INTRODUCTION

Studies on social networks have mainly focused on the subjects of guanxi in China, yongo in South Korea, wasta in the Middle East, and blat in Russia. These concepts of connections characterize relationships among people of similar ethnic groups (guanxi) or backgrounds related to, for example, a shared hometown (yongo) or kinship ties (wasta). For instance, the wasta concept refers to people with similar traits such as shared kinship ties, shared tribal loyalty, and a shared language. Many studies have examined the various concepts of ‘connections’ in the Asian and Middle Eastern regions, but less attention has been paid to Malaysia. Informal social networks in Malaysia are somewhat different, with connections that cross various ethnic groups, as Malaysia is a multiracial country with three dominant ethnic groups: Bumiputera, Chinese, and Indian.

These ethnic groups formed the National Front (Barisan Nasional in Malay), the main ruling coalition party that governed Malaysia from the time of its independence in 1957 but experienced a defeat in the 2018 federal elections.[Footnote 1] The cooperation between various ethnic groups in Malaysia provides a link between social networks and the development of the capital market. White (Reference White2004) documents that between 1955 and 1970, the creation of the informal social network among the various ethnic groups in Malaysia was mainly due to the economic development of the country, as Bumiputera groups controlled the government while Chinese groups owned many national resources. However, the network changed after 1970 as a result of the introduction of the New Economic Policy (NEP), which supported affirmative action to increase Bumiputeras' economic participation in the capital market. Some studies (Case, Reference Case2017; Chan, Reference Chan2012; White, Reference White2004) state that appointments have become ethnicity-driven over time, with Bumiputera government officials joining the boards of Chinese-dominated firms to gain experience. However, the introduction of the NEP in 1970 resulted in two main issues in relation to board appointments in Malaysia. First, the affirmative action initiatives limited the interactions between ethnic groups, as the appointments were not due to expansion and acquisition of resources among Bumiputera directors but rather to fulfill the NEP's objectives (Chan, 2012; Gomez, Reference Gomez2004). Gomez (Reference Gomez2004) highlights that due to the introduction of the NEP, Chinese-controlled firms decided to remain independent, i.e., to retain a family-type firm structure. Such a policy is often seen as an inhibitor of networking in Malaysia, as it promotes cronyism and nepotism (Chan, Reference Chan2012; Gomez & Jomo, Reference Gomez and Jomo1999). The second issue is that board appointments were often seen as a tool to promote NEP initiatives, resulting in increasing nepotism and cronyism. The board appointments are not confined to only one ethnic group (i.e., Bumiputeras) but include other ethnic groups as well. Case (Reference Case2017) highlights how Tun Mahathir and Tun Daim, while in power, granted major infrastructural contracts to Vincent Tan, Ting Pek Kkiing, and Ling Hee Leong.[Footnote 2] Case (Reference Case2017) further argues that this revolving-door system used by the government is designed to forge intricate sets of government-business relationships, thus enabling authoritarian politics to persist over time.

Corporate scandals have recently plagued Malaysia. The ongoing case of 1Malaysia Development Berhad (1MDB) involving the former prime minister of Malaysia, Dato’ Seri Najib Razak, offers an example of alleged misuse of power at the highest level. 1MDB adopted a three-tier corporate structure, with a management tier, board of directors, and advisory board. Najib, as the finance minister and the chairman of 1MDB, was the sole signatory of its investments (Case, Reference Case2017); this suggests a failure of the proper separation of power and control. The 1MDB scandal has attracted the attention of the U.S. Department of Justice (DOJ) in relation to possible illegal money laundering.

Studies on political connections in Malaysia suggest that politically connected firms are inefficient and risky. Johnson and Mitton (Reference Johnson and Mitton2003) investigate the impact of the implementation of capital controls on politically connected firms in Malaysia during the Asian financial crisis in 1998–99 and find that the measure improved the performance of connected firms by increasing their efficiency. Gul (Reference Gul2006) finds that auditors charge higher auditor fees to politically connected firms because they view them as risky. These papers provide some consensus in which connected firms are viewed as inefficient and risky and as a route for expropriating minority shareholders. Anecdotal and empirical evidence provides some indication that political connections cause a certain amount of uncertainty in Malaysia's capital market.

We propose two research objectives. First, we examine the relationship between director networks and earnings quality in Malaysia. Second, given the political landscape coupled with smoking-gun anecdotal evidence of cronyism and nepotism in Malaysia, we examine the relationship between the network of politically connected directors and earnings quality. Generally, the director network is defined as a set of directors along with a set of specific types of connections, such as friendships and formal appointments, among them. The network in our context is constituted by persons or directors who are affiliated with one firm while sitting on the board of directors of another firm. We defined politically connected directors as directors who sit on the boards of the firms primarily affiliated with Tun Mahathir, Dato’ Seri Anwar Ibrahim, and Tun Daim Zainuddin. These are political figures from the dominant party, the UMNO that forms the backbone of the National Front (Barisan Nasional), which governed Malaysia during our sample period. Similar to Johnson and Mitton (Reference Johnson and Mitton2003), we consider the firms that are affiliated with the major parties, the UMNO, and the MCA.

We elaborate our study based on resource dependence theory, which states that an organization must obtain resources from its environment to survive (Pfeffer & Salancik, Reference Pfeffer and Salancik1978). Pfeffer and Salancik (Reference Pfeffer and Salancik1978) describe four strategic factors for managing inter-organizational resources: (1) interlocking directors, (2) joint ventures, (3) organization size, and (4) top administrator contacts with other organizations. Board interlocks could serve as a mechanism for firms to reduce environmental uncertainty and dependence and provide access to diverse and unique information and the ability to learn new corporate practices. Directors who are in a network could obtain better information and gain more experience from other firms, which should be positively reflected in monitoring and hence increase earnings quality. On the other hand, board interlocks could increase directors' professional commitments, and this could result in inadequate monitoring, especially concerning giving appropriate advice. This lack of monitoring by directors could result in lower firm performance and, thus, lower earnings quality (Larcker, So, & Wang, Reference Larcker, So and Wang2013).

Pfeffer and Salancik (Reference Pfeffer and Salancik1978) suggest political mechanisms as another means to reduce uncertainty and interdependence on the broader social system, which includes the government.

Studies by Hillman (Reference Hillman2005) and Pascual-Fuster and Crespí-Cladera (Reference Pascual-Fuster and Crespí-Cladera2018) suggest that politicians, or former politicians, on boards of directors provide several advantages. First, politicians are able to provide resources to firms and probably act as (unofficial) collateral against capital owed. In addition, they could provide expertise on the capital market rules and regulations imposed by government regulators and thereby help increase firm stability. Politicians could play a governance role, as they could act to ensure that firms remain within the expectations of regulators. The involvement of politicians on boards could also suggest that they want to counter negative perceptions of cronyism among the public by exercising due care and monitoring of the firm. These advantages could mean an increase in firm performance and could, in turn, result in higher earnings quality.

However, having politicians on the board could have an adverse effect since the nature of politics creates uncertainty. Mizruchi (Reference Mizruchi1996) and Westphal and Khanna (Reference Westphal and Khanna2003) suggest that directors may be less likely to monitor management to maintain their social status and network cohesion while avoiding social sanctions from the directorate network.

We consider five network centrality measures. The first two measures on the degree are the total number of direct relationships formed with other directors internal and external to the entity, respectively. Higher degree centrality suggests that a board has more opportunities and resources compared to other firms in the network (Larcker et al., Reference Larcker, So and Wang2013), as they are more active in terms of intercorporate board networks (Wasserman & Faust, Reference Wasserman and Faust1995). The third measure, which is a further refinement of the degree measures, recognizes that having more direct connections is more influential when the connections are to other well-connected boards (Larcker et al., Reference Larcker, So and Wang2013). The first three measures of network centrality are a reflection of the direct impact or size of information in the network. However, the size of the network does not measure the quality of the information within the network. Hence, our next two network centrality measures provide information on the brokerage position and the distance or closeness between two firms in the network. The brokerage position suggests that a board is well connected if it lies on a relatively more direct path between boards, making them a principal broker of information or resource exchange (Larcker et al., Reference Larcker, So and Wang2013). The fifth network centrality measure captures the relative closeness of a board with an outside board. One would expect the relative closeness between two boards to result in faster information exchange and thus make information more readily available. Directors who receive information and can act upon it faster are beneficial for firm innovation and efficient governance practices (Borgatti, Reference Borgatti2005). Our choice of earnings quality measure is the residual from an accrual model. Accrual is the difference between earnings and cash flow. An extreme amount of accruals suggests low earnings quality because they represent less persistent or sustainable components of earnings (Dechow, Ge, & Schrand, Reference Dechow, Ge and Schrand2010). These residuals represent management discretion or estimation errors, both of which reduce decision usefulness (Dechow et al., Reference Dechow, Ge and Schrand2010).

To calculate the network measures, we hand-collected the names of the directors of 745 firms listed on Bursa Malaysia in 2011, resulting in 4,416 individual directors. Based on the cumulative director network measures that form the firms’ network measures, we find a negative relationship between these measures and earnings quality and our results suggest a decrease of 14 percent. Our results suggest that the increase in the number of professional commitments among directors prevents them from effectively monitoring firms.

Our univariate analysis of politically connected directors finds that connected directors are more central in the network, which means they have more contacts and thus have greater resources. In addition, connected directors have a better brokerage position relative to nonconnected directors, as they are closer between two directors. Their better brokerage position and closeness to other directors in the network suggest that the information could travel faster to these directors, and their firms could act upon it, with the director's political connection, thus serving to promote efficiency and good governance. However, our multivariate analysis finds a negative relationship between increases in the connectedness measures of politically connected directors and earnings quality. The findings support the idea that political connections generate uncertainty in the organization itself. In addition, the appointment of politically connected directors is rather ceremonial and enhances their social stature rather than the monitoring of the organization. In addition, our findings may suggest that the information such directors provide could be redundant or even false (Larcker et al., Reference Larcker, So and Wang2013). For most of the network centrality measures mentioned above, the results are consistent when we use alternative measures of earnings quality.

We contribute to the extant literature in several ways. First, we add to the growing literature on informal networks by examining the role of director networks and their impact on earnings quality. Second, the choice of Malaysia provides a distinct contribution since Malaysia is an emerging economy with a unique institutional background, as the development of its capital market coincides with the interaction of several ethnic groups. Third, we contribute to the political connections literature by examining a network created by politically connected directors. This investigation and results provide further opportunity for a similar type of research in the region, where the formal institutions of some countries are underdeveloped.

The outline of the study is as follows. The next section discusses the institutional background of Malaysia, while the next section elaborates on the theoretical background and the rationale behind the hypotheses developed for this study. The methods section discusses the choice of variables and the main model we use for this study. The section that follows tabulates our results and presents the various robustness analyses performed. We present the discussion and research implications in the next section, and the final section concludes.

INSTITUTIONAL BACKGROUND

Malaysia is a multiethnic society and is often seen as a product of British colonialism (Berger, Reference Berger2010). Malaysia was originally inhabited by Bumiputera (literally ‘sons of the soil’), who include the Malays and orang Asli (indigenous people such as the Iban and Kadazan in East Malaysia). Immigrants, primarily Chinese and Indian, started to arrive during the period of British colonization. Chinese immigrants were involved mainly in mining, commerce, and trade, while Indian immigrants were most active on plantations. The Bumiputera or Malay population worked mainly in civil services. Malaysia achieved independence in 1957 through collaborative efforts across ethnic groups (Johansson, Reference Johansson2015). These efforts not only formed the government but also shaped the initial government-business link in Malaysia. The initial partnership between ethnic groups aimed primarily to coordinate power and resources among the two dominant ethnic groups. The UMNO, a Malay political party, held most of the ministerial posts, but it lacked resources and thus tapped into the resources of Chinese groups (White, Reference White2004). White (Reference White2004) argues that the relationship between the Malay aristocracy and Chinese and later Indian business leaders proved to be foundational for a free enterprise economic policy, a sound economy, and balanced budgets. Gomez (Reference Gomez2004) supports this view and further states that interlocking directorates among ethnic groups were common during the colonial period.

Malaysian society faced a defining event with the racial riots of 1969, which were primarily blamed on economic imbalances among ethnic groups, especially between the Bumiputera and Chinese populations. Hence, in 1970, the Malaysian government introduced the New Economic Policy (NEP) with two distinct objectives: to eradicate poverty and to restructure society to reach interethnic economic parity (Gomez & Jomo, Reference Gomez and Jomo1999), or in other words, to eliminate ethnic identification in relation to economic contribution. In reality, the NEP developed into an affirmative action initiative to enhance Bumiputera economic participation. The post-NEP period is often seen as a time when the informal network was mostly supportive of the NEP agenda in promoting ownership in the capital market among the Bumiputera population (Chan, Reference Chan2012). Malaysian board appointments have since been proven to be driven by policies of enhancing ownership among the Bumiputera ethnic group. This policy was seen as successful in an early stage, but it was prolonged as a form of cronyism. Appointments to boards of directors in the post-NEP period have mostly come to be seen as ceremonial, limiting the possible benefits that an organization could reap from them.

To conclude, board appointments in Malaysia have shifted from emphasizing a joint partnership among ethnic groups to fulfilling the NEP objectives of enhancing ownership and participation in the capital market of the Bumiputera people. Gomez (Reference Gomez2004) argues that affirmative action does not increase the level of directorate interlocking among ethnic groups. Gomez (Reference Gomez2004) further argues that the Chinese business community has transcended the family-controlled business model, which indicates that these firms are able to function independently.

THEORETICAL BACKGROUND AND HYPOTHESES

Director Networks and Earnings Quality

We elaborate our argument based on the tenets of resource dependence theory (Pfeffer & Salancik, Reference Pfeffer and Salancik1978), which states the network created by interlocking board directorates should provide more information and resources to the firm and thus should increase firm performance. Interlocking directorates or networks of directors are often viewed as a means of bridging organizations such that friendships can develop, communication can easily flow, and plans can be made (Shrader, Hoffman, & Stearns, Reference Shrader, Hoffman and Stearns1991). The connections are established through shared endpoints and create paths that indirectly connect other directors (Borgatti & Halgin, Reference Borgatti and Halgin2011; Brass, Reference Brass and Kozlowski2011). The connections are socially rather than legally binding (Kilduff & Brass, Reference Kilduff and Brass2010). Omer, Shelley, and Tice (Reference Omer, Shelley and Tice2014) state that by sitting on multiple boards, directors have access to information and resources on, for instance, effective corporate practices. They argue that multiple directorships promote information transfer among directors across networks.

This notion is supported by several studies (see Larcker et al., Reference Larcker, So and Wang2013; Omer et al., Reference Omer, Shelley and Tice2014; Renneboog & Zhao, Reference Renneboog and Zhao2011), that better networks provide better, faster, more uniform information. Renneboog and Zhao (Reference Renneboog and Zhao2011) suggest that the purpose of a network is to create economies of scale, to provide better connections and thus better resources, to assist in decision-making and protection and to promote positive and effective governance. Better-networked directors could have access to more information and a better understanding of the capital market based on the information they obtain from other firms, as the network depicts the amount and timeliness of information diffused among the individuals involved (Omer et al., Reference Omer, Shelley and Tice2014). Omer et al. (Reference Omer, Shelley and Tice2014) argue that the better the network, the more informed the decisions the directors or individuals can make; an effective network, therefore, assists in decision making and monitoring.

Brown, Gao, Lee, and Stathopoulos (Reference Brown, Gao, Lee, Stathopoulos, Boubaker, Nguywen and Nguywen2012) view the benefits derived from director networks as determined by the ‘strength’ of the network, arguing that weak ties are better and provide more incremental benefits to a firm than a strong network, as the information is more likely to come from a more trustworthy source, and thus weak ties provide a different perspective relative to stronger ties.

On the other hand, increases in networking mean directors become busier, and this may give them less capacity for monitoring, leading to a decrease in earnings quality. Core, Holthausen, and Larcker (Reference Core, Holthausen and Larcker1999), Fich and Shivdasani (Reference Fich and Shivdasani2006), and Larcker et al. (Reference Larcker, So and Wang2013) argue that multiple boards or board interlocks reduce monitoring effectiveness; this phenomenon is commonly termed ‘busy boards’ or the ‘busyness hypothesis’. Andres, Bongard, and Lehmann (Reference Andres, Bongard and Lehmann2013) state that the busyness hypothesis associates firms that have busy directors with weak governance, as directors who serve on a large number of boards may become overcommitted and unable to comply adequately with the requirements of their position as monitors of management. These commitments are not only those directly related to the firms but also social obligations such as attending functions, becoming involved in charitable organizations (Hwang & Kim, Reference Hwang and Kim2009) and sustaining political or media connections (Andres et al., Reference Andres, Bongard and Lehmann2013). Moreover, while Hall, Samuel, and Sedgwick (Reference Hall, Samuel, Sedgwick and Taylor1957) state that board interlocks via shareholdings and directorates create an elite group of ‘insiders’ that wield close and continuous control of the organization, they suggest that these interlocking directorates impede the possible benefits from diverse ownership occasioned by the separation of ownership and control.

Theoretically, the diversity of business networks in Malaysia should yield similar benefits. However, the NEP, introduced in 1970, has had some adverse effects in relation to board appointments and, ultimately, to firms’ acquisition of external resources. As highlighted by White (Reference White2004), the appointment of Bumiputera or Malay civil servants to the boards of firms dominated by Chinese owners is often seen as ceremonial, as the civil servants do not possess expertise in the area. However, White (Reference White2004) argues that this arrangement is somewhat necessary to ease transactions with the government, which is dominated by Malay civil servants. The NEP, aimed at eliminating ethnic-economic identification, has only resulted in affirmative action to increase Bumiputera economic participation. Gomez (Reference Gomez2004) holds that the NEP limits interaction between ethnic groups and mitigates further interlocking directorates. Gomez (Reference Gomez2004) also argues that firms dominated by Chinese owners have become more independent and self-reliant in the post-NEP period. Based on this scenario shaped by policy changes that limit possible interactions among directors, we propose the following hypothesis:

Hypothesis 1: There is a negative relationship between the connectedness of director networks and earnings quality in the Malaysian context.

Politically Connected Networks and Earnings Quality

Building on resource dependence theory in the context of director networks, we apply a similar premise for the network of directors with political connections. Pfeffer and Salancik (Reference Pfeffer and Salancik1978) state that firms might resort to political mechanisms to reduce uncertainty and dependency on the broader social system, which includes the government. Firms may opt for political means to influence economic conditions in their favor. Hillman (Reference Hillman2005) argues, based on resource dependence theory, that firms’ dependency on external resources creates uncertainty. This uncertainty could originate from government policies, regulations, and enforcement. The firm creates informal linkages with politicians to mitigate this uncertainty (Selznick, Reference Selznick1949). Based on the above arguments, one would expect that there is a positive relationship between the degree of political connection of a network and earnings quality. Dahan (Reference Dahan2005a) suggests that the organizational resources secured by having political connections include relational resources such as formal and informal relationships with politicians, reputation, and financial resources.

Conventional wisdom suggests that political connections should increase a firm's value, as a tremendous amount of political rents are generated due to the resources politicians need to devote to rent-seeking activities (Fisman, Reference Fisman2001). There are many ways for political connections to lead to the accumulation of benefits for a firm. Such connections can deliver preferential access to finance (Dinc, Reference Dinc2005), political bailouts in the event of financial distress (Faccio, Masulis, & McConnell, Reference Faccio, Masulis and McConnell2006), lower tax burdens (Adhikari, Derashid, & Zhang, Reference Adhikari, Derashid and Zhang2006) and a greater allocation of government investment during periods of financial crisis (Johnson & Mitton, Reference Johnson and Mitton2003). Chaney, Faccio, and Parsley (Reference Chaney, Faccio and Parsley2011) also suggest that political connections should increase earnings quality due to heightening media scrutiny of connected firms, which could enhance monitoring. One would expect that, with this increased scrutiny, better access to resources, and enhanced monitoring due to public or state interest, connected firms should have higher earnings quality relative to nonconnected firms.

Higher average degree centrality measures of politically connected directors suggest that they have more contacts in the network. Since politicians have direct access to information on, for instance, government contracts and possible future collaboration with foreign countries, this provides an avenue for firms to increase their resources and could, in turn, increase earnings. In addition, politically connected directors that have, on average, higher eigenvalues are more visible in the network and could signal media pressure (Chaney et al., Reference Chaney, Faccio and Parsley2011), which should have a positive impact on the firm, as politicians want to avoid being scrutinized. Next, politically connected directors that have, on average, higher closeness and betweenness measures are more central in the network, which suggests that they have faster access to information in the network. Politically connected directors have access to private information such as future regulations and changes in tax provisions, which should assist management in shaping the direction of the firm. Lupton and Wilson (Reference Lupton and Wilson1959) provide an initial assessment of the nature of the network of top decision-makers in the UK based on six categories.[Footnote 3] They find that the top decision-makers in these categories have some commonalities in terms of educational background, and they do display some degree of family kinship.

Chaney et al. (Reference Chaney, Faccio and Parsley2011) describe three mechanisms that could contribute to a negative relationship between political connections and earnings quality. First, insiders in connected firms could hide, obscure, or delay reporting the benefits received with the intention of misleading investors. Second, Chaney et al. (Reference Chaney, Faccio and Parsley2011) argue that connected firms simply care less about the quality of accounting information, as politicians are shielding them, and the third argument is that firms with poor earnings quality are more likely to establish political connections. Pascual-Fuster and Crespí-Cladera (Reference Pascual-Fuster and Crespí-Cladera2018) argue that having politicians as directors could result in deviation from value-maximizing objectives. In addition, politicians could be a source of risk and uncertainty, which are features of being in politics.

In China, government ties or political connections are part of the guanxi concept of social networks. Managerial ties to government function as a substitute for formal institutional support (Xin & Pearce, Reference Xin and Pearce1996), as ties with government officials can compensate for a lack of market-supporting institutions such as transparent laws and regulations. In addition, government ties or political connections are established to access scarce resources, to obtain information about policies and to reduce uncertainty. Guanxi works well in China since the country is experiencing an economic transition, which produces a high degree of uncertainty and institutional voids. Interpersonal ties play a critical role in facilitating economic transitions, resource acquisition, and business operations (Peng & Heath, Reference Peng and Heath1996).

Studies find that benefits accrue to firms based on political connections. A paper on Malaysia by Johnson and Mitton (Reference Johnson and Mitton2003) finds that connected firms perform better than nonconnected firms during periods of imposition of capital controls. These findings of Johnson and Mitton (Reference Johnson and Mitton2003) suggest that politically connected firms in Malaysia do use political tactics for their own benefit. Bliss and Gul (Reference Bliss and Gul2012b) find a positive relationship between political connections and leverage, which also signals that connected firms have more collateral to obtain funding. A meta-analysis by Luo, Huang, and Wang (Reference Luo, Huang and Wang2012) finds that the studies in their sample support this argument. They find a positive relationship between guanxi and firm performance at both the economic and organizational levels.

The evolution of the political network in Malaysia's capital market began with the direct intervention by the state in major businesses after the introduction of the NEP in 1970. The NEP aimed first to eradicate poverty irrespective of race through income expansion and occupational opportunities and second to restructure Malaysian society to reduce and eventually eliminate the identification of race with economic function. During the initial stage of the NEP, the state directly intervened in business activities through public corporations that act as trustees on behalf of economically disadvantaged Bumiputeras. Further, this period witnessed active political involvement by the dominant parties in Malaysia and thus created a social network among politicians, state managers, and directors.

The political economy of Malaysia also provides an institutional setting characterized by the existence of a relationship-based economy. The term ‘relationship-based economy’ reflects the significance of relationships between the corporate and political spheres in Malaysia (Gomez, Reference Gomez and Gomez2002). The political economy in Malaysia also shows considerable evidence of the creation of indirect relationships among key players in firms due to NEP implementation. These indirect relationships evolved throughout the NEP period and eventually sparked arguments over whether favoritism towards Chinese capitalists by Malay groups in politics and government stabilized economic conditions at that time. Chan (Reference Chan2012) argues that informal ties with politicians facilitate access to key state leaders who can provide firms with lucrative state rents in the form of licenses, contracts, and business deals with state corporations. In addition, it is generally argued that these ties facilitate cronyism and rent-seeking activities (Gomez, Reference Gomez and Gomez2002). The current economic situation is characterized by the presence of elite groups sustained by the relationship-based economy, which has led to favoritism of firms or directors in the Malaysian capital market (Adhikari et al., Reference Adhikari, Derashid and Zhang2006). Given Malaysia's institutional and political background, board appointments of politicians could serve ceremonial and strategic purposes. As highlighted by Case (Reference Case2017), the appointments of UMNO party officials to positions in ministerial posts and government-linked corporations has led to the extraction of state assets, licenses, and funds. Case (Reference Case2017) further highlights that due to this positioning of party members, the barriers between government and firms are low, which results in expropriation of assets. Such relationships or ties are often seen as not contributing much to business growth as they are only symbolic or occupational in nature and serve to fulfill the NEP's objectives (Gomez, Reference Gomez and Gomez2002).

The nature of board directors’ political connections in the region might be similar, as the connections are much needed as a substitute for formal institutions. However, the connections have to led to nepotism and cronyism and are driven by political needs and the authoritarianism of the ruling party. The evidence seems to support this interpretation for the case of the informal social network in Malaysia but not that of guanxi in China. Based on the above arguments and the evidence in the extant literature, we propose the following alternative hypotheses:

Hypothesis 2: There is a negative relationship between the degree of political connectedness of director networks and earnings quality in the Malaysian context.

Hypothesis 2a (H2a): There is a positive relationship between a lack of political connectedness in director networks and earnings quality in the Malaysian context.

METHODS

Dependent Variable

We opt for Francis, LaFond, Olsson, and Schipper's (Reference Francis, LaFond, Olsson and Schipper2005) model of accruals quality, which is a modification of Dechow and Dichev's (Reference Dechow and Dichev2002) model, as our proxy for earnings quality. The Dechow and Dichev model uses firm-level time series regressions with total accruals as the dependent variable and the cash flow of previous, current, and subsequent years as independent variables. The standard deviation of the residuals for each firm is then used as the accruals quality measure. Dechow and Dichev (Reference Dechow and Dichev2002) note that the absolute value of the residual is an alternative measure of accruals quality when such a measure is needed for each firm-year.

Based on comments made by McNichols (Reference McNichols2002), Francis et al. (Reference Francis, LaFond, Olsson and Schipper2005) included two more independent variables, changes in sales revenue, and property, plant and equipment (PPE) assets, on the basis that this helps to improve the expectations of current accruals. We use the same model, and since we want the measure on a firm-year basis, we use the absolute value of the residual as the measure of accruals quality. The model is as follows:

The variables are as follows:

All variables are scaled by average total assets. After computing the residual from (1), we use the negative absolute value to suggest that greater discretionary accruals represent weaker accruals quality as the dependent variable in the following model:

Independent Variables

Our choice of independent variables reflects the network (NETWORK) measures widely used in the literature on director networks. We opt for five centrality measures: (1) degree-included (NDEGREE-IN), (2) degree-excluded (NDEGREE-EX), (3) eigenvalue (NEIGEN), (4) betweenness (NBETWEENNESS), and (5) closeness (NCLOSENESS). The normalized value for each centrality measurement is a relative measure used when comparing different types of networks (Scott, Reference Scott2000).

We measure the networks by these five well-known dimensions rather than by a simple count of director interlocks, which is hardly an adequate measure of network centrality (Andres et al., Reference Andres, Bongard and Lehmann2013). The first dimension is degree-included (DEGREE-IN), which is the most straightforward measure of an individual's importance in a network (Freeman, Reference Freeman1979). It is defined as the number of direct ties that a director has to other directors in the network via common board membership (Omer et al., Reference Omer, Shelley and Tice2014). The second is degree-excluded (DEGREE-EX), which is calculated by a director's number of direct ties outside the firm.

Based on literature focusing on the measurement of direct networks, these degree calculations can be used to assess managerial or power influences (Bonacich, Reference Bonacich1987; Brass, Reference Brass and Kozlowski2011; Horton & Serafeim, Reference Horton and Serafeim2012; Renneboog & Zhao, Reference Renneboog and Zhao2011). Both calculations (DEGREE-IN and DEGREE-EX) represent network size and connectivity (Durbach & Parker, Reference Durbach and Parker2009; Fracassi, Reference Fracassi2017).

The third measure is the eigenvalue (EIGEN), which measures the number of connections to well-connected directors. The larger the number of these three measures, the more direct ties and the higher the level of managerial influence (Larcker et al., Reference Larcker, So and Wang2013; Renneboog & Zhao, Reference Renneboog and Zhao2011). EIGEN centrality is widely used, which also implies the assumption that the status of managerial power or the centrality of individuals is based on the position of neighboring directors of firms (Bonacich & Lloyd, Reference Bonacich and Lloyd2015).

Our fourth network measure is betweenness (BETWEENNESS), which represents the key point of information brokerage within the network. Freeman (Reference Freeman1979) and Scott (Reference Scott2000) suggest that betweenness is useful and potentially measures the point of control of information. BETWEENNESS has been widely used in social network analysis as an effective indicator of the information a director can secure and access purely from his or her networks (Barnea & Guedj, Reference Barnea and Guedj2006; Freeman, Reference Freeman2004). Therefore, a director with a relatively high betweenness measure has the opportunity to control and manipulate information within the network.

The fifth measure is closeness (CLOSENESS), which captures director centrality and reflects how close a particular individual is to all others in the network (Horton, Millo, & Serafeim, Reference Horton, Millo and Serafeim2012). CLOSENESS, therefore, refers to how efficiently and effectively an individual can communicate with others by communicating either directly or through intermediaries (Horton et al., Reference Horton, Millo and Serafeim2012). It also represents the importance of the network connections that each director has (Barnea & Guedj, Reference Barnea and Guedj2006; Fracassi, Reference Fracassi2017), as director closeness should optimize communication efficiency (Nicholson, Alexander, & Kiei, Reference Nicholson, Alexander and Kiel2004). Horton et al. (Reference Horton, Millo and Serafeim2012), Renneboog and Zhao (Reference Renneboog and Zhao2011), and Omer et al. (Reference Omer, Shelley and Tice2014) suggest that the higher the value of this indicator, the faster information transfers within the network. The shorter the social path between individual directors within the same network, the higher the quality of information available to each director (Larcker et al., Reference Larcker, So and Wang2013).

All the variables above are calculated at the director level, but they can also be applied at the firm level. Horton et al. (Reference Horton, Millo and Serafeim2012) state that a firm establishes connections through well-connected directors, and thus, the network position of a firm's directors collectively yields a network position for the firm. Like Horton et al. (Reference Horton, Millo and Serafeim2012), we measure the network measures of each firm by aggregating the network measures for each director within each firm.

For our politically connected directors, we base the identification of the directors on the firms identified by Johnson and Mitton (Reference Johnson and Mitton2003). The directors in these firms are then categorized as politically connected directors, and we recalculate the network centrality measures.

Corporate Governance Variables

We have two sets of corporate governance variables: internal and external governance mechanisms. Internal governance mechanisms consist of board characteristics and audit committee characteristics. Board characteristics are captured by three variables. The first is the number of directors on the board (BSIZE), for which we predict a nondirectional relationship with earnings quality. On the one hand, the number of directors reflects the amount of resources and connections firms have, and this could have a positive impact on earnings quality. On the other hand, an increase in the number of directors could suggest delays in decision making, which could impair earnings quality.

The second board characteristic variable takes the value of 1 if the proportion of independent directors is more than two-thirds of the board and zero otherwise (BIND). We predict a positive relationship between BIND and earnings quality since we expect monitoring by the board to increase as the number of independent directors increases. Better or enhanced monitoring should limit managerial discretion in relation to accounting policy choices and thus reduce the residual in the accruals model. The next corporate governance variable is duality or the ‘dominant personality’ phenomenon (Haniffa & Cooke, Reference Haniffa and Cooke2002), whereby the CEO is also the chairman of the board (DUALITY). According to resource dependence theory (Boyd, Reference Boyd1995), duality promotes the unity of leadership and facilitates organizational effectiveness (Stewart, Reference Stewart1991). Alternatively, agency theorists suggest that the board should be independent of management to prevent managerial entrenchment (Fama & Jensen, Reference Fama and Jensen1983). Based on this argument, we predict a nondirectional relationship between DUALITY and earnings quality.

Audit committee characteristics consist of audit committee independence and audit committee diligence (audit committee meetings), as proposed by He, LaBelle, and Piot (Reference He, Labelle, Piot and Thornton2009). Similar to Bedard and Johnstone (Reference Bedard and Johnstone2004) and Klein (Reference Klein2002), we operationalize audit committee independence as a binary variable that takes the value of 1 if all the members are independent directors and zero otherwise (ACIND), while audit committee diligence (ACMEET) is the number of annual meetings by audit committee members. Audit committees are expected to monitor the reliability of the firm's accounting process and compliance; hence, this should mitigate managerial discretion and increase earnings quality (Turley & Zaman, Reference Turley and Zaman2004). Based on this argument, we predict a positive relationship between audit committee independence (ACIND) and earnings quality. Lin and Hwang (Reference Lin and Hwang2010) argue that the number of meetings by an audit committee is important if there is to be ample time for them to make sound, informed decisions and thus increase the level of monitoring.

Our first external governance variable is the percentage of the top five institutional investors (INSTOWN), for which we predict a positive relationship with earnings quality. One would expect institutional investors to have the size and expertise to monitor firms. In addition, the role of institutional investors in Malaysia has significantly increased since the Asian financial crisis with the establishment of the Minority Shareholders Watchdog Group (MSWG) with the five main institutional investors in Malaysia as founding members. Abdul Wahab, How, and Verhoeven (Reference Abdul Wahab, How and Verhoeven2007) find a positive relationship between institutional investors and firm performance, which supports the argument that institutional investors play a monitoring role by requesting better governance of directors.

We include another external corporate governance variable, auditor size. Auditor size (BIG4) takes the value of 1 if the firm is audited by a Big 4 auditing firm and zero otherwise. Big 4 auditors are subject to the ‘deep pocket’ effect, whereby they provide better quality auditing to protect themselves from litigation by clients. In addition, the Big 4 auditors have reputational capital, resources and experience, which should result in better earnings quality. Fan and Wong (Reference Fan and Wong2005) investigate whether Big 4 auditors play a governance role in East Asian economies, and find that firms in East Asian countries are likely to hire Big 5 auditors as agency conflicts increase. This suggests that auditors do play a governance role in relation to reducing agency conflicts. We therefore predict a positive relationship between BIG4 and earnings quality.

Institutional Variables

To provide a more holistic view of Malaysia's capital market, we include three institutional variables that are widely established in the literature. The first is the proportion of Bumiputera directors on the board (BUMI), which is our proxy for culture. Studies have used the Hofstede-Gray framework to provide a link between culture (proxied by ethnic group) and accounting disclosure. Based on the Hofstede-Gray framework, Malays may be expected to be relatively more secretive than their Chinese counterparts, which implies lower disclosure (Haniffa & Cooke, Reference Haniffa and Cooke2002). Lower disclosure could affect the level of information asymmetry, and this should have an adverse effect on earnings quality. Based on this framework, we posit a negative relationship between BUMI and earnings quality. Abdul Wahab, Allah Pitchay, and Ali (Reference Abdul Wahab, Allah Pitchay and & Ali2015) investigate the relationship between Bumiputera directors and analysts’ forecast errors and find a positive relationship, lending support to the Hofstede-Gray framework.

The second is an indicator variable that takes the value of 1 if the firm is a family firm (FAMILY). The Malaysian capital market is dominated by family-controlled firms (Claessens, Djankov, & Lang, Reference Claessens, Djankov and Lang2000), which suffer from higher agency problems due to conflicts between majority and minority shareholders. Due to the heightened agency conflicts in these firms, we predict a negative relationship between family control of firms and earnings quality. Munir, Saleh, Jaafar, and Yatim (Reference Munir, Saleh, Jaffar and Yatim2013) find a nonlinear relationship between family control of firms and earnings quality, while Wan Hussin (Reference Wan-Hussin2009) finds a positive relationship between family control of firms and segmental disclosure in Malaysia. The third institutional variable is POLCON, which takes the value of 1 if the firm has at least one director identified as politically connected based on the firms listed by Johnson and Mitton (Reference Johnson and Mitton2003), and a negative relationship is predicted.

Control Variables

We include the natural log transformation of total assets (ASSETS) to control for firm size. Larger firms face stricter regulations and are under greater scrutiny by external monitors, constraining the ability of managers to manipulate earnings (Pincus & Rajgopal, Reference Pincus and Rajgopal2002). In support of this theory, several studies find that earnings quality is lower in smaller firms (Simpson, Reference Simpson2013). Next, we control for leverage (DEBT), which we operationalize as total debt scaled by total equity. According to the debt covenant hypothesis, firms engage in aggressive earnings management, and thus lower earnings quality, practices when approaching the violation of their debt covenants (Bartov, Gul, & Tsui, Reference Bartov, Gul and Tsui2000).

We include an indicator variable that takes the value of 1 if the firm records a loss during the year (DLOSS). Some studies have shown that earnings management is more prevalent in poorly performing firms (Kothari, Leone, & Wasley, Reference Kothari, Leone and Wasley2005). In a similar vein, Dechow, Sloan, and Sweeney (Reference Dechow, Sloan and Sweeney1995) find that models of discretionary accruals are least reliable when used on companies exhibiting extreme performance. In contrast, DeGeorge, Patel, and Zeckhauser (Reference DeGeorge, Patel and Zeckhauser1999) find that highly performing firms engage in earnings management practices to meet earnings expectations. While this study predicts that firm performance is associated with earnings management, the predicted sign is unclear. The fourth control variable, market-to-book value (MTBV), controls for growth opportunities; we predict a negative relationship between MTBV and earnings quality. Finally, we control for unobserved variation in the industries by including an industry fixed effect (INDUSTRIES). Appendix A presents the operational definitions of the variables.

RESULTS

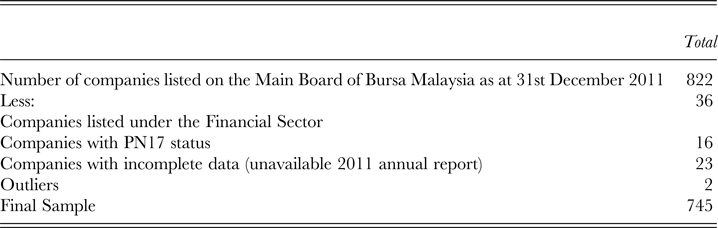

The sample in this study consists of 4,416 directors from 745 firms listed on Bursa Malaysia in 2011. We started with 822 firms listed on the Main Board of Bursa Malaysia as of 31 December 2011. We excluded financial firms (36) and firms that fall under PN17 (16) status as per 2011, as shown in Table 1.[Footnote 4] Twenty-three firms were without 2011 annual reports, and we excluded two outliers, ending up with 745 firms for our sample.

Table 1. Sample selection

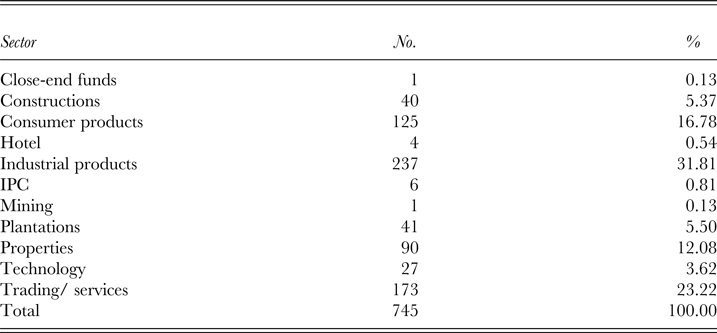

Table 2 presents the industry classifications. Industrial product firms account for 31.81 percent of those in the sample (237 firms), followed by trading and services firms at 23.22 percent (173 firms). The sample also includes one closed-end fund and one mining firm.

Table 2. Industries classifications

The directors’ details (name and political connections) were hand-collected from annual reports. Corporate governance variables were also hand-collected from the annual reports made available on Bursa Malaysia's website. Data on firm characteristics were extracted from Datastream. The network measures were derived from the social network software UCInet.[Footnote 5]

Data Description

Table 3 presents the descriptive statistics for the sample in this study. The mean for our measure of earnings quality (AQ) is -0.06, with a range between 0.00 and -0.91. Panel A of Table 3 tabulates the figures for our network measures. The mean for DEGREE-IN is 12.11, which indicates that, on average, directors in a firm have 12.11 direct connections within firms and to external firms. Our next direct measure, DEGREE-EX, averages 4.70, which denotes that, on average, directors have 4.70 direct connections with external directors. The third direct measure, EIGEN, is 0.003, which implies that directors have connections to better-connected directors in the sample. Our indirect measures, BETWEENNESS, and CLOSENESS, average 1124.75 and 91.28, respectively.

Table 3. Descriptive statistics (n = 745)

Note: Please refer to Appendix I for the operational definitions of variables.

The average of normalized degree centrality (NDEGREE-IN) suggests that, on average, a firm in the network has direct connections to 9 percent of all other firms. NDEGREE-EX, NCLOSENESS, NBETWEENNESS, and NEIGEN average 6 percent, 12.24 percent, 41 percent, and 48 percent of their respective theoretical maximum. An average of 1124.75 for BETWEENNESS equates to 0.13 percent of indirect connections running through a firm.[Footnote 6]

Panel B of Table 3 tabulates the descriptive statistics for corporate governance variables. The average size of the board of directors is 7.42 members, with a range of 3 to 18 directors. Only 28 percent of the sample firms combine the functions of CEO and chairperson (DUALITY), and 6 percent have boards on which more than two-thirds of directors are independent (BIND). Audit committees meet (ACMEET), on average, 4.92 times per year, and 62 percent of sample firms have only independent directors on their audit committee. Institutional ownership (INSTOWN) averages 2.90 percent, and 54 percent of sample firms are audited by a Big 4 firm (BIG4). Panel C tabulates the descriptive statistics for our institutional variables. Bumiputera directors (BUMI) make up, on average, only 33 percent of a board, and 44 percent of the firms are POLCON (Johnson & Mitton Reference Johnson and Mitton2003).[Footnote 7]

Of our sample firms, 21 percent are family connected (FAMILY). Our control variables, the natural log transformation of total assets (ASSETS) and the proportion of debt to total equity (DEBT), average 19.84 and 0.49, respectively; these are presented in panel D of Table 3. The average (median) for MTBV is 1.38 (0.56), while 20 percent of sample firms record a loss (DLOSS) during the period.

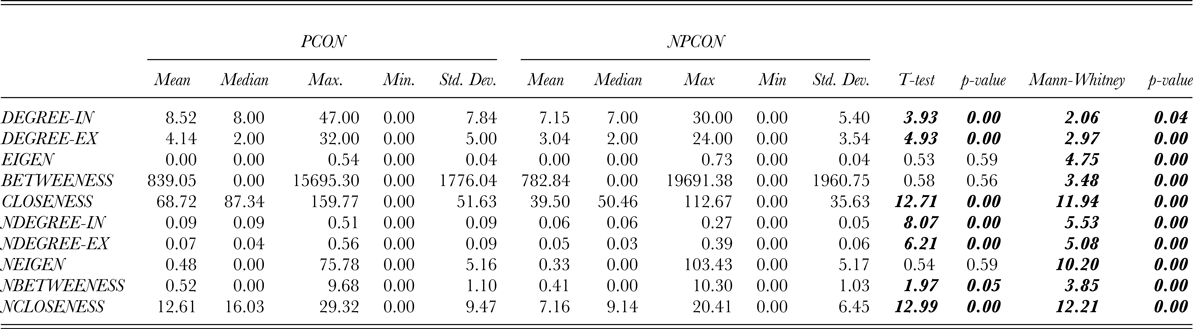

Table 4 presents the descriptive statistics for the network measures for both politically and nonpolitically connected directors. Politically connected directors have, on average, (median), 8.52 (8.00) direct connections (internal and external) relative to 7.15 (7.00) direct connections for nonpolitically connected directors, and the differences are significant. Eveland Jr, Hutchens, and Morey (Reference Eveland, Hutchens and Morey2013) state that political network size correlates with the frequency of political conversation and that this translates to critical political outcomes such as knowledge and participation. Eveland Jr et al. (Reference Eveland, Hutchens and Morey2013) also state that a larger network is likely to contain a more diverse set of individuals compared to smaller networks. Further, Eveland Jr et al. (Reference Eveland, Hutchens and Morey2013) state that a larger political network is composed of a mix of strong and weak ties. The value of weak ties is that they provide access to different perspectives relative to stronger ties (Brown et al., Reference Brown, Gao, Lee, Stathopoulos, Boubaker, Nguywen and Nguywen2012). The YTL Cement Berhad dominates the DEGREE-IN, DEGREE-EX, and NEIGEN values.

Table 4. Network measures for politically and non-politically connected directors

Notes: PCON stands for politically-connected directors while NPCON is non-politically-connected directors.

Please refer to Appendix I for the operational definitions of variables.

We find significant differences in external connections (DEGREE-EX) for politically connected and nonpolitically connected directors. For EIGEN, we find a significant difference in the median between the two samples.

Politically connected directors are more central in the network, as demonstrated by significantly higher BETWEENNESS and CLOSENESS relative to nonpolitically connected directors. These figures suggest that politically connected directors have shorter distances between each other, which suggests that they are a close-knit community. The higher BETWEENNESS and CLOSENESS figures for politically connected directors (PCON) suggest that information could travel faster and hence make it reliable. However, it could also indicate that such directors are unable to source alternative information or resources and that the information is relatively redundant in nature. This could have an adverse effect on earnings quality.

Our descriptive statistics suggest that politically connected directors have more direct and indirect connections than nonpolitically connected directors do. In addition, politically connected directors are more central in the network and closely connected to each other. This finding provides some evidence that the relationship-based economy in Malaysia is a crucial foundation for the capital market. In summary, politically connected directors have more contacts, more visibility, and more centrality in the network.

Univariate Analysis

Table 5 presents the correlations, both Pearson and Spearman-rank. The correlations between the network measures are above 0.50 and significant at the 1 percent level. We find positive and significant correlations (only for Pearson) between AQ and the network measures, except for NEIGEN. This provides initial support that networking between directors prevents effective monitoring and is harmful to earnings quality. In addition, we observe significant correlations between the network measures. The Pearson correlations between NDEGREE-IN and NBETWEENNESS and NCLOSENESS are 0.65 and 0.73, respectively, and significant at the 1 percent level, which indicates that these measures, either direct or indirect, measure a similar dimension of the network.

Table 5. Correlations (n = 745)

Notes: Please refer to Appendix I for the operational definitions of variables. ***, ** and * denote significance at 1%, 5% and 10% respectively

Multivariate Analysis

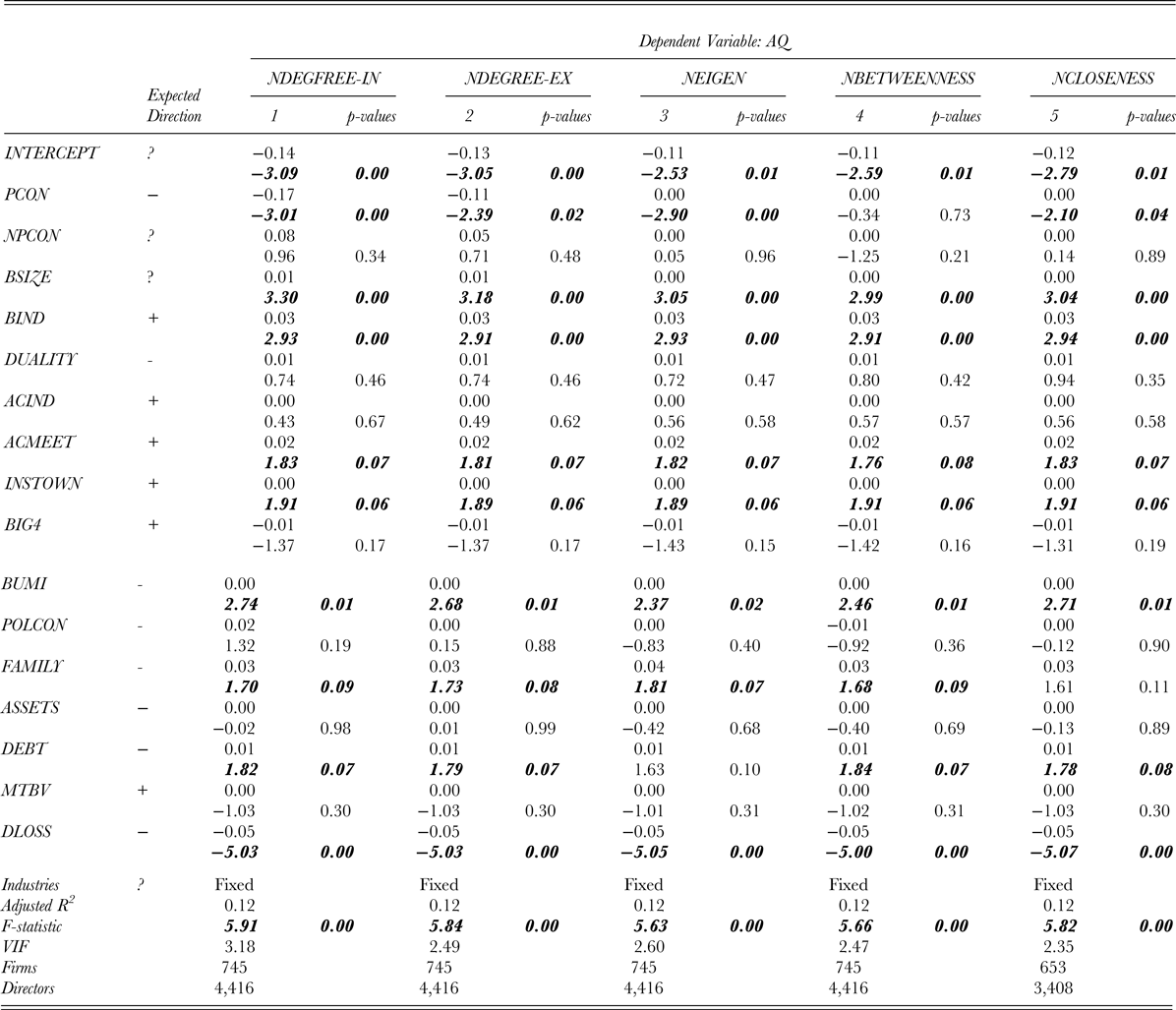

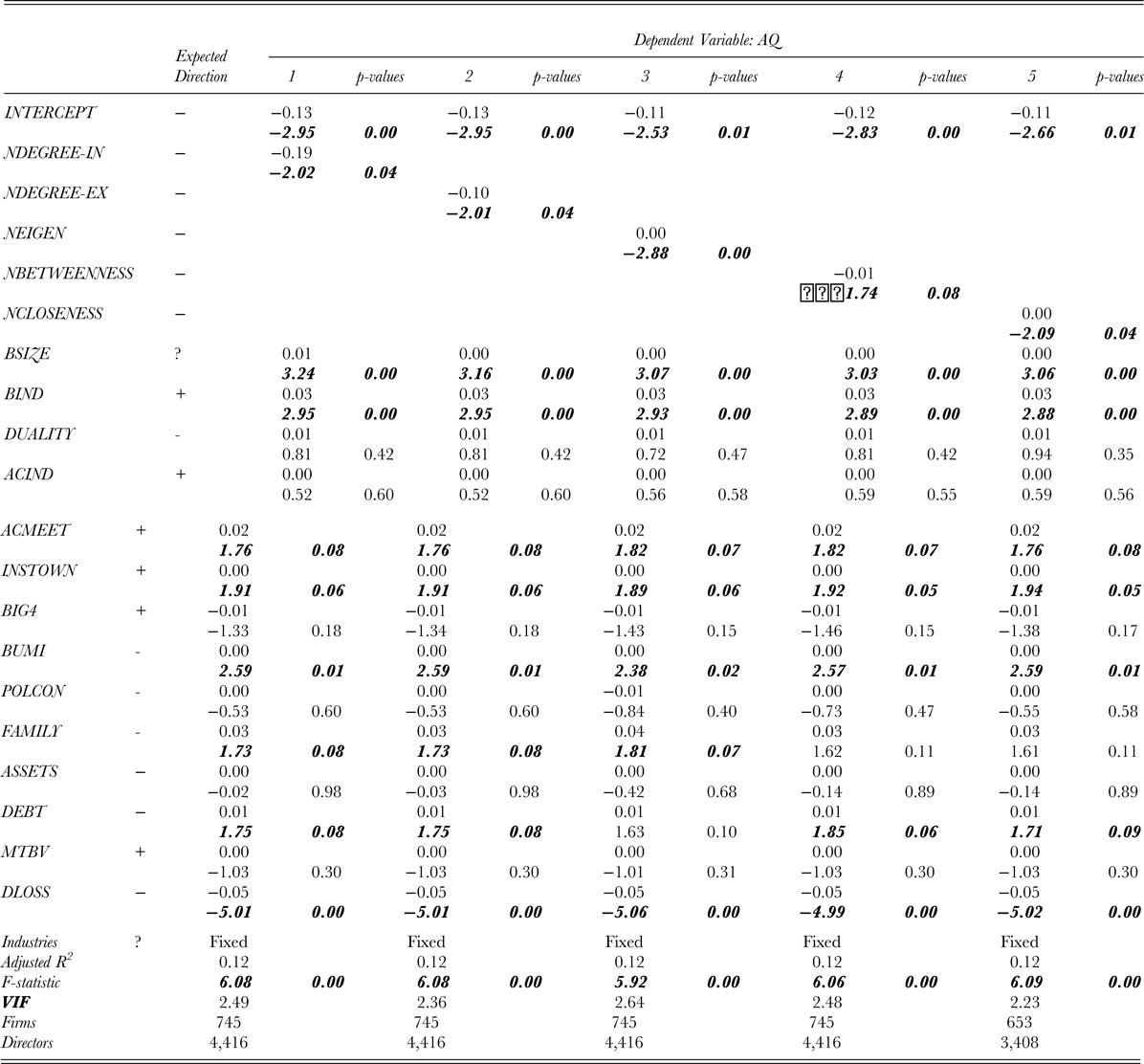

Directors network. Table 6 presents the results of our main regression for H1 based on a sample of 745 firms in 2011. Columns 1 to 5 report the results for NDEGREE-IN, NDEGREE-EX, NEIGEN, NCLOSENESS, and NBETWEENNESS, respectively. We find a negative and significant coefficient of −0.19 (p = 0.04) for NDEGREE-IN and −0.10 (p = 0.04) for NDEGREE-EX, which suggests that the direct internal and external ties of directors have a negative impact on earnings quality, as tabulated in columns 1 and 2 of Table 6. We find a negative and significant relationship between NEIGEN (β = 0.00, p = 0.00) and earnings quality. Our next two measures, NBETWEENNESS (β = −0.01, p = 0.08) and NCLOSENESS (β = 0.00, p = 0.04), yield a negative and significant relationship with earnings quality. Although all the network measures are negatively and significantly related to accruals quality, the economic impact differs. For instance, the regression coefficient implies that an increase of one standard deviation of NDEGREE-IN (please see Table 3, 0.04) would decrease earnings quality by 0.14 (or 14 percent).[Footnote 8]

Table 6. Main regression (n = 745)

Note: Please refer to Appendix I for the operational definitions of variables.

Based on a similar approach, the relative economic impacts of NDEGREE-EX, NEIGEN, NBETWEENNESS, and NCLOSENESS are 0.10, 0.52, 0.72, and 0.70, respectively. The relative economic impact provides an interesting outcome. The brokerage position (NBETWEENNESS) and the distance (NCLOSENESS) reflect how information travels within the network and have a more negative impact on earnings quality. This supports the argument of Larcker et al. (Reference Larcker, So and Wang2013) that the information that travels within the network could be false or redundant. Although the other three network measures have a smaller economic impact, the results suggest that they do affect earnings quality negatively.

The findings support the argument that networks created by directors demonstrate board busyness, which prevents them from being effective monitors (Andres et al., Reference Andres, Bongard and Lehmann2013; Ferris et al., Reference Ferris, Jagannathan and Pritchard2003; Larcker et al., Reference Larcker, So and Wang2013). The findings also support the notion that appointees are concerned with their social status and adhere to management decisions as part of the reciprocity arrangements on the board (Mizruchi, Reference Mizruchi1996). In addition, the results could suggest that information that travels within a network directly does not provide any benefit to the organization and that false information is being distributed (Larcker et al., Reference Larcker, So and Wang2013). The negative relationships we find between our network measures and earnings quality suggest that the quality of information is minimal and indicates that the number of intermediaries lessens the positive outcome of the information (Omer et al., Reference Omer, Shelley and Tice2014).

We find a positive relationship between board size (BSIZE) and earnings quality (β = 0.01, p = 0.00), indicating that earnings quality improves with larger boards; this supports the notion that larger boards bring better resources to the firm and enhance monitoring. In addition, we find a positive and significant relationship between BIND (β = 0.03, p = 0.00) and earnings quality, lending support to the idea that a high level of board independence serves to improve corporate governance monitoring. However, we find an insignificant relationship between DUALITY and earnings quality (β = 0.01, p = 0.42), which suggests that the separation of power between the CEO and chairperson does not affect earnings quality. We find a positive and significant relationship between ACMEET (β = 0.02, p = 0.08) and AQ, suggesting that the frequency of audit committee meetings signals a suitable monitoring mechanism that increases earnings quality.

Our external governance variable, INSTOWN (β =0.00, p = 0.06), is positively and significantly related to earnings quality, suggesting that institutional investors in Malaysia do play a governance role. This result supports the findings of Abdul Wahab et al. (Reference Abdul Wahab, How and Verhoeven2007) on the role of institutional investors in Malaysia. Contrary to our expectations, we find no relationship between BIG4 (β = −0.01, p = 0.18) and earnings quality, which suggests no differences in monitoring capabilities among the large and smaller auditing firms. The finding on BIG4 could indicate that the litigation risk is rather minimal in Malaysia relative to developed nations such as the US or in the UK and thus that auditor size is less important in relation to monitoring and the earnings quality of firms.

As per our institutional variables, we find that the proportion of Bumiputera directors (BUMI) is positively and significantly related to earnings quality (β = 0.00, p = 0.01), and our finding is consistent with Haniffa and Cooke (Reference Haniffa and Cooke2002). We find that family firms (FAMILY) record better earnings quality (β = 0.03, p = 0.08), but we can find no support for a relationship between political connection (POLCON) and earnings quality. We view the insignificant finding for POLCON as suggestive that these firms have higher agency costs and thus have a detrimental impact on earnings quality.

We find a positive relationship between DEBT (β = 0.01, p = 0.08) and earnings quality. In addition, we find a negative relationship between DLOSS and AQ (β = −0.05, p = 0.00), which suggests that firms that record a current loss have lower earnings quality. Finally, we find no support for any relationships for ASSETS (β = 0.00, p = 0.98) and MTBV (β = 0.00, p = 0.30), which suggests that firm size and growth are not determinants of earnings quality. The adjusted R2 for the regression models stands at 12 percent, while the mean-variance inflation factors (VIF) for all variables range from 2.23 to 2.64, suggesting that the regressions do not suffer from multicollinearity issues. The adjusted R2 is comparable to that of other studies, such as that of Srinidhi and Gul (Reference Srinidhi and Gul2007), which records a similar range of results. The recorded adjusted R2 could be due to an unobserved effect that we are unable to capture with single-year data, as fixed-effect models with multiple years could increase the power to explain the variance in the model. Further, as suggested by Neter, Wasserman, and Kutner (Reference Neter, Wasserman and Kutner1983), a VIF of less than 10 can be taken as a sign that multicollinearity is unlikely to be an issue.

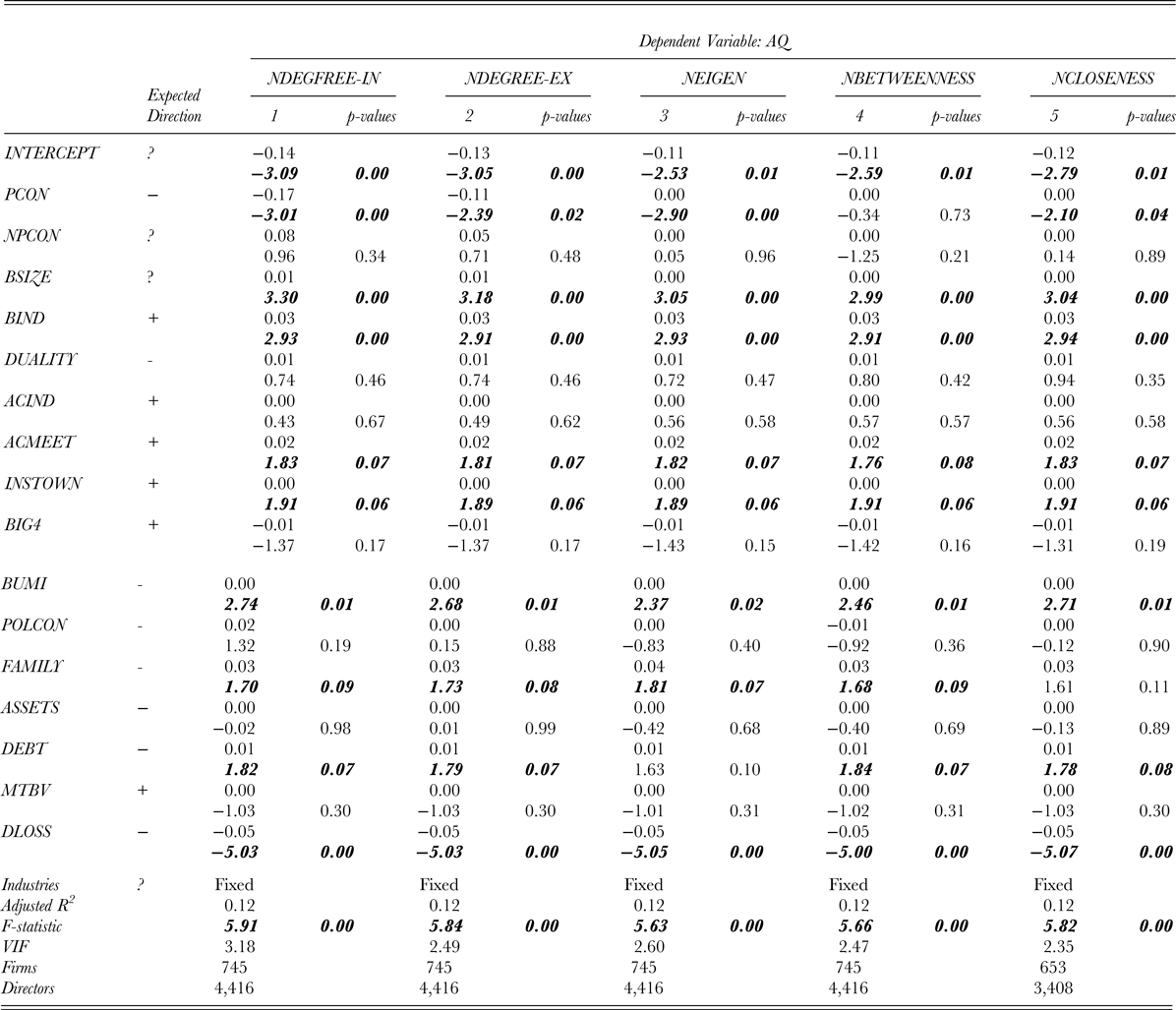

Politically connected network. Table 7 contains the results of our regression to test H2 and H2a, with columns 1 to 5 reporting the outcomes for the network measures established earlier. The estimation results in columns 1 and 2 show that the degree measures NDEGREE-IN (β = −0.17, p = 0.00) and NDEGREE-EX ( β =−0.11, p = 0.02) are associated with lower earnings quality. The NEIGEN, as shown in column 3 of Table 7, shows a significant coefficient (β = −0.00, p = 0.00), while NCLOSENESS records a similar negative and significant coefficient (β =−0.00, p = 0.04) in relation to earnings quality. However, we find an insignificant relationship between NBETWEENNESS (β = −0.00, p = 0.73) and earnings quality. In general, our regression results lend support to H2, in that we find a negative relationship between the political connectedness of the network of directors and earnings quality.

Table 7. Regressions for firms with PCON and NPCON directors

Note: Please refer to Appendix I for the operational definitions of variables.

Our results support the argument that having a politician as a director presents a cost to the firm. Our findings generally support the arguments that politicians appear to be a risk to the firm and that this creates uncertainty. In addition, lower earnings quality suggests that they might not be interested in producing high-quality information. Our findings support the argument that politically connected directors are concerned with social status and disruption to network cohesion (Mizruchi, Reference Mizruchi1996). In addition, the findings also suggest that political appointees do not disagree with management having been appointed to the board (Westphal & Zajac, Reference Westphal and Zajac1997).

Our findings support the notion that politically connected directors are often seen as a symbolic fulfillment of the NEP's objectives (Gomez, Reference Gomez and Gomez2002). Although shown earlier, that PCON directors are close to each other could suggest that they are face difficulties in verifying the information they have access to. In addition, the higher number of connections indicates that PCON directors are busy directors, which prevents them from monitoring the firms. The nature of the Malaysian capital market could also suggest that these appointments are somewhat symbolic and ceremonial in nature and serve to give firms connections to and protection from the government.

Sensitivity Analysis – Alternative Measures of Earnings Quality

This study uses two other discretionary accruals measures from Francis et al. (Reference Francis, LaFond, Olsson and Schipper2005) as alternative measures for accruals quality. The first alternative measure is the modified Jones model (JONES), which we use to estimate discretionary accruals (DuCharme, Malatesta, & Sefcik, Reference DuCharme, Malatesta and Sefcik2004; Habib, Bhuiyan & Islam, Reference Habib, Uddin Bhuiyan and Islam2013). Our second model is the Kothari et al. (Reference Kothari, Leone and Wasley2005) (KOTHARI) performance-adjusted discretionary accruals model, in which we add the previous year's performance (return on assets) as an independent variable in the modified Jones model. Our alternative measures for discretionary accruals, modified Jones (JONES) and performance-adjusted (KOTHARI) accruals, record means of −0.21 and −0.18, respectively.

Director networks – Aleternative mearns on earnings quality. Our measures of networking degree are both negative and significantly associated with JONES. NDEGREE-IN records a coefficient of −0.75 (p = 0.01), while NDEGREE-EX has a coefficient of −0.42 (p = 0.01), which results in an economic impact of 0.14 and 0.12 per percentage point, respectively. The third measure, NEIGEN, is also negative and significant (β = −0.00, p = 0.01) to JONES. These results are consistent with our primary measure of earnings quality from Francis et al. (Reference Francis, LaFond, Olsson and Schipper2005). However, we find no evidence of a relationship of the NBETWEENNESS (β = −0.02, p = 0.23) and NCLOSENESS (β = 0.00, p = 0.15) measures with JONES.

NDEGREE-IN and NDEGREE-EX record coefficients of −0.66 (p = 0.01) and −0.36 (p = 0.01) and translate to 0.15 and 0.12 percentage point decreases in KOTHARI, respectively. Similar to Tables 6, we find a negative and significant relationship with NEIGEN (β = −0.00, p = 0.06) and KOTHARI. (Please refer to Appendix B online at https://osf.io/wdmv7/).

Politically-connected network – Alternative measures of earnings quality. We extend the analysis by examining the impact of PCON and NPCON directors on the alternative measures of earnings quality, Our untabulated results find a negative and significant relationship between PCON and JONES for all network measures with two exceptions: NBETWEENNESS and NCLOSENESS. Interestingly, we find a negative and significant relationship for NPCON directors and JONES for NBETWEENNESS and NCLOSENESS. We find similar results when we opt for KOTHARI as our earnings quality measure. (Please refer to Appendix C online at https://osf.io/wdmv7/).

DISCUSSION

We are motivated to investigate the relationship between director networks and earnings quality because there is a lack of evidence on this issue. According to resource dependence theory, the network created by directors should provide opportunities for securing resources and building economies of scale. Since director networks are closely linked to board interlocks, the size of a director's network could suggest an increase in the number of his or her professional commitments, and this could limit monitoring if directors are unable to provide sound feedback to the firm.

In a sample of 745 firms listed on Bursa Malaysia for the year 2011 and the 4,416 individual directors, we find that greater director network connectedness is detrimental to earnings quality in Malaysia. Our primary results are robust when we use multiple measures of director network connectedness, as shown in Table 6. We extend this analysis by examining two other well-known accruals models, the modified Jones and the Kothari models, as alternative dependent variables. The untabulated results find that three director network measures have a negative relationship with earnings quality based on the alternative models: NDEGREE-IN, NDEGREE-EX, and NEIGEN.

Our second main objective is to examine the role of directors' political connections in earnings quality. Malaysia provides an interesting case, as Faccio (Reference Faccio2006) highlights, as the country with the second-highest number of politically connected firms. In addition, given the social background of the country and its close relationship with the development of the capital market, the examination of this network is rather timely. We reconstruct the network measures by identifying politically and nonpolitically connected directors in the sample. We find, in general, that politically connected directors and the network they create are detrimental to the earnings quality of the firms. Our evidence suggests that the appointment of these directors to boards is largely ceremonial (Gomez, Reference Gomez and Gomez2002), providing little or no contribution to the firm. Although the connected directors position themselves in a better brokerage position then do directors in nonconnected firms, the information that flows through them may be redundant or false (Larcker et al., Reference Larcker, So and Wang2013). In fact, the negative and significant finding could suggest that the appointment of politically connected directors could lead to the expropriation of assets and politicians tapping into firms’ resources for personal or political gains (Case, Reference Case2017).

From a theoretical standpoint, our study primarily contributes to the literature on informal networks by examining the impact of director networks on earnings quality. With regard to the network literature, our work is one of the few studies that extend the growing literature by examining the network created by politically connected directors. Existing studies on political connections have only been confined to a dichotomous measure, while our study took a deeper approach by examining the dimensions of the network of connected directors. We extend the argument raised by Hillman et al. (Reference Hillman, Withers and Collins2009) in relation to the need for more studies on the role of resource dependence theory on political connections. In addition, we raised an important point that understanding the institutional background is essential to understanding whether networks provide benefits.

From a practical standpoint, two implications can be derived from this research. First, although not explicitly, this research warrants further investigation on the nature of appointments of directors to boards. Our findings imply that to increase monitoring and enhance the quality of resources, the number of multiple directorships should be limited to a certain number of appointments. The second implication involves the role of politicians on boards of directors and, subsequently, in the capital market.

Limitations and Future Research Implications

This study is not without limitations. The first limitation is the high unexplained variance observed of 82 percent in our regressions, which suggests that other factors could explain the relationship. Among the factors are the similarities among the directors such as educational background, expertise (Macus, Reference Macus2008), alumnus affiliation (Koka & Prescott, Reference Koka and Prescott2008) which could further explain the impact of the network on earnings quality. One would expect the similarities or ‘homophily’ (McPherson, Smith-Lovin, & Cook, Reference McPherson, Smith-Lovin and Cook2001) could strengthen the investigation on social networks. Another potential factor that could further explain the relationship is the political conglomerate that possibly exists in Malaysia.

The unexplained variance in relation to earnings quality could be attributed to the nature of our data. We are constrained by the fact that we have to extract the names of the directors manually from downloaded annual reports published on Bursa Malaysia's website. We are limited to only one year of directors’ data due to the nature of collecting the data. A longitudinal data of 3 years or more could provide more information and mitigate any possible unobserved impact relative to a snapshot (1 year) of data. Furthermore, longitudinal data would provide better insight into whether such networks change over time and thus present a better understanding of the impact of the network on earnings quality.

The analyses to test the hypotheses might suffer from several measurement and testing issues, primarily our choice of the dependent variable of earnings quality. Although we provide two measures to demonstrate robustness, these measures do suffer from several limitations. Dechow et al. (Reference Dechow, Ge and Schrand2010) state that the definition of earnings quality is dependent on several factors. First, earnings quality is conditional upon the decision relevance of the earnings information. Second, the quality of the reported earnings number depends on whether it provides information about a firm's financial performance, which is mostly unobservable. Third, earnings quality is jointly determined by the relevance of underlying financial performance to the decision that the earnings interpretation relates to and by the ability of the accounting system to measure performance (Dechow et al., Reference Dechow, Ge and Schrand2010). Alternatively, other measures of earnings quality, such as earnings conservatism or earnings persistence, could be used as the dependent variable for this study. Future research measuring the impact of director networks could take into consideration other direct management activities, such as risk-taking and investment decisions.

Future research in networks among directors could explore the link between resource dependence and agency theory as mooted by Hillman and Dalziel (Reference Hillman and Dalziel2003) and Zona, Gomez-Mejia, and Withers (Reference Zona, Gomez-Mejia and Withers2018). These papers provide an avenue for further convergence of arguments regarding the role of the board of directors and earnings quality.

CONCLUSION

This study examines the relationship between director networks and earnings quality in Malaysia. Based on a sample of 4,416 directors for 745 firms in Malaysia during 2011, we find that overall, greater connectedness of director networks negatively affects accruals quality, our proxy for earnings quality. Our findings provide support for the argument that networking by directors distorts managerial influence, demonstrates board busyness, and prevents effective monitoring. The results also support the contention that limiting the movement of beneficial information across networks could enhance earnings quality.

We extended our analysis by recalculating the network measures based on a key feature of the institutional setting in Malaysia, political connections. Our extended analysis of politically connected directors finds that the political connectedness negatively affects earnings quality, but we find no evidence of a relationship between the connectedness of nonpolitically connected directors and earnings quality.

APPENDIX I

Operational Definitions of Variables