interact with politicians and regulators, those firms will be less likely to support challengers to those politicians than firms without such important industry ties. As a result, we control for this factor with the measure of regulation based on the number of pages of the Federal Register addressing industry regulations as compiled by regdata.org (Al-Ubaydli and McLaughlin, Reference Al-Ubaydli and McLaughlin2014, Clark and Nesbit, Reference Clark and Nesbit2018). For industries with no pages of regulation listed, we entered a zero.

Firm size. Ridge et al. (Reference Ridge, Ingram, Abdurakhmonov and Hasija2019) empirically demonstrated that firm size will impact the amount of firm CPA (see also Combs et al., Reference Combs, Gentry, Lux, Jaskiewicz and Crook2020). As a result, we controlled for the size of each firm, following the literature by including the total assets of the firm as a control variable (Flammer, Reference Flammer2018). We obtained this information from Compustat.

CEO duality. Consistent with the UET (Finkelstein and Boyd, Reference Finkelstein and Boyd1998), we argue the discretion available to the firm’s top managers will impact discrete firm outcomes, including the firm’s CPA. In particular, we argue that where CEOs have more discretion, they are able to bend the CPA to their individual goals in a way more constrained CEOs would be unable to. One source of managerial discretion is CEO duality, the appointment of a single individual as both CEO and board chair (Wangrow et al., Reference Wangrow, Schepker and Barker2015). Scholars expect that where the CEO has both titles, that structure will constrain board independence (Ram et al., Reference Ram Baliga, Charles Moyer and Rao1996). Therefore, if the CEO also serves as the firm’s board chair, we included a dummy variable equaling 1, 0 otherwise. We obtained this information from the Execucomp database.

CEO compensation. Another measure of CEO discretion, as well as an indicator as to the likelihood of a CEO behaving opportunistically, would be the CEO’s level of pay, particularly relative to firm size and when compared with its industry peers. Despite the belief that CEO pay is set by the board, research has shown that it is in fact largely within the control of the CEO (Cornett et al., Reference Cornett, McNutt and Tehranian2009, van Essen et al., Reference van Essen, Otten and Carberry2015). If a CEO tends to behave opportunistically, then we would expect to see that CEO receiving higher compensation relative to the firm’s other employees than a CEO who seeks to distribute the firm’s profits fairly. We control for this factor with a ratio calculated by dividing the CEO’s total compensation by the number of employees at the firm (Werner et al., Reference Werner, Tosi and Gomez-Mejia2005), which we then divide by the 2-digit SIC industry average.

CSR. Corporate social responsibility is the other major form of non-market strategy that firms engage in, and as such, it has been linked to the firm’s choices regarding its political activity (Rehbein and Schuler, Reference Rehbein and Schuler2015, den Hond et al., Reference den Hond, Rehbein, de Bakker and Lankveld2014). As a result, to control for this factor, following prior literature (see, e.g., Flammer, Reference Flammer2018), we added up the strengths identified in the KLD/MSCI database and subtracted from that number any identified CSR concerns.

Contribution total. We wanted to create a level playing field for this research, in effect avoiding a situation where some firms have a greater impact on our results than others simply because of the level of their CPA. In effect, we seek to explore how CEO personality impacts the nature of a firm CPA, not just its quantity. Since some firm PACs make more political contributions than others, we included as a control the total amount of money each firm PAC contributed to all candidates.

Firm performance. A firm with stronger finances will naturally be in a better position to engage in CPA. As a result, we control for this fact with ROA, a variable commonly used in strategy research (Houthoofd and Heene, Reference Houthoofd and Heene1997). The source of this data is Compustat.

Industry dummy. As indicated above, the industry can have an impact on a firm CPA. As a result, we controlled for industry by including dummy variables for each 2-digit SIC code in all our regressions.

Empirical approach

To address potential endogeneity, we used an instrumental variable approach (Reeb et al., Reference Reeb, Sakakibara and Mahmood2012). Following the guidance of Semadeni et al. (Reference Semadeni, Withers and Trevis Certo2014), we select multiple instrumental variables to use in our regressions. Since personality has been shown to relate to job performance, and the CEOs’ job is to operate the firm, we selected a number of archival variables describing firm operations, namely the firms’ sales, general, and administrative expenses (XSGA), their advertising expenses (XAD), and their capital expenditures (PSTKL). Furthermore, while these budget line items may have some impact on the firms’ total level of CPA (Hillman et al., Reference Hillman, Keim and Schuler2004), they will not likely directly impact what kind of CPA the firm engages in. That decision will more likely be within the discretion of the CEO. Thus, these variables achieve the requirements to be instrumental variables, namely, that they are correlated with the explanatory variable but uncorrelated to the dependent variable and the error term (Angrist and Krueger, Reference Angrist and Krueger1991). Thus, we deem these variables an appropriate choice as instruments. We confirmed this decision with the weak instrument test (Olea and Pflueger, Reference Olea and Pflueger2013, Pflueger and Su, Reference Pflueger and Su2015). For all our models, that test resulted in significant results (p < 0.001). Therefore, with these variables identified, we were able to estimate our regressions using the 2-stage least squares (2SLS) approach for our continuous dependent variable iCPA (Schembera, Reference Schembera2018), which is widely used in the literature to address potential endogeneity (Shoham and Lee, Reference Shoham and Lee2018).

Following Shoham and Lee (Reference Shoham and Lee2018), we regressed these instrumental variables on the potentially endogenous independent variables, in this case, CEO personality traits, generating predicted values that are no longer endogenous. In the second stage of regression, this predicted value takes the place of the endogenous independent variable in the regression that tests the hypotheses of interest (Angrist and Krueger, Reference Angrist and Krueger1991, Wooldridge, Reference Wooldridge2012). Based on the Wu-Hausman test of endogeneity (Gupta et al., Reference Gupta, Briscoe and Hambrick2018) we rejected the null hypothesis that the CEO personality variables are exogenous for all our tests except for the regression of CEO extraversion on our dependent variable iCPA, as well as our base regressions which included only our control variables. For those three models, we estimated our regressions using ordinary least squares (OLS). For all the other models, then, we used 2SLS as our estimator which is the most unbiased in such circumstances (Angrist and Krueger, Reference Angrist and Krueger1991).

Results

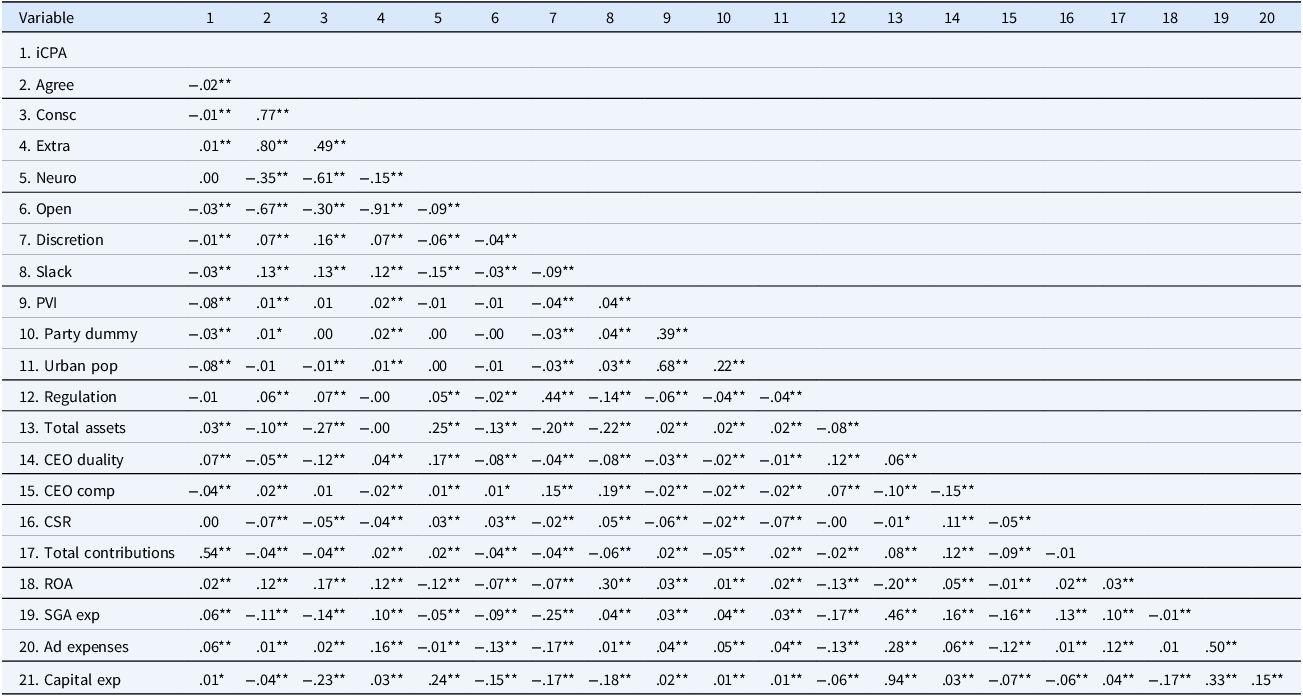

Table 2 displays correlations for our variables. None of our independent variables display correlations of more than 0.3 with any of our control variables. As a result, multicollinearity does not appear to be an issue between our independent variables and controls. On the other hand, our personality trait measures display high correlations with each other. Following the guidance of Kalnins (Reference Kalnins2018), we estimated our regressions by testing only one personality trait at a time. Indeed, when we ran a regression including all five of the personality variables, the results were quite different, suggesting multicollinearity. This approach was validated when we calculated the variance inflation factor (VIF) for each regression. In all cases, the mean VIF was at or below 1.40 (agreeableness, 1.31; conscientiousness, 1.33; extraversion, 1.31; neuroticism, 1.33; openness, 1.31), all far below the conventional threshold of 10 (Oh et al., Reference Oh, Chang and Kim2016).

Table 2. Correlations

*p < 0.05, ** p < 0.01, *** p < 0.001. All variables except dummies are standardized, so their mean is 0 and standard deviation is 1.

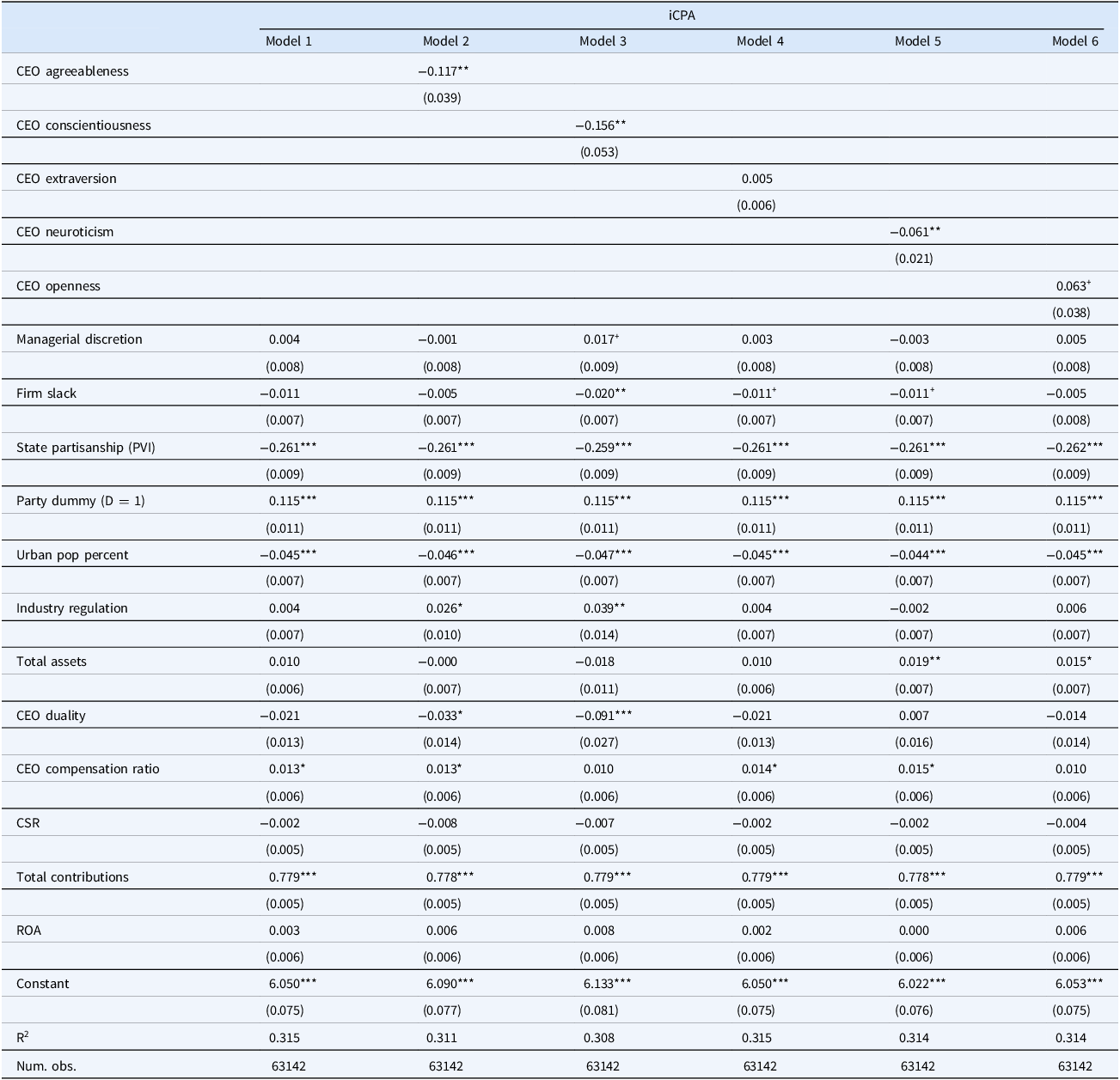

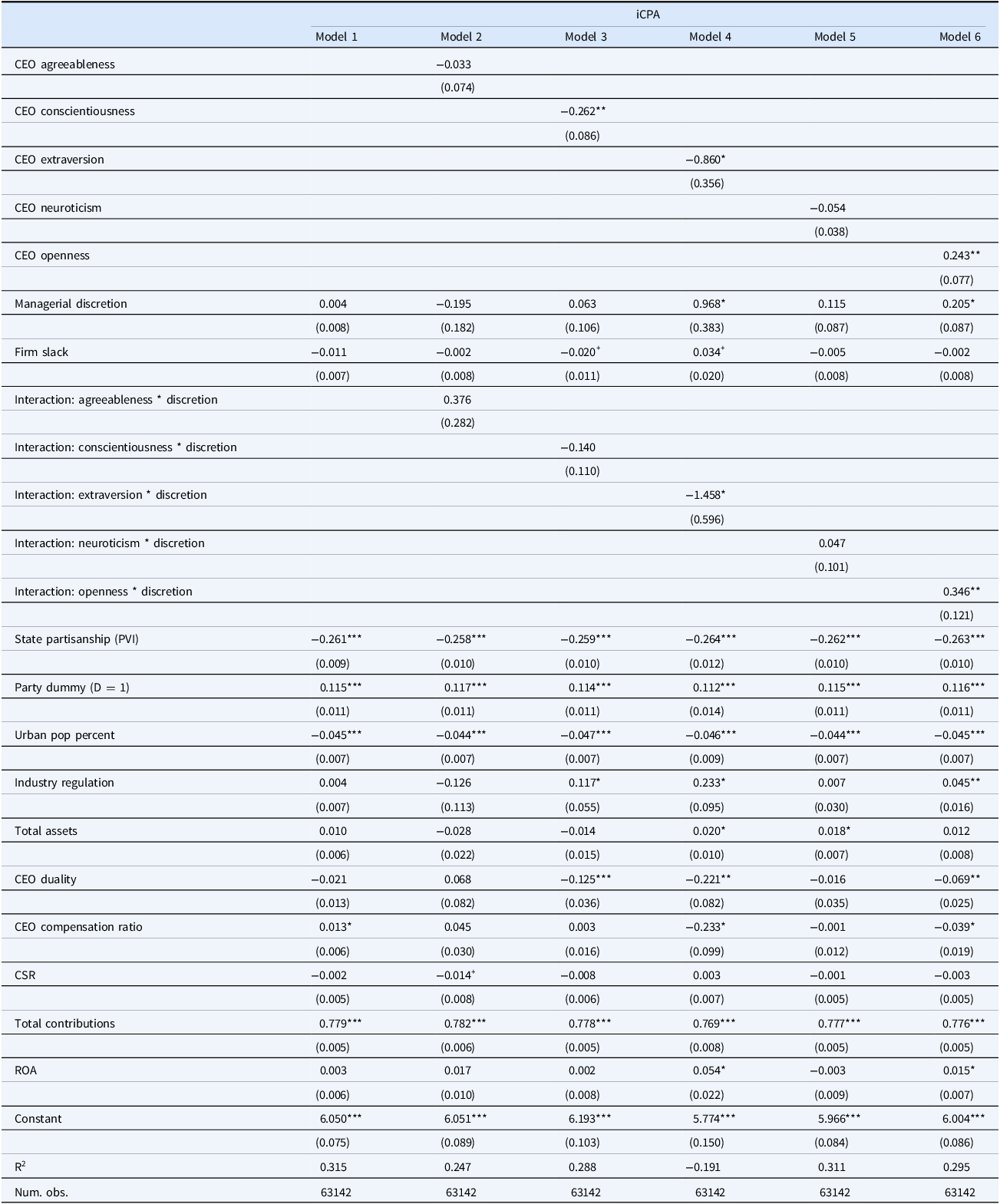

We report in Table 3 the beta coefficients for our direct effect regressions testing hypotheses 1 through 5. In model 1, we report the results of OLS regressions of our control variables on the dependent variable, iCPA. We find that many of the controls are statistically significant, demonstrating the value of their inclusion.

Table 3. Hypothesis tests

+ p < 0.10, *p < 0.05, **p < 0.01, ***p < 0.001, standard errors in parentheses.

Region dummies and two-digit SIC industry dummies included in all models.

Models 1 and 4 estimated with OLS, and all other models estimated with 2SLS to address endogeneity.

In hypotheses 1 through 5, we predicted that a relationship exists between the Big Five personality traits and ideological CPA. In most cases, we found support for our hypotheses. In hypothesis 1, we predicted a negative relationship between agreeableness and ideological CPA, and we did find the expected negative, significant relationship with iCPA (β=−0.117, p < 0.01, model 2). Thus, we find support for hypothesis 1. In hypothesis 2, we predicted a negative relationship between conscientiousness and ideological CPA. We also found support for this prediction, with a negative, statistically significant result (β=0.156, p < 0.01, table 3, model 3). In hypothesis 3, we predicted a positive relationship between the extraversion personality trait and ideological CPA. We did not find support for this prediction (β=0.005, p=0.472, model 4). Next, in hypothesis 4, we predicted a significant negative relationship between neuroticism and ideological CPA. Here, the results revealed the predicted relationship with our dependent variable (β=−0.061, p < 0.01, model 5). Finally, in hypothesis 5, we predicted a positive relationship between openness and ideological CPA, which we also found support for in our results (β=0.063, p < 0.1, model 6). Importantly, we note that the R2 we report for our models, ranging from 0.308 to 0.315 is high compared with other CPA research (McKay, Reference McKay2012), demonstrating the robustness of our results. Thus, in our initial tests, we found strong support for hypotheses 1, 2, and 4, and some support for hypothesis 5. We will analyze these results further in the discussion section.

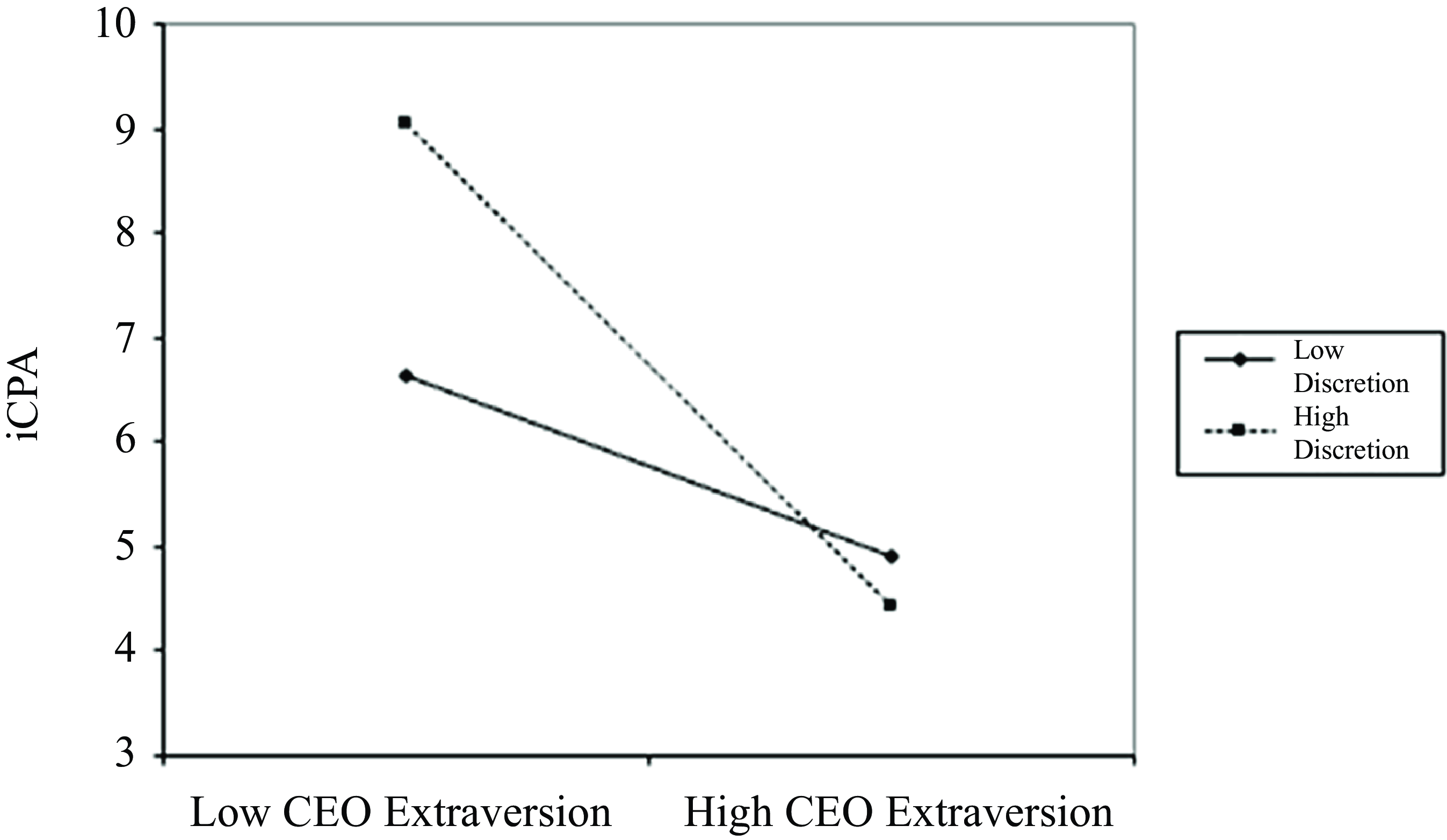

In hypothesis 6a and 6b, we predicted that managerial discretion would moderate the relationship between the CEO’s personality traits of extraversion and openness with the firm’s iCPA. In effect, since iCPA is something generally not in the interest of the firm, for a CEO to engage in more iCPA, they would require a certain level of discretion to do so. In table 4, we report our regressions testing these hypotheses. In particular, in models 10 and 12 of table 4, we found a significant interaction effect (extraversion: β=-1.458, p < 0.05, model 10; openness: β=0.346, p < 0.01, model 12), suggesting that we explore these relationships further (Aiken and West, Reference Aiken and West1991). In figure 2, we graph the effect managerial discretion has on the relationship between CEO extraversion and firm iCPA. Contrary to our prediction, we find that higher managerial discretion results in more iCPA where the CEO’s extraversion is low. As a result, we did not find support for hypothesis 6a.

Table 4. Moderation tests

+ p < 0.10, * p < 0.05, ** p < 0.01, *** p < 0.001, standard errors in parentheses.

Region dummies and two-digit SIC industry dummies included in all models.

Model 1 estimated with OLS, and all other models estimated with 2SLS to address endogeneity.

Figure 2. Interaction graph: Moderation effect of managerial discretion upon CEO extraversion.

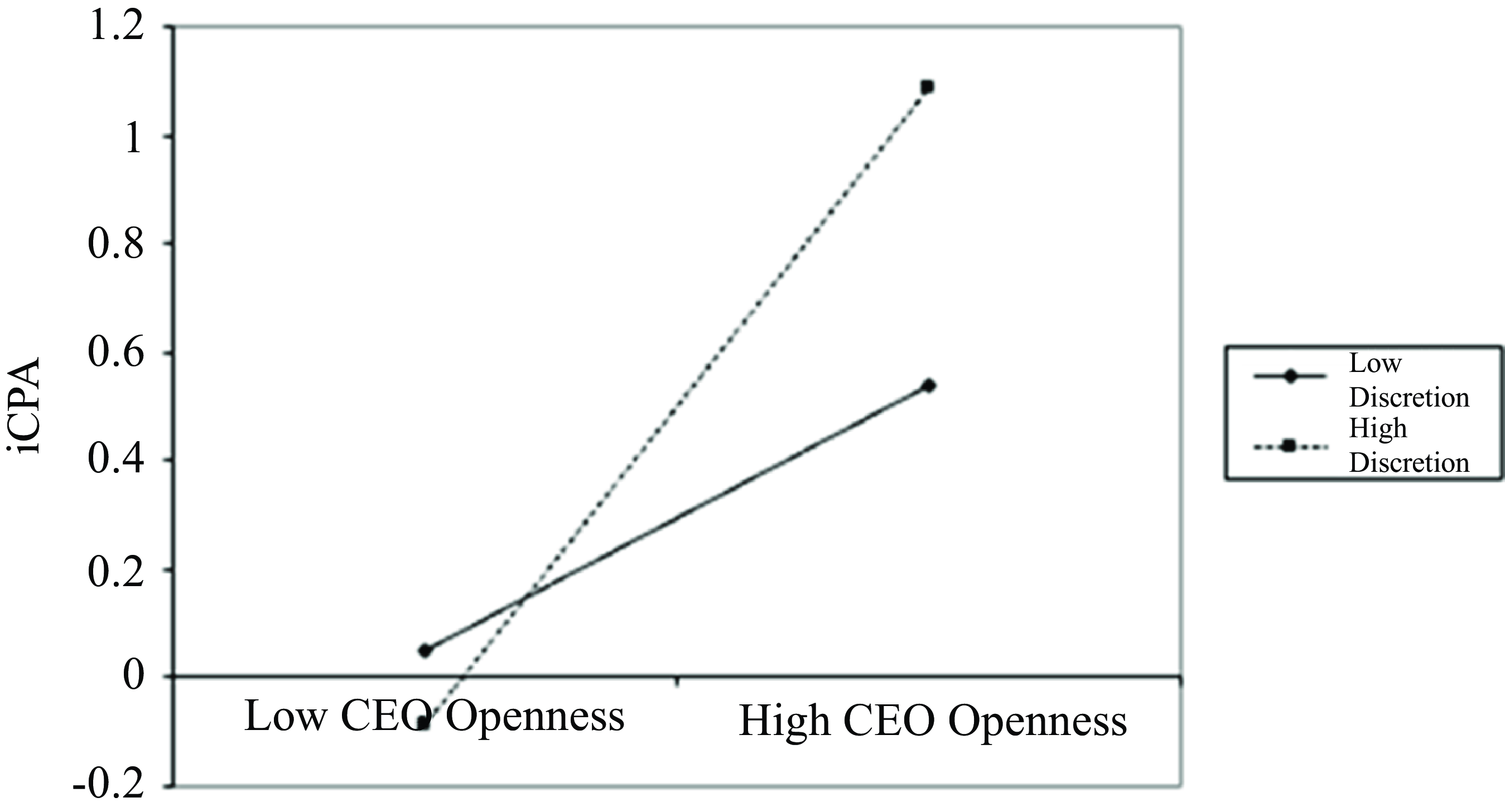

Next, to further explore the moderating effect of managerial discretion on the relationship between CEO openness and iCPA, we graph that relationship in figure 3. There, we can see that higher managerial discretion is related to significantly higher iCPA when CEO openness is high. As a result, we find strong support for hypothesis 6b.

Figure 3. Interaction graph: Moderation effect of managerial discretion upon CEO openness.

Robustness test

In testing our hypotheses, we constructed a dependent variable based on a measure of ideological CPA that quantifies the ideology of the social policies favored by the recipient of the CPA (Lewis et al., Reference Lewis, Poole, Rosenthal, Boche, Rudkin and Sonnet2018). There is, however, another dimension of the NOMINATE scores: economic issues. As a result, as a robustness test, we conducted regressions identical to our initial test, except with the NOMINATE dimension 1 economic scores as the basis for our ideological measure. In support of our findings, the results were consistent with the results we found for our main test.

Discussion

In this research, we address the question of whether CEO personality can be linked to CPA. We suggest that certain personality types will be more or less related to firm engagement in ideological CPA that provides a “consumption” benefit to the CEOs (Aggarwal et al., Reference Aggarwal, Meschke and Wang2012). In probing this question, we rely on UET, which suggests that due to their bounded rationality, CEOs make strategic choices based on their experiences and personalities (Chin et al., Reference Chin, Hambrick and Treviño2013, Hambrick and Mason, Reference Hambrick and Mason1984). In this way, CEOs’ personalities and values affect their firms’ operations and strategy.

In support of our hypotheses, we found significant, direct relationships as predicted between CEO agreeableness, conscientiousness, neuroticism, and openness with our ideological CPA dependent variable. Furthermore, we found significant interaction effects suggesting that managerial discretion moderates the relationship between CEO extraversion and openness on firm iCPA. When we graphed those interaction effects, however, we found support for the moderation effect we predicted on CEO openness, while we found the opposite of what we predicted for CEO extraversion. As a result, we found support for all our predicted relationships, except for those involving CEO extraversion.

This article contributes to the literature in several ways. First, it adds to the CPA literature by exploring a heretofore neglected antecedent to a firm’s CPA (Hillman et al., Reference Hillman, Keim and Schuler2004): CEO personality. While we had reason to think that CEO personality mattered, regarding the most common way personality is discussed we knew nothing. No longer. We support and expand the notion that CEO personality matters for CPA in that we now know how an additional number of distinct characteristics can orient CEOs toward or away from it. This is a much richer picture than could be had by considering narcissism, for example, alone. Research into the influence of CEO personality on firm outcomes has been growing since technology has allowed scholars to analyze texts for personality traits (Benischke et al., Reference Benischke, Martin and Glaser2019, Gow et al., Reference Gow, Kaplan, Larcker and Zakolyukina2016, Harrison et al., Reference Harrison, Thurgood, Boivie and Pfarrer2019, Yarkoni, Reference Yarkoni2010). In what appears to be a first-of-its-kind study, we find that CEO personality does affect CPA in predictable ways. This information can assist scholars in understanding why firms engage in CPA, a question that has been an issue in the research (Hadani and Schuler, Reference Hadani and Schuler2013, Aggarwal et al., Reference Aggarwal, Meschke and Wang2012).

Furthermore, this article contributes to the literature on UET. For instance, it points to another way that CEO personality can affect firm behavior. Prior research has found that certain characteristics of CEOs can affect organizational outcomes. For example, Petrenko et al. (Reference Petrenko, Aime, Ridge and Hill2016) found that CEO narcissism is related to firm CSR, Li and Tang (Reference Li and Tang2010) found that CEO hubris is associated with greater risk taking, but that this result is moderated by managerial discretion, and Chatterjee and Hambrick (Reference Chatterjee and Hambrick2007) found that higher CEO narcissism can influence firm performance and strategy. Other research has looked at the effect of personality traits on managerial behavior. For example, Peterson et al. (Reference Peterson, Smith, Martorana and Owens2003) found that CEO personality influences top management team dynamics. Thus, it seems clear that personality can be a basis for understanding CEO behavior and in turn how CEO characteristics will affect the organization. Here, we have a specific test that shows how such a fundamental CEO characteristic influences a discrete organizational activity, research that provides important support and embellishment to UET.

The results for our tests of the extraversion personality trait seems puzzling, given that they reveal what is essentially the opposite relationship of what we predicted. Perhaps this result might not be so puzzling, however. For example, extraverted CEOs, given their outgoing nature, might be more likely to befriend more moderate politicians since they are more likely to have a broad base of support within Congress as opposed to the ideological outliers. Thus, the social network of extraverted CEOs might be more likely to include the more moderate politicians. In this way, the characteristic of this personality trait might help explain these unexpected results.

Further research might explore the interaction of CEO personality with CPA in other contexts. For example, as detailed above, the results of empirical research looking for a link between CPA and firm performance have been ambiguous, at best (Hadani and Schuler, Reference Hadani and Schuler2013, Coates, Reference Coates2012). Perhaps scholars would find more consistent results when CEO personality moderates firm CPA. In other words, where CEO personality leads the CEO to behave responsibly with CPA funds, would we find higher performance? On the other hand, where a CEO personality lends itself to opportunistic behavior, the relationship between CPA and performance will likely be poor. Similarly, there may be other boundary factors in addition to managerial discretion that might affect the ability of the CEO to engage in ideological CPA. For example, where slack is unavailable, it might be impossible for a CEO to behave opportunistically even where managerial discretion is high. In other words, perhaps we might find more consistent results where we take into consideration the influence of managerial discretion and firm slack on CEO behavior, rather than just managerial discretion. Furthermore, research might explore whether these personality traits impact other forms of opportunism in the same way they impact opportunistic CPA. For instance, might these same personality traits be related in the same way to the acquisition of perquisites, shirking, or empire building? Indeed, one might explore overall the relationship between agency costs and CEO personality. Finally, future research might consider whether TMT personality traits moderate the impact of CEO personality traits on firm outcomes. For example, might a TMT high in conscientiousness be able to mute the inclination of CEOs high in openness to engage in opportunistic CPA? Or might a team high in openness result in an even more opportunistic CPA where the firm has a CEO high in openness? Clearly, there remain exciting opportunities for research on this topic.

Limitations of this research

Admittedly, this research is focused on American politics. Although this reality might be a limitation, given the important role the American economy plays on the global stage, it is likely worthwhile to study the distinct characteristics of US CPA. Furthermore, the five-factor model of personality has proven to be remarkably robust in its application in different cultures, nationalities and languages (Mondak and Halperin, Reference Mondak and Halperin2008). In this way, this theory might serve as a model for similar research in other countries.

Furthermore, this research only explored the impact of CEO personality on one aspect of CPA. This field, however, is robust (Schuler et al., Reference Schuler, Rehbein and Green2016), with many aspects of it demanding similar treatment. Future research might consider whether the choice of tactic, such as whether the firm engages in lobbying or independent campaign expenditures, is influenced by CEO personality. Indeed, the question as to whether the firm engages in CPA at all might be influenced by CEO’s personality and values. As a result, much research remains to be done on the relationship between CEO personality and firm CPA.

Additionally, there are many other factors that might serve as antecedents to firm CPA. For example, Greiner et al. (Reference Greiner, Kim and Cordon Thor2023b) looked at the impact of CEO narcissism on firm CPA. Similarly, Hadani and Schuler (Reference Hadani and Schuler2013) did find that the performance of firms in more highly regulated industries does tend to benefit from CPA, suggesting an industry impact on CPA. Other possible antecedents to explore might be firm strategy or exposure to policy, and conscientiousness and other CEO personality traits might be interesting to explore further as moderators. Therefore, much work remains to be done on the question of antecedents to firm CPA.

One limitation of this research impacts our methods and results. Specifically, as we detailed in the results section, the collinearity between the various personality traits is quite high, far above the level Kalnins (Reference Kalnins2018) would characterize as problematic. To address the bias introduced by multicollinearity, we tested each personality trait individually, as recommended by Kalnins (Reference Kalnins2018). While we would have liked to test all personality traits together, perhaps even interacting with them in some cases, we lacked the statistical tools to do so without bias. Indeed, this approach seems to make sense given the large amount of research that has looked at the impact of just one CEO trait, narcissism, on various discrete firm outcomes (see, e.g., Greiner et al., Reference Greiner, Kim and Cordon Thor2023b, Petrenko et al., Reference Petrenko, Aime, Ridge and Hill2016, Liu et al., Reference Liu, Zhu, Huang, Wang and Huang2021, Chatterjee and Hambrick, Reference Chatterjee and Hambrick2007). That said, it would be interesting to see results combining all personality traits, so it is our hope that methods can be devised to accomplish this goal without bias.

Finally, we were limited in our research by both the availability of data and the difficulty in measuring personality even with our linguistic approach. As a result, there will certainly be an opportunity to expand on this research as other scholars increase the number of CEOs for whom personality is measured and the kind of organizations in which such measures are taken.

Managerial implications

For managers and investors, this research provides a valuable contribution: specifically, it helps them identify managers who might behave in a more opportunistic manner. While this research is focused on CPA, its findings can likely extend into other areas where managers might behave opportunistically, such as CSR (Wright and Ferris, Reference Wright and Ferris1997, Petrenko et al., Reference Petrenko, Aime, Ridge and Hill2016), the acquisition of perquisites, shirking, or empire building (Ang et al., Reference Ang, Cole and Lin2000). Given the controversy over the use of personality tests as a tool for hiring and promotion (Tett and Christiansen, Reference Tett and Christiansen2007), this research might provide additional justification for employers and boards to use such tests as they construct their top management teams. Indeed, if, as we expect, these conclusions can be generalized to address other potential sources of agency costs, this research might prove to be a powerful tool for boards to safeguard shareholder resources from abuse.

Conclusion

In this article, we sought to explore a long-standing question puzzling management scholars, particularly the antecedents to CPA (Hillman et al., Reference Hillman, Keim and Schuler2004, Lawton et al., Reference Lawton, McGuire and Rajwani2013). We argue that the personality traits of CEOs will impact the kind of CPA the firm engages in. In particular, we argue that certain CEO traits are more or less associated with ideological CPA, which tends to be reflective of opportunism on the part of the CEO. Furthermore, we find that managerial discretion moderates the relationship between CEO personality and the level of ideological CPA the firm engages in. Given the controversy associated with CPA, especially when it is motivated by the CEO’s personal priorities, this research can not only contribute to the scholarly debate over CPA antecedents but also can provide guidance to boards seeking to limit agency costs while also contributing to the public policy discussion over how to repair the American electoral system that is widely believed to be deeply broken.

Funding

This study received no funding.

Competing interests

The authors declare that they have no conflict of interest.

Open access

Open access