This discussion relates to the paper presented by Shelagh Young and Susan Murray at the IFoA sessional event held on 23 January 2023.

The Moderator (Mr N. Chadha, F.I.A.): I am Nick Chadha, a member of the Institute and Faculty of Actuaries (IFoA)’s Scottish Board.

At the start of 2020, the IFoA launched its campaign on “the Great Risk Transfer.” The IFoA explored the trend of the transfer of risks, from institutions such as employers, the State and financial services providers, to individuals.

The key goals of the campaign were:

To gather and share evidence about the Great Risk Transfer and its impact across society.

To bring stakeholders together to debate the evidence and potential actions that can be taken to address the trend.

To propose recommendations for action and to work with stakeholders, including government and regulators, to drive actions that will have a positive impact on the public interest.

The IFoA published their interim findings report in July 2020, and their final findings report in April 2021. The cumulation of the IFoA’s work resulted in two key policy recommendations. Firstly, there needs to be a rebalancing of risks. In particular, it is believed that there are opportunities to ease the burden for consumers by shifting the prime responsibility for certain risks back towards institutions. The mechanism for achieving this is structural changes to markets, products and services and the legal and regulatory frameworks that shape them. Secondly, consumers need help so that they can manage their financial risk through good decision-making. A key driver for new products and services should be to help consumers with the complex decisions involved in managing financial risks effectively and affordably. This could dramatically improve outcomes for many people and for society as a whole.

In the summer of 2021, the Scottish Board was approached by the David Hume Institute (DHI). The DHI was very interested in the Great Risk Transfer and wanted to delve into the analysis further. Building on the four important areas of risk transfer – pensions, work, health, and insurance – the DHI wanted to complete a research project to find out more about relevant perceptions of risk in the Scottish population, and how people respond to risks that can affect their financial well-being.

Shelagh Young and Susan Murray are the speakers for tonight. Shelagh is the engagement lead for the David Hume Institute. Shelagh is an experienced leader, writer and facilitator in the not-for-profit and cooperative sector. Her focus at the DHI is on ensuring their work is informed by the widest possible range of people. Shelagh moved from journalism to in-house communications, joining Oxfam GB before moving to Scotland to focus on leadership development with disabled people and their families. She was chair of the UK’s only cooperative telecoms provider, the Phone Co-op, and a Founding Director of the sustainable food and farming organisation, Nourish Scotland.

Susan (Murray) joined the Institute as a Director in November 2019. She is committed to diversity of thought and was a founding trustee of the Institute of Chartered Accountants of Scotland (ICAS) Foundation, which aims to increase the diversity of young people entering the financial profession. Susan is a core social leadership fellow and has studied at the University of Edinburgh, Goldsmiths (University of London), and Aberdeen Business School. She is a member of the Institute of Directors as well as the charity Changing the Chemistry.

Ms S. Young: This research took place from early to late spring in 2022. It is interesting to speculate what the findings would be if we were talking to people now, given that conditions have materially changed in the interim. For example, the Joseph Rowntree Foundation issued a report this week reminding us that 2.4 million mortgagees are now living in poverty, judged by official measures. They think that, by the end of this year, if the mortgage rate is around 5.5%, another 400,000 people will be added to that total. This is an example of the types of risks in people’s everyday lives that I think have really shifted since we did this fieldwork.

The IFoA’s fieldwork had focused primarily on professionals. We wanted to talk to ordinary people and see what they thought about the balance of risk in their lives. We spoke to nearly 50 people face-to-face using a semi-structured interview, and we also did a population-level survey. When I make comments about what people told us, I will make the distinction between prompted and unprompted responses because we started off by asking very open questions. We did some initial scoping work, as it was very hard to get people to engage with the subject of risk. We had to simplify our approach to make it easier for people to understand what we were trying to get them to think about.

As Nick (Chadha) said, the IFoA’s report was talking about the transfer of risk from employers, the State and other institutions, and it stated that this is a significant but little-understood challenge. We wanted to see if we could understand how ordinary people perceived this. A number of factors driving this shift were identified in the original report. Among those mentioned were increased longevity, advances in technology, low-interest rates and changes in financial regulation.

The IFoA also mentioned that levels of numeracy, financial literacy and understanding of risk are generally low. There is a great deal of research that shows how people struggle with these things, and that is a really important factor to bear in mind when we come to some of our findings.

Our first question to people, either in groups or one-to-one, was very open. We asked what they understood to be the main long-term risks to their financial well-being. Well-being, money and finance all had resonance with people. It was difficult for people to grasp what we were interested in when we asked about risk without those ideas.

In the IFoA’s report, key areas were pensions, work, health and insurance. There were other items, but these were the key areas mentioned. When we spoke to people, housing came out really strongly. When we asked about risk, they talked about their housing situation. Pensions also featured prominently, as well as health to a slightly lesser extent. Work and insurance were not front of mind for people. We spoke to people who were securely ensconced in homes where the mortgage had long been paid off, so some older, wealthier people, and we also spoke to people living in rented accommodation. The interesting thing about those older people was their concern for others, such as members of the younger generation in their own family, and their ability to achieve some form of financial security through housing, which was seen as becoming out of reach for even quite well-to-do people. For those in rented accommodation, major factors were cost and insecurity in terms of tenancies. The third thing that came out very strongly, without prompting once people mentioned housing, was the idea that they were being denied the ability to build some financial security if they could not get onto the housing ladder.

We tried not to prompt people with very specific questions about pensions or insurance, until it seemed the right stage in the interview to do so, because we really wanted to understand what people saw as the things that were important to their financial well-being. Older people often talk about the risk to others rather than to themselves, and that is often because they would self-describe as being “sort of okay.” We were interested in the extent to which what we heard was influenced by current events.

If we were doing it now, what would have come out of the interviews? Rising food and energy costs? They were on the horizon at the time, but not yet hitting people financially. No or very low pay growth? That is certainly not what people told us at the time. Lack of savings is a well-researched issue in the UK. I think we compare poorly with other European nations in terms of savings, especially pension savings. That, because of that lack of resilience in the face of increased living costs, is now a big topic in the media. None of these issues were mentioned when conducting this research. Rising interest and mortgage rates were a thought rather than an experience at the time.

One surprise was that long waiting times for the NHS were not a major concern for most people. With the current public sector strikes, this is very much in people’s faces, but it was still an issue in the media at the time of the research. The other really interesting thing was social care costs. These were a big issue of debate around the time and I did expect some older people to raise it without prompting, but nobody did. When prompted on the matter, we saw some pessimistic fait accompli responses along the lines of “there is no insurance scheme to help so we just have to manage.”

One of the interesting things about housing was the lack of understanding of the risks associated with home ownership. Universally, people considered securing a mortgage and owning a home as a route to security and as a legacy for their children. Only one participant, an expert on the subject, pointed out that the housing benefits system covers some or all of one’s rent on losing a job or becoming unable to earn an income. Conversely, the State has substantially reduced the help available to people who can no longer afford to pay their mortgage, and that is a really big shift that is not well understood. Only one person raised the risk of home ownership; someone with health issues who was concerned about her ability to insure against the risk of being severely compromised. Otherwise, people universally perceived home ownership as being the route to a more secure future and a way of reducing financial risk. That “common sense” understanding may, for some people, need challenging.

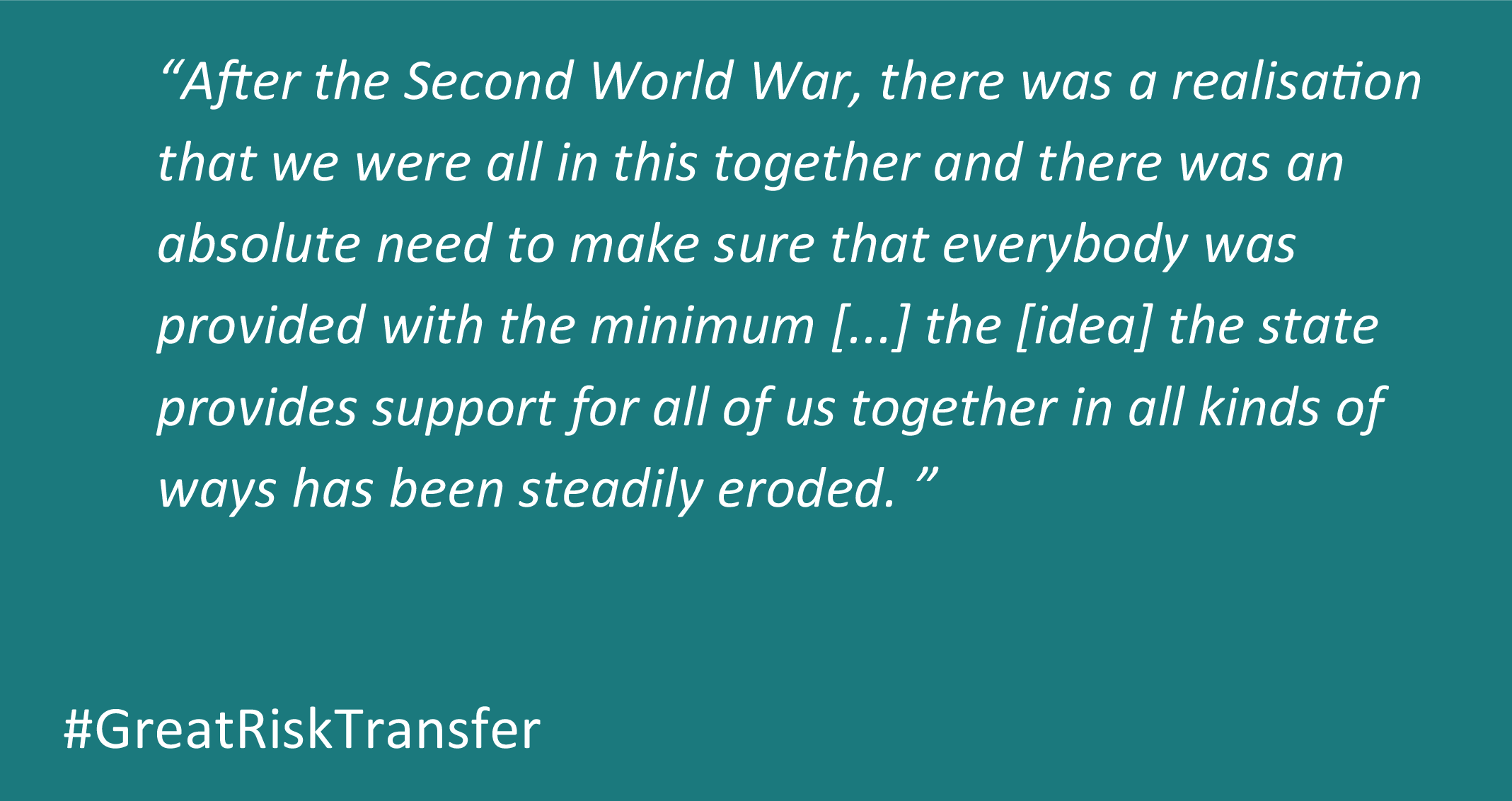

Unsurprisingly, it was only the over-60s who, unprompted, identified the shift in the social contract in the transfer of risk from institutions to individuals. The quote in Figure 1 gives one example of this:

Figure 1. Quote from respondent on the shift in the social contract.

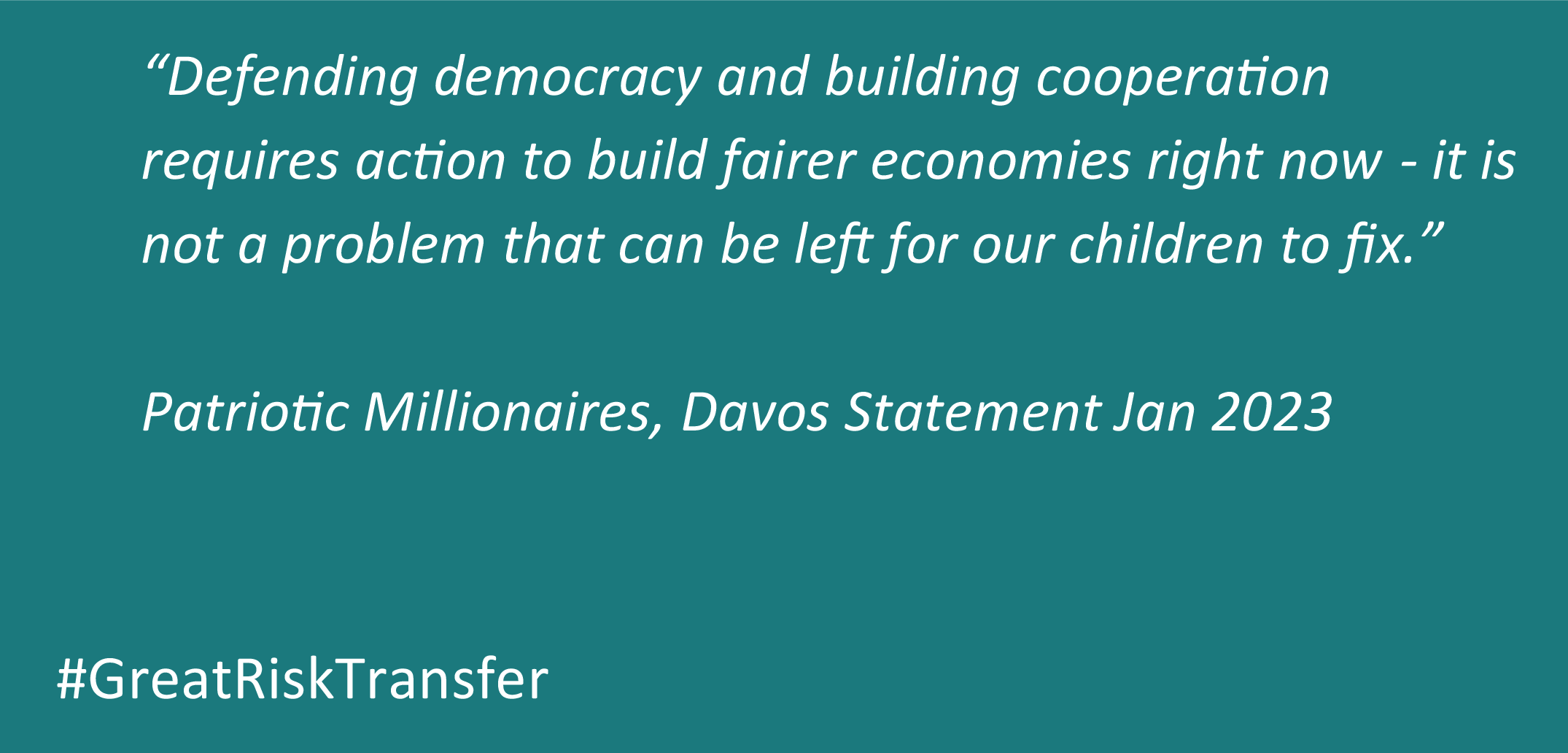

This is not just a concern for those most exposed to financial risk. In the news this week there have been reports on the self-styled ultra-rich who have banded together under the headline of being patriotic millionaires, suggesting that the ultra-wealthy should be taxed at higher rates to tackle what they called extreme inequality.

If we were to act on the IFoA’s recommendations about shifting this balance of risk and responsibility, who would we be doing it for? The report cites the public benefit but is that the key point? Is it in support of social justice by tackling inequalities? Is it to avoid creating a new generation of poor pensioners? Do we care about public spending? Do we care about supporting the industries that are dependent on us investing in our pensions or savings? Are we looking for something that is good for all of these reasons?

Figure 2 has a quote from the Patriotic Millionaires.

Figure 2. Patriotic Millionaires, Davos statement January 2023.

That notion of intergenerational fairness is interesting. Younger participants exhibited a fairly gloomy take on their futures, whilst still seeing home ownership as both de-risking their own financial futures and that of their children. For a 25 to 35-year-old, the typical age at which they will receive an inheritance is 61, which is not conducive to getting them on the housing ladder. It might pay off the rest of an existing mortgage. Those in the UK born after the 1980s might inherit an average of £200,000–£400,000, which does not go too far these days. This challenges the notion that there is a super-privileged group of people who are going to get an inheritance, and you can help your own children by getting on the housing ladder yourself.

We discovered very low levels of knowledge of what the financial risks of owning a home might be, and gaps in people’s understanding of how much risk they bear feel like a challenge that needs to be overcome.

In terms of work, the notion that changing jobs creates a new risk in life did not seem to register, nor did the threat to current job status from being made redundant or being redeployed. This is despite the fact that I spoke to several people who were in new jobs, who had recently changed jobs or were graduates who had just got their first job.

Insurance was rarely mentioned without prompting. The IFoA’s report recommended that, for people on very low incomes, there should be a minimum standard of insurance coverage. People spoke about insurance being unaffordable and, when prompted, about just covering essential possessions. In the population survey, there was a sense that you could get by without insurance, revealing a lack of appreciation for the cost of replacing goods that were damaged or stolen. Such comments came mainly from younger people.

There is a complete lack of awareness of the issue raised by the IFoA that risk profiles in insurance are increasingly priced based on the risk profiles of individuals as opposed to groups. There is an asymmetry of information, as the insurance industry has a huge amount of knowledge, but the people for whom that knowledge could be useful do not possess it.

Concern about being unable to afford basic household bills outstripped concern about the affordability of insurance for important possessions by at least 2-to-1 in every age group. I can imagine that the concern might have grown since then.

What might people have said if they better understood some of the risks they face, or if they had better knowledge of the extent to which the balance of risk has shifted towards individual responsibility? If they understood, would they want or feel able to do something? We were not able to explore that, but it is a really interesting question.

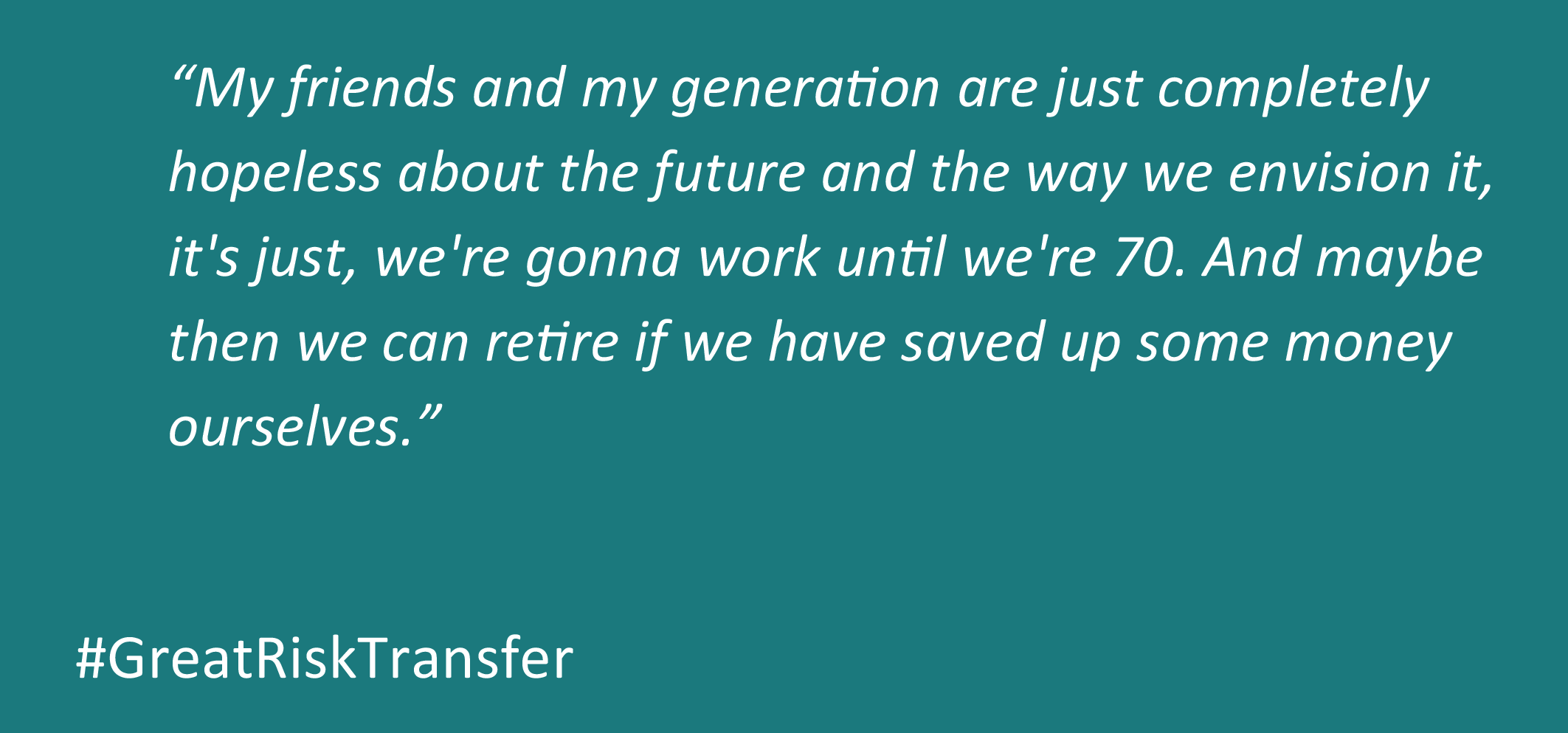

If you want to look at peak pessimism and hopelessness, speak to a young person who has thought about their future in the way that the person in Figure 3 had.

Figure 3. Quote from respondent about feeling hopeless about the future.

That sense of being outside of a system that will support them, and that maybe things will get worse rather than better, was front of mind for some people. This person was in their 30s, but not the youngest we spoke to.

It is common to view old age as being in the distant future and not consider it to be a current concern. However, the rapid increase in State pension age, especially for women, has created a sense that the rug can be pulled out from under us at any point, and that what we have been paying for we might not eventually get. That feeling of instability and lack of trust was apparent.

Plenty of research shows that people are not clear on the choices they need to make on their pension, such as how to invest, and when and how to access it. Only 45% of people were aware that they had to make any choices. That does not address whether they are confident about what choices to make, so there is a substantial lack of knowledge. One of the key recommendations in the IFoA’s report is the decumulation pathway to help address these issues.

There is a big class, or income, differential. In the ABC1 group, 50% of people were aware of choices. They did not necessarily know what to do, but they were aware that there were choices available to manage and access pension savings. Only 37% of C2DE, which would typically be lower earners, were aware of choices. That is quite a big difference.

Age is also a big difference. In the 16-to-34 age group, 31% of people were aware of the importance of managing the financial risk of pensions. The percentage rises to 60% in the 55-to-64 age range. The government has been telling people that the earlier you start saving the better, yet this does not seem salient to 16-to-34-year-olds. They are thinking about other things. That is where the notion of accumulated risk is important. If you are struggling to keep a roof over your head, are you going to be thinking about what might happen when you are 65 or 70?

The person quoted in Figure 3 went on to say that they are not even sure that they will get a pension at 70 because the rules change all the time.

It was very telling that, when it came to talking about pensions, there was a real lack of confidence that they could predict what the future might hold. We did not ask people if that made them less likely to save into their pensions. Other research has asked those kinds of questions and I think that it would be interesting to follow up and find out if there is a relationship between those two views, because it seems to me that there would be.

In our population-level survey, 52% of people said the government should be entirely responsible for ensuring that everybody has a decent standard of living in retirement. I do not know how people thought that was going to happen, given the debate around the affordability of pensions. This did not come up in the one-to-one interviews, and the strength of this feeling surprised me, especially given the fact that younger people weren’t really noticing some of the risks that they face, or even noticing there had been a shift in risks from institutions to individuals. When we conducted the interviews, people were not expecting very much, but this casts that outcome in a slightly different light. There is a sense that people still think that we are all in it together, and the government needs to do something about that.

This area of trust and of cognitive load is an important point. Cognitive load is a term used to talk about what is on your mind, the impact of having a lot on your mind and how well you function in daily life. I think that is very important when you are thinking about the public benefit of shifting the transfer of risk. Stressed people are not necessarily the most productive, and productivity at work is a big issue for our economy. We also know that stress can impact a person’s health, either in the short- or the long-term. That has a cost to society, and so we do not want to increase stress levels in the population. Therefore, the fact that people are becoming stressed by their finances does matter.

If you are shifting risk to individuals and expecting them to respond appropriately, you are putting a mental load on them. Policymakers should be wary of imposing cognitive taxes on the poor, just as they avoid monetary taxes on the poor. Filling out long forms, preparing for a lengthy interview, deciphering new rules or responding to complex incentives, all consume cognitive resources. Policymakers rarely recognise these cognitive taxes, yet our results suggest they should focus on reducing them.

Think about the things mentioned previously: the complexities of working out how to manage your pension; the challenge of working out if you are better off buying your own home; and the options that you might have. I do not think anyone is suggesting that we take those away from people, but if the burden of working it all out falls on individuals, there is a price to pay for that. For some people, this could cause enough stress to impact their quality of life.

We did our Great Risk Transfer population-level survey in May 2022. That survey went out before the peak of the issues that we are experiencing now in January 2023 as a result of the cost-of-living crisis. Concerns around not being able to afford basic household bills, such as food and energy, outstripped concerns about affordability of insurance by at least 2-to-1 in every age group. However, we also run a quarterly survey called Understanding Scotland. In our latest quarterly update, we found that nearly a quarter of Scots have lost sleep due to stress or anxiety relating to financial issues, and that rises to 35% in the 35-to-44 age group. We can only speculate as to why that is, but that would be peak age group for having children to support. I imagine that you could find similar results at the UK level. We know that the stress people are experiencing, their cognitive load, is high already. Rolling back the balance of risk might help.

In total, 36% of people said that they don’t know whose financial advice or guidance they can trust. Only those who could seriously contemplate advice cited affordability as an issue. People who perhaps did not appreciate the difference between financial advice and guidance never considered paying for advice and are more likely to say “I don’t know who I can trust.” A total of 34% of people said that it was the cost of financial advice or guidance that prevented them from seeking it out. A lot of guidance is free, but cost is something that people associate with guidance and advice.

The other stand-out result is that 52% of people in our survey are avoiding thinking about long-term financial well-being, because of more immediate financial challenges. If people are not thinking about it, they can either act inappropriately or take no action.

People trust names they have heard of. Martin Lewis was front of mind, but Citizens Advice came out strongly as well. There were low levels of trust in advice or guidance provided by an organisation that had a product to sell. In the original IFoA report, there were several references to previous mis-selling scandals. That was in the population-level survey, but it also came out unprompted in a minority of the interviews.

Interestingly, there was not a very high level of trust in government sources of information, either from the UK or Scottish Government. It indicated that people do not know who has their best interests at heart when it comes to their financial well-being. People preferred to take advice from friends and family. They noted that they might trust the person but wouldn’t know whether to trust their advice.

There is a serious democratic deficit if people are not thinking about these issues and are not very knowledgeable about them. Every time an idea is suggested, whether it is the pensions dashboard, a shift to increase take-up or approving collectively defined contribution schemes, most governments run some sort of consultation process. An informed electorate would say what they thought but there is a risk that only the experts would speak up.

We made a number of recommendations. One is that people need to talk to each other more about the things they don’t understand because we won’t deal with that democratic deficit unless we are honest about it.

We felt that the myth of choice needs to be exposed. For example, there is a plethora of choices in terms of where I might switch my defined contribution pension fund, but I do not have much choice in the type of pension scheme.

We thought that, coming back to the idea of cognitive load, avoiding financial risk compounding was important. If people are overburdened in one area, such as housing insecurity, they are probably not going to pay much attention to the other risks to their financial well-being.

Our simple recommendation was to invest in trusted, quality advisers, such as Citizen’s Advice.

The IFoA report has specific recommendations on the pensions dashboard. In our view, we need something that is more universal and rises above individual corporate entities, to increase trust and avoid the feeling that information is being provided because the company has something to sell.

Another IFoA recommendation is affordable basic insurance. How to achieve this is not entirely clear, but it seems clear that if people are locked out of the insurance market, that leads to situations where they could be without a home and possessions. Why don’t we nip those problems in the bud for those people who struggle, noting that “affordable” does not mean “free”?

There is another recommendation in the main report about learning from Flood Re. I bought an Edwardian terraced house, two fields away from the Thames, in 1992. By 2001, the flood level was at the bottom of my garden. Flood Re would not cover some newer houses like that (i.e., houses built in a place where estimated/predicted flood levels have changed since the house was built).

Secure and affordable housing is clearly a big issue. When people do not feel secure in their homes, it seems unlikely that they are going to be thinking about savings and investments. We are in the transition between a generation that could feel secure in their homes, and a generation that perhaps never can. We do not yet know what impact that might have on people’s financial provision for the future.

The IFoA report supports collectively defined contribution pensions as an alternative to defined contribution, which could bring the balance away from individuals a bit more.

In Scotland, we have the Fair Work agenda, which covers a number of things that a good employer would do. Perhaps the provision for pensions should be included, beyond auto enrolment. The concern around auto enrolment is that, once someone thinks they are contributing to a pension, they are going to be okay, but contribution levels are frequently inadequate to provide the desired level of security in older age.

Now we move to the question-and-answer session.

Mr J. Taylor, F.I.A.: I want to congratulate the David Hume Institute on taking forward the Great Risk Transfer. You have done remarkable work in bringing to life what it means for individuals. A political economist attributed the pivot point to the political ideology of the 1980s, abetted by more onerous regulation that made it much more expensive for employers to offer Defined Benefit (DB) schemes and for insurers to provide guarantees. The actuarial profession has helped to enable financial institutions with this transfer.

The profession’s public interest obligation should surely be about helping individual consumers to manage their risks better. Products involving risk-sharing mechanisms may well be the answer. Part of the issue, as Shelagh (Young) was saying, is that individuals often do not understand the risk. Simply developing a better product is not the answer, you have to be able to communicate why it is superior to create changes in behaviour.

Ms Murray: John (Taylor)'s comments are spot on. The IFoA’s publication has started the conversation and we have spread it out to a wider audience, but there is much more to do and to discuss.

Moderator: For those people who work in the general or life insurance industry, do you think that the companies you work for will enable you to develop risk-sharing products, or will the cultures within these workplaces restrict that kind of innovation?

Mr Taylor: I have two follow up questions. I was interested to know if there were any comments made about employers and the level of trust individuals placed in employers in terms of giving them advice or support. The second question was whether, through all of your interviews, anyone saw the positives in the transfer of risk over to them and in their level of choice and influence?

Ms Young: Nobody mentioned employers as a source of information, but lots of people talked about something more general, which might include employers. They talked about “age and stage” of appropriate education. A lot of younger people said they did not learn about any of this at school, but wished they had. Some also said that, once they got to university, they saw things differently. Within the Scottish Curriculum for Excellence, there may be some potential for schools to cover some of these areas, whether it is financial products or understanding compound interest, for example. People were very clear that, at each stage of your life, you look at things a bit differently, particularly when you are young and you are still rapidly developing. People needed a reminder or some guidance. They felt it was a “sink or swim” approach, and that age and stage-appropriate guidance was absent. For those people where it seemed appropriate, I did say “Well what about at work”? That caused pretty much a constipated silence as if work would not be the place where you would expect to get such guidance.

That is another societal shift. My mum used to tell me to get a job at Marks & Spencer because they looked after your dental treatment and had an in-house hairdresser. That notion of the paternalistic employer has come back rapidly over the last year. We hear of employers providing food because they are worried about their employees not being able to eat well enough. Younger people that I spoke to did not see their employers as occupying that role in their lives. That does not mean to say they would not have trusted them, because we did not ask that question. That is an open area of interest.

On your second question, whether anyone saw the positives in the transfer of risk, I think it was very hard to get a sense of that. We were talking about something that was the piece of the iceberg they could not even see. So they did not say, “Well I find that really difficult, but on the other hand at least I get to choose,” because they were not understanding it a lot of the time. Some older people, and from memory it was older, slightly wealthier people, did reference choice as being a good thing, but that seems slightly outweighed by those people who had fallen on the wrong side of luck.

There was one older woman who had been forced to take out an annuity just before the choices opened up on pension drawdown and so forth. She now thought that an annuity was not a good option for her, but even she did not think that choice was necessarily a good thing as she would be out of her depth. We did not encounter much positivity. People were tending to say that, as soon as they had a choice, it felt like it was a bad one. In the population-level survey, we did ask questions that allowed for a more positive response. It was not universally negative, but there was not a lot of buoyant positivity about this notion of opening up choice. The phrase “pension freedoms” is well known, but nobody said they feel free as a bird when it comes to sorting out their pension.

Ms Murray: We did follow up with everyone who took part in the in-depth interviews 6 months later. We wanted to know if taking part in the research had changed anything in their lives, because we are interested in action, not just in government or industry action. We wanted to see if talking about risk changes behaviour. Of the people who responded, it was pretty high, maybe 40% or 50% had done something as a direct result of taking part in the research. They did not tell us in detail what those actions were, but I thought that the fact that they had done something was incredible.

Ms Young: The comment most often made when I was winding up the face-to-face interviews was “That’s really made me think,” so I suppose that’s positive in itself.

Ms E. Kerr: On the topic of education, I think that the resounding point in the talk was that people, especially around my age, just don’t have education on these topics, and do not really seem to have the motivation to educate themselves. Putting things on the curriculum would help upcoming generations, but what can be done for people in their 20s already? I agree that with the opt-in scheme for workplace pensions, people think, “Okay well that’s fine.” Do we think that there should be some regulatory requirement for employers to properly discuss the workplace pension, and its limitations, with employees? I think that a lot of people have multiple pensions and they do not know how to find out where they are, who they are with or how to consolidate them. How can you engage people who are already out of education?

Ms Young: My son is 30 and said, “I’ve just realised I’ve got two old pensions, what shall I do with them”? And I thought, “Oh no, he’s asking friends and family.” At such a young age he has already lost track of a few little pension pots. We talk about those things in our household because we are people with some relevant resources, and yet he still has no clue. He had lots of advice at university about managing his financial affairs but nobody talked about the longer term. When I had my Pension Wise appointment, some of what we discussed I probably should have thought about when I was 25, not 55. I do think something is needed for younger people to help that lifelong understanding.

Moderator: The pensions dashboard is coming in 2025, and the intention is to create a one-stop shop for everybody to see where all of their pensions are.

Ms Murray: On that last question, I am really interested in the other research that we do with parents. If you are a very stressed parent who’s losing sleep over your finances, you are unlikely to be worrying about teaching your children about financial sustainability and pensions. About a third of the population in Scotland is under high financial stress. That is a huge number of families affected, and if you are getting your financial education from your parents, a third of young people are going to be affected. I also want to reflect on how difficult it can be to teach children about saving. When I was young, I had a post office savings book. Going in, handing over my pocket money, seeing the money going up and getting the interest paid made a difference. When I took my kids to the bank, they said it was all online now and they wouldn’t have that physical book. I tried showing them on the screen and it just didn’t work. There was only one children’s account that I could get with the physical book, but as soon as we had that, they learned how to save. I know the physical book costs providers money, but it has made so much long-term difference.

Mr P. C. Hardingham, F.I.A.: Did you discover whether actuaries are trusted by the public? Would it be helpful if actuaries get behind this? Secondly, housing was seen as a way of managing long-term risk. I am aware that this is not a traditional area for actuaries, other than maybe equity release, but is this a means for the profession to help people manage long-term risk?

Ms Young: I can’t answer your second question as it is not a topic we explored. On your first question, introducing the term “actuary” seemed inappropriate, when the concept of risk was already challenging enough for people. Expert advice was not something that people wanted though, the fear being that such advice was embedded in companies trying to sell you something. So, if there is a role for actuaries, it would have to be disentangled from the company doing the selling.

Ms Murray: Unless you come across an actuary, you probably do not know they exist.

Mr J. A. Moreland, F.I.A.: The two points that stood out to me were the first part about the evolution of the social contract from the Second World War, and the statistic of broadly 50% of people saying that the government should be responsible for providing a minimum standard of living in retirement. Given the nature of the tax system in the UK, we are saying that current and future taxpayers should be responsible for providing health care and a state pension in older age. In your study, how much awareness did you see of that? Do people recognise that this social contract is really an intergenerational social contract, and did you see a mindset of “I’ve paid for this all my life, therefore I should get X,” or “I’ve paid for those who go before me, and those that come after me should pay for me”? That then leads to the issue of how much awareness there is of the demographic changes in the UK and the risks that these present.

Ms Young: I cannot answer all of those points because our research did not cover them all. Older people clearly thought they were lucky, but on probing, they were talking about having been born at a particular time. For example, house prices came up, and the NHS in the past was very different to how it is now, for many reasons, including the fact that available treatments have expanded so much. There was a sense that things had changed and therefore perhaps the social contract had to change. There wasn’t a consistent view that it was better before and we just have to return to that. That point you made about “I have paid for this and I should get it” didn’t emerge very strongly in the research. There was a good understanding, especially among older people, that current taxpayers are funding pensions now, and that fuelled concerns about intergenerational unfairness. They were not necessarily taking a view that tax was too high but were recognising the pressures on younger people. Older people acknowledged that housing is a bigger percentage of a person’s income now than it was when they were young.

There was intergenerational understanding and there was concern about fairness. With younger people, there was a sense of doomy hopelessness, which may be because they understood that the population is aging. We did not push on people’s general understanding of demographics, as it was out of scope. There were one or two people who took the view that affordability of pensions for an aging population was an issue. With those people, we did push to make sure they understood how today’s pensions were funded to understand what lies behind their comments.

Mr S. Drewchy: I was struck by your comments about the pessimism amongst the younger interviewees. Did you find much resentment towards the older generation or a feeling that they were monopolising all of these resources?

Ms Young: No, although I had expected that because it has been in the media. Some older people did say that it was unfair and it was right that they resent us, but actually, that is not what came across. It felt like this idea of individual responsibility had really been accepted by younger people. They just thought that they had to make the best of it. They would use quite pessimistic terms like “It’s difficult,” “It’s challenging” and “I can’t see when things will get better,” but there was not a sense of older people being responsible. I think that most of the younger people we spoke to had received help from their parents, or sometimes their grandparents, in one way or another. They had a lot to be grateful for in terms of the help they had received, even if that was just advice rather than financial help. So, no, I didn’t pick up on that.

Moderator: Excellent, thank you very much. I will wrap it up there. Shelagh (Young), and Susan (Murray), thank you very much for your discussion this evening and thank you to the audience for participating.

This is an Open Access article, distributed under the terms of the Creative Commons Attribution licence (https://creativecommons.org/licenses/by/4.0/), which permits unrestricted re-use, distribution, and reproduction in any medium, provided the original work is properly cited.

This is an Open Access article, distributed under the terms of the Creative Commons Attribution licence (https://creativecommons.org/licenses/by/4.0/), which permits unrestricted re-use, distribution, and reproduction in any medium, provided the original work is properly cited.

You have

Access

You have

Access

Open access

Open access

This discussion relates to the paper presented by Shelagh Young and Susan Murray at the IFoA sessional event held on 23 January 2023.

The Moderator (Mr N. Chadha, F.I.A.): I am Nick Chadha, a member of the Institute and Faculty of Actuaries (IFoA)’s Scottish Board.

At the start of 2020, the IFoA launched its campaign on “the Great Risk Transfer.” The IFoA explored the trend of the transfer of risks, from institutions such as employers, the State and financial services providers, to individuals.

The key goals of the campaign were:

To gather and share evidence about the Great Risk Transfer and its impact across society.

To bring stakeholders together to debate the evidence and potential actions that can be taken to address the trend.

To propose recommendations for action and to work with stakeholders, including government and regulators, to drive actions that will have a positive impact on the public interest.

The IFoA published their interim findings report in July 2020, and their final findings report in April 2021. The cumulation of the IFoA’s work resulted in two key policy recommendations. Firstly, there needs to be a rebalancing of risks. In particular, it is believed that there are opportunities to ease the burden for consumers by shifting the prime responsibility for certain risks back towards institutions. The mechanism for achieving this is structural changes to markets, products and services and the legal and regulatory frameworks that shape them. Secondly, consumers need help so that they can manage their financial risk through good decision-making. A key driver for new products and services should be to help consumers with the complex decisions involved in managing financial risks effectively and affordably. This could dramatically improve outcomes for many people and for society as a whole.

In the summer of 2021, the Scottish Board was approached by the David Hume Institute (DHI). The DHI was very interested in the Great Risk Transfer and wanted to delve into the analysis further. Building on the four important areas of risk transfer – pensions, work, health, and insurance – the DHI wanted to complete a research project to find out more about relevant perceptions of risk in the Scottish population, and how people respond to risks that can affect their financial well-being.

Shelagh Young and Susan Murray are the speakers for tonight. Shelagh is the engagement lead for the David Hume Institute. Shelagh is an experienced leader, writer and facilitator in the not-for-profit and cooperative sector. Her focus at the DHI is on ensuring their work is informed by the widest possible range of people. Shelagh moved from journalism to in-house communications, joining Oxfam GB before moving to Scotland to focus on leadership development with disabled people and their families. She was chair of the UK’s only cooperative telecoms provider, the Phone Co-op, and a Founding Director of the sustainable food and farming organisation, Nourish Scotland.

Susan (Murray) joined the Institute as a Director in November 2019. She is committed to diversity of thought and was a founding trustee of the Institute of Chartered Accountants of Scotland (ICAS) Foundation, which aims to increase the diversity of young people entering the financial profession. Susan is a core social leadership fellow and has studied at the University of Edinburgh, Goldsmiths (University of London), and Aberdeen Business School. She is a member of the Institute of Directors as well as the charity Changing the Chemistry.

Ms S. Young: This research took place from early to late spring in 2022. It is interesting to speculate what the findings would be if we were talking to people now, given that conditions have materially changed in the interim. For example, the Joseph Rowntree Foundation issued a report this week reminding us that 2.4 million mortgagees are now living in poverty, judged by official measures. They think that, by the end of this year, if the mortgage rate is around 5.5%, another 400,000 people will be added to that total. This is an example of the types of risks in people’s everyday lives that I think have really shifted since we did this fieldwork.

The IFoA’s fieldwork had focused primarily on professionals. We wanted to talk to ordinary people and see what they thought about the balance of risk in their lives. We spoke to nearly 50 people face-to-face using a semi-structured interview, and we also did a population-level survey. When I make comments about what people told us, I will make the distinction between prompted and unprompted responses because we started off by asking very open questions. We did some initial scoping work, as it was very hard to get people to engage with the subject of risk. We had to simplify our approach to make it easier for people to understand what we were trying to get them to think about.

As Nick (Chadha) said, the IFoA’s report was talking about the transfer of risk from employers, the State and other institutions, and it stated that this is a significant but little-understood challenge. We wanted to see if we could understand how ordinary people perceived this. A number of factors driving this shift were identified in the original report. Among those mentioned were increased longevity, advances in technology, low-interest rates and changes in financial regulation.

The IFoA also mentioned that levels of numeracy, financial literacy and understanding of risk are generally low. There is a great deal of research that shows how people struggle with these things, and that is a really important factor to bear in mind when we come to some of our findings.

Our first question to people, either in groups or one-to-one, was very open. We asked what they understood to be the main long-term risks to their financial well-being. Well-being, money and finance all had resonance with people. It was difficult for people to grasp what we were interested in when we asked about risk without those ideas.

In the IFoA’s report, key areas were pensions, work, health and insurance. There were other items, but these were the key areas mentioned. When we spoke to people, housing came out really strongly. When we asked about risk, they talked about their housing situation. Pensions also featured prominently, as well as health to a slightly lesser extent. Work and insurance were not front of mind for people. We spoke to people who were securely ensconced in homes where the mortgage had long been paid off, so some older, wealthier people, and we also spoke to people living in rented accommodation. The interesting thing about those older people was their concern for others, such as members of the younger generation in their own family, and their ability to achieve some form of financial security through housing, which was seen as becoming out of reach for even quite well-to-do people. For those in rented accommodation, major factors were cost and insecurity in terms of tenancies. The third thing that came out very strongly, without prompting once people mentioned housing, was the idea that they were being denied the ability to build some financial security if they could not get onto the housing ladder.

We tried not to prompt people with very specific questions about pensions or insurance, until it seemed the right stage in the interview to do so, because we really wanted to understand what people saw as the things that were important to their financial well-being. Older people often talk about the risk to others rather than to themselves, and that is often because they would self-describe as being “sort of okay.” We were interested in the extent to which what we heard was influenced by current events.

If we were doing it now, what would have come out of the interviews? Rising food and energy costs? They were on the horizon at the time, but not yet hitting people financially. No or very low pay growth? That is certainly not what people told us at the time. Lack of savings is a well-researched issue in the UK. I think we compare poorly with other European nations in terms of savings, especially pension savings. That, because of that lack of resilience in the face of increased living costs, is now a big topic in the media. None of these issues were mentioned when conducting this research. Rising interest and mortgage rates were a thought rather than an experience at the time.

One surprise was that long waiting times for the NHS were not a major concern for most people. With the current public sector strikes, this is very much in people’s faces, but it was still an issue in the media at the time of the research. The other really interesting thing was social care costs. These were a big issue of debate around the time and I did expect some older people to raise it without prompting, but nobody did. When prompted on the matter, we saw some pessimistic fait accompli responses along the lines of “there is no insurance scheme to help so we just have to manage.”

One of the interesting things about housing was the lack of understanding of the risks associated with home ownership. Universally, people considered securing a mortgage and owning a home as a route to security and as a legacy for their children. Only one participant, an expert on the subject, pointed out that the housing benefits system covers some or all of one’s rent on losing a job or becoming unable to earn an income. Conversely, the State has substantially reduced the help available to people who can no longer afford to pay their mortgage, and that is a really big shift that is not well understood. Only one person raised the risk of home ownership; someone with health issues who was concerned about her ability to insure against the risk of being severely compromised. Otherwise, people universally perceived home ownership as being the route to a more secure future and a way of reducing financial risk. That “common sense” understanding may, for some people, need challenging.

Unsurprisingly, it was only the over-60s who, unprompted, identified the shift in the social contract in the transfer of risk from institutions to individuals. The quote in Figure 1 gives one example of this:

Figure 1. Quote from respondent on the shift in the social contract.

This is not just a concern for those most exposed to financial risk. In the news this week there have been reports on the self-styled ultra-rich who have banded together under the headline of being patriotic millionaires, suggesting that the ultra-wealthy should be taxed at higher rates to tackle what they called extreme inequality.

If we were to act on the IFoA’s recommendations about shifting this balance of risk and responsibility, who would we be doing it for? The report cites the public benefit but is that the key point? Is it in support of social justice by tackling inequalities? Is it to avoid creating a new generation of poor pensioners? Do we care about public spending? Do we care about supporting the industries that are dependent on us investing in our pensions or savings? Are we looking for something that is good for all of these reasons?

Figure 2 has a quote from the Patriotic Millionaires.

Figure 2. Patriotic Millionaires, Davos statement January 2023.

That notion of intergenerational fairness is interesting. Younger participants exhibited a fairly gloomy take on their futures, whilst still seeing home ownership as both de-risking their own financial futures and that of their children. For a 25 to 35-year-old, the typical age at which they will receive an inheritance is 61, which is not conducive to getting them on the housing ladder. It might pay off the rest of an existing mortgage. Those in the UK born after the 1980s might inherit an average of £200,000–£400,000, which does not go too far these days. This challenges the notion that there is a super-privileged group of people who are going to get an inheritance, and you can help your own children by getting on the housing ladder yourself.

We discovered very low levels of knowledge of what the financial risks of owning a home might be, and gaps in people’s understanding of how much risk they bear feel like a challenge that needs to be overcome.

In terms of work, the notion that changing jobs creates a new risk in life did not seem to register, nor did the threat to current job status from being made redundant or being redeployed. This is despite the fact that I spoke to several people who were in new jobs, who had recently changed jobs or were graduates who had just got their first job.

Insurance was rarely mentioned without prompting. The IFoA’s report recommended that, for people on very low incomes, there should be a minimum standard of insurance coverage. People spoke about insurance being unaffordable and, when prompted, about just covering essential possessions. In the population survey, there was a sense that you could get by without insurance, revealing a lack of appreciation for the cost of replacing goods that were damaged or stolen. Such comments came mainly from younger people.

There is a complete lack of awareness of the issue raised by the IFoA that risk profiles in insurance are increasingly priced based on the risk profiles of individuals as opposed to groups. There is an asymmetry of information, as the insurance industry has a huge amount of knowledge, but the people for whom that knowledge could be useful do not possess it.

Concern about being unable to afford basic household bills outstripped concern about the affordability of insurance for important possessions by at least 2-to-1 in every age group. I can imagine that the concern might have grown since then.

What might people have said if they better understood some of the risks they face, or if they had better knowledge of the extent to which the balance of risk has shifted towards individual responsibility? If they understood, would they want or feel able to do something? We were not able to explore that, but it is a really interesting question.

If you want to look at peak pessimism and hopelessness, speak to a young person who has thought about their future in the way that the person in Figure 3 had.

Figure 3. Quote from respondent about feeling hopeless about the future.

That sense of being outside of a system that will support them, and that maybe things will get worse rather than better, was front of mind for some people. This person was in their 30s, but not the youngest we spoke to.

It is common to view old age as being in the distant future and not consider it to be a current concern. However, the rapid increase in State pension age, especially for women, has created a sense that the rug can be pulled out from under us at any point, and that what we have been paying for we might not eventually get. That feeling of instability and lack of trust was apparent.

Plenty of research shows that people are not clear on the choices they need to make on their pension, such as how to invest, and when and how to access it. Only 45% of people were aware that they had to make any choices. That does not address whether they are confident about what choices to make, so there is a substantial lack of knowledge. One of the key recommendations in the IFoA’s report is the decumulation pathway to help address these issues.

There is a big class, or income, differential. In the ABC1 group, 50% of people were aware of choices. They did not necessarily know what to do, but they were aware that there were choices available to manage and access pension savings. Only 37% of C2DE, which would typically be lower earners, were aware of choices. That is quite a big difference.

Age is also a big difference. In the 16-to-34 age group, 31% of people were aware of the importance of managing the financial risk of pensions. The percentage rises to 60% in the 55-to-64 age range. The government has been telling people that the earlier you start saving the better, yet this does not seem salient to 16-to-34-year-olds. They are thinking about other things. That is where the notion of accumulated risk is important. If you are struggling to keep a roof over your head, are you going to be thinking about what might happen when you are 65 or 70?

The person quoted in Figure 3 went on to say that they are not even sure that they will get a pension at 70 because the rules change all the time.

It was very telling that, when it came to talking about pensions, there was a real lack of confidence that they could predict what the future might hold. We did not ask people if that made them less likely to save into their pensions. Other research has asked those kinds of questions and I think that it would be interesting to follow up and find out if there is a relationship between those two views, because it seems to me that there would be.

In our population-level survey, 52% of people said the government should be entirely responsible for ensuring that everybody has a decent standard of living in retirement. I do not know how people thought that was going to happen, given the debate around the affordability of pensions. This did not come up in the one-to-one interviews, and the strength of this feeling surprised me, especially given the fact that younger people weren’t really noticing some of the risks that they face, or even noticing there had been a shift in risks from institutions to individuals. When we conducted the interviews, people were not expecting very much, but this casts that outcome in a slightly different light. There is a sense that people still think that we are all in it together, and the government needs to do something about that.

This area of trust and of cognitive load is an important point. Cognitive load is a term used to talk about what is on your mind, the impact of having a lot on your mind and how well you function in daily life. I think that is very important when you are thinking about the public benefit of shifting the transfer of risk. Stressed people are not necessarily the most productive, and productivity at work is a big issue for our economy. We also know that stress can impact a person’s health, either in the short- or the long-term. That has a cost to society, and so we do not want to increase stress levels in the population. Therefore, the fact that people are becoming stressed by their finances does matter.

If you are shifting risk to individuals and expecting them to respond appropriately, you are putting a mental load on them. Policymakers should be wary of imposing cognitive taxes on the poor, just as they avoid monetary taxes on the poor. Filling out long forms, preparing for a lengthy interview, deciphering new rules or responding to complex incentives, all consume cognitive resources. Policymakers rarely recognise these cognitive taxes, yet our results suggest they should focus on reducing them.

Think about the things mentioned previously: the complexities of working out how to manage your pension; the challenge of working out if you are better off buying your own home; and the options that you might have. I do not think anyone is suggesting that we take those away from people, but if the burden of working it all out falls on individuals, there is a price to pay for that. For some people, this could cause enough stress to impact their quality of life.

We did our Great Risk Transfer population-level survey in May 2022. That survey went out before the peak of the issues that we are experiencing now in January 2023 as a result of the cost-of-living crisis. Concerns around not being able to afford basic household bills, such as food and energy, outstripped concerns about affordability of insurance by at least 2-to-1 in every age group. However, we also run a quarterly survey called Understanding Scotland. In our latest quarterly update, we found that nearly a quarter of Scots have lost sleep due to stress or anxiety relating to financial issues, and that rises to 35% in the 35-to-44 age group. We can only speculate as to why that is, but that would be peak age group for having children to support. I imagine that you could find similar results at the UK level. We know that the stress people are experiencing, their cognitive load, is high already. Rolling back the balance of risk might help.

In total, 36% of people said that they don’t know whose financial advice or guidance they can trust. Only those who could seriously contemplate advice cited affordability as an issue. People who perhaps did not appreciate the difference between financial advice and guidance never considered paying for advice and are more likely to say “I don’t know who I can trust.” A total of 34% of people said that it was the cost of financial advice or guidance that prevented them from seeking it out. A lot of guidance is free, but cost is something that people associate with guidance and advice.

The other stand-out result is that 52% of people in our survey are avoiding thinking about long-term financial well-being, because of more immediate financial challenges. If people are not thinking about it, they can either act inappropriately or take no action.

People trust names they have heard of. Martin Lewis was front of mind, but Citizens Advice came out strongly as well. There were low levels of trust in advice or guidance provided by an organisation that had a product to sell. In the original IFoA report, there were several references to previous mis-selling scandals. That was in the population-level survey, but it also came out unprompted in a minority of the interviews.

Interestingly, there was not a very high level of trust in government sources of information, either from the UK or Scottish Government. It indicated that people do not know who has their best interests at heart when it comes to their financial well-being. People preferred to take advice from friends and family. They noted that they might trust the person but wouldn’t know whether to trust their advice.

There is a serious democratic deficit if people are not thinking about these issues and are not very knowledgeable about them. Every time an idea is suggested, whether it is the pensions dashboard, a shift to increase take-up or approving collectively defined contribution schemes, most governments run some sort of consultation process. An informed electorate would say what they thought but there is a risk that only the experts would speak up.

We made a number of recommendations. One is that people need to talk to each other more about the things they don’t understand because we won’t deal with that democratic deficit unless we are honest about it.

We felt that the myth of choice needs to be exposed. For example, there is a plethora of choices in terms of where I might switch my defined contribution pension fund, but I do not have much choice in the type of pension scheme.

We thought that, coming back to the idea of cognitive load, avoiding financial risk compounding was important. If people are overburdened in one area, such as housing insecurity, they are probably not going to pay much attention to the other risks to their financial well-being.

Our simple recommendation was to invest in trusted, quality advisers, such as Citizen’s Advice.

The IFoA report has specific recommendations on the pensions dashboard. In our view, we need something that is more universal and rises above individual corporate entities, to increase trust and avoid the feeling that information is being provided because the company has something to sell.

Another IFoA recommendation is affordable basic insurance. How to achieve this is not entirely clear, but it seems clear that if people are locked out of the insurance market, that leads to situations where they could be without a home and possessions. Why don’t we nip those problems in the bud for those people who struggle, noting that “affordable” does not mean “free”?

There is another recommendation in the main report about learning from Flood Re. I bought an Edwardian terraced house, two fields away from the Thames, in 1992. By 2001, the flood level was at the bottom of my garden. Flood Re would not cover some newer houses like that (i.e., houses built in a place where estimated/predicted flood levels have changed since the house was built).

Secure and affordable housing is clearly a big issue. When people do not feel secure in their homes, it seems unlikely that they are going to be thinking about savings and investments. We are in the transition between a generation that could feel secure in their homes, and a generation that perhaps never can. We do not yet know what impact that might have on people’s financial provision for the future.

The IFoA report supports collectively defined contribution pensions as an alternative to defined contribution, which could bring the balance away from individuals a bit more.

In Scotland, we have the Fair Work agenda, which covers a number of things that a good employer would do. Perhaps the provision for pensions should be included, beyond auto enrolment. The concern around auto enrolment is that, once someone thinks they are contributing to a pension, they are going to be okay, but contribution levels are frequently inadequate to provide the desired level of security in older age.

Now we move to the question-and-answer session.

Mr J. Taylor, F.I.A.: I want to congratulate the David Hume Institute on taking forward the Great Risk Transfer. You have done remarkable work in bringing to life what it means for individuals. A political economist attributed the pivot point to the political ideology of the 1980s, abetted by more onerous regulation that made it much more expensive for employers to offer Defined Benefit (DB) schemes and for insurers to provide guarantees. The actuarial profession has helped to enable financial institutions with this transfer.

The profession’s public interest obligation should surely be about helping individual consumers to manage their risks better. Products involving risk-sharing mechanisms may well be the answer. Part of the issue, as Shelagh (Young) was saying, is that individuals often do not understand the risk. Simply developing a better product is not the answer, you have to be able to communicate why it is superior to create changes in behaviour.

Ms Murray: John (Taylor)'s comments are spot on. The IFoA’s publication has started the conversation and we have spread it out to a wider audience, but there is much more to do and to discuss.

Moderator: For those people who work in the general or life insurance industry, do you think that the companies you work for will enable you to develop risk-sharing products, or will the cultures within these workplaces restrict that kind of innovation?

Mr Taylor: I have two follow up questions. I was interested to know if there were any comments made about employers and the level of trust individuals placed in employers in terms of giving them advice or support. The second question was whether, through all of your interviews, anyone saw the positives in the transfer of risk over to them and in their level of choice and influence?

Ms Young: Nobody mentioned employers as a source of information, but lots of people talked about something more general, which might include employers. They talked about “age and stage” of appropriate education. A lot of younger people said they did not learn about any of this at school, but wished they had. Some also said that, once they got to university, they saw things differently. Within the Scottish Curriculum for Excellence, there may be some potential for schools to cover some of these areas, whether it is financial products or understanding compound interest, for example. People were very clear that, at each stage of your life, you look at things a bit differently, particularly when you are young and you are still rapidly developing. People needed a reminder or some guidance. They felt it was a “sink or swim” approach, and that age and stage-appropriate guidance was absent. For those people where it seemed appropriate, I did say “Well what about at work”? That caused pretty much a constipated silence as if work would not be the place where you would expect to get such guidance.

That is another societal shift. My mum used to tell me to get a job at Marks & Spencer because they looked after your dental treatment and had an in-house hairdresser. That notion of the paternalistic employer has come back rapidly over the last year. We hear of employers providing food because they are worried about their employees not being able to eat well enough. Younger people that I spoke to did not see their employers as occupying that role in their lives. That does not mean to say they would not have trusted them, because we did not ask that question. That is an open area of interest.

On your second question, whether anyone saw the positives in the transfer of risk, I think it was very hard to get a sense of that. We were talking about something that was the piece of the iceberg they could not even see. So they did not say, “Well I find that really difficult, but on the other hand at least I get to choose,” because they were not understanding it a lot of the time. Some older people, and from memory it was older, slightly wealthier people, did reference choice as being a good thing, but that seems slightly outweighed by those people who had fallen on the wrong side of luck.

There was one older woman who had been forced to take out an annuity just before the choices opened up on pension drawdown and so forth. She now thought that an annuity was not a good option for her, but even she did not think that choice was necessarily a good thing as she would be out of her depth. We did not encounter much positivity. People were tending to say that, as soon as they had a choice, it felt like it was a bad one. In the population-level survey, we did ask questions that allowed for a more positive response. It was not universally negative, but there was not a lot of buoyant positivity about this notion of opening up choice. The phrase “pension freedoms” is well known, but nobody said they feel free as a bird when it comes to sorting out their pension.

Ms Murray: We did follow up with everyone who took part in the in-depth interviews 6 months later. We wanted to know if taking part in the research had changed anything in their lives, because we are interested in action, not just in government or industry action. We wanted to see if talking about risk changes behaviour. Of the people who responded, it was pretty high, maybe 40% or 50% had done something as a direct result of taking part in the research. They did not tell us in detail what those actions were, but I thought that the fact that they had done something was incredible.

Ms Young: The comment most often made when I was winding up the face-to-face interviews was “That’s really made me think,” so I suppose that’s positive in itself.

Ms E. Kerr: On the topic of education, I think that the resounding point in the talk was that people, especially around my age, just don’t have education on these topics, and do not really seem to have the motivation to educate themselves. Putting things on the curriculum would help upcoming generations, but what can be done for people in their 20s already? I agree that with the opt-in scheme for workplace pensions, people think, “Okay well that’s fine.” Do we think that there should be some regulatory requirement for employers to properly discuss the workplace pension, and its limitations, with employees? I think that a lot of people have multiple pensions and they do not know how to find out where they are, who they are with or how to consolidate them. How can you engage people who are already out of education?

Ms Young: My son is 30 and said, “I’ve just realised I’ve got two old pensions, what shall I do with them”? And I thought, “Oh no, he’s asking friends and family.” At such a young age he has already lost track of a few little pension pots. We talk about those things in our household because we are people with some relevant resources, and yet he still has no clue. He had lots of advice at university about managing his financial affairs but nobody talked about the longer term. When I had my Pension Wise appointment, some of what we discussed I probably should have thought about when I was 25, not 55. I do think something is needed for younger people to help that lifelong understanding.

Moderator: The pensions dashboard is coming in 2025, and the intention is to create a one-stop shop for everybody to see where all of their pensions are.

Ms Murray: On that last question, I am really interested in the other research that we do with parents. If you are a very stressed parent who’s losing sleep over your finances, you are unlikely to be worrying about teaching your children about financial sustainability and pensions. About a third of the population in Scotland is under high financial stress. That is a huge number of families affected, and if you are getting your financial education from your parents, a third of young people are going to be affected. I also want to reflect on how difficult it can be to teach children about saving. When I was young, I had a post office savings book. Going in, handing over my pocket money, seeing the money going up and getting the interest paid made a difference. When I took my kids to the bank, they said it was all online now and they wouldn’t have that physical book. I tried showing them on the screen and it just didn’t work. There was only one children’s account that I could get with the physical book, but as soon as we had that, they learned how to save. I know the physical book costs providers money, but it has made so much long-term difference.

Mr P. C. Hardingham, F.I.A.: Did you discover whether actuaries are trusted by the public? Would it be helpful if actuaries get behind this? Secondly, housing was seen as a way of managing long-term risk. I am aware that this is not a traditional area for actuaries, other than maybe equity release, but is this a means for the profession to help people manage long-term risk?

Ms Young: I can’t answer your second question as it is not a topic we explored. On your first question, introducing the term “actuary” seemed inappropriate, when the concept of risk was already challenging enough for people. Expert advice was not something that people wanted though, the fear being that such advice was embedded in companies trying to sell you something. So, if there is a role for actuaries, it would have to be disentangled from the company doing the selling.

Ms Murray: Unless you come across an actuary, you probably do not know they exist.

Mr J. A. Moreland, F.I.A.: The two points that stood out to me were the first part about the evolution of the social contract from the Second World War, and the statistic of broadly 50% of people saying that the government should be responsible for providing a minimum standard of living in retirement. Given the nature of the tax system in the UK, we are saying that current and future taxpayers should be responsible for providing health care and a state pension in older age. In your study, how much awareness did you see of that? Do people recognise that this social contract is really an intergenerational social contract, and did you see a mindset of “I’ve paid for this all my life, therefore I should get X,” or “I’ve paid for those who go before me, and those that come after me should pay for me”? That then leads to the issue of how much awareness there is of the demographic changes in the UK and the risks that these present.

Ms Young: I cannot answer all of those points because our research did not cover them all. Older people clearly thought they were lucky, but on probing, they were talking about having been born at a particular time. For example, house prices came up, and the NHS in the past was very different to how it is now, for many reasons, including the fact that available treatments have expanded so much. There was a sense that things had changed and therefore perhaps the social contract had to change. There wasn’t a consistent view that it was better before and we just have to return to that. That point you made about “I have paid for this and I should get it” didn’t emerge very strongly in the research. There was a good understanding, especially among older people, that current taxpayers are funding pensions now, and that fuelled concerns about intergenerational unfairness. They were not necessarily taking a view that tax was too high but were recognising the pressures on younger people. Older people acknowledged that housing is a bigger percentage of a person’s income now than it was when they were young.

There was intergenerational understanding and there was concern about fairness. With younger people, there was a sense of doomy hopelessness, which may be because they understood that the population is aging. We did not push on people’s general understanding of demographics, as it was out of scope. There were one or two people who took the view that affordability of pensions for an aging population was an issue. With those people, we did push to make sure they understood how today’s pensions were funded to understand what lies behind their comments.

Mr S. Drewchy: I was struck by your comments about the pessimism amongst the younger interviewees. Did you find much resentment towards the older generation or a feeling that they were monopolising all of these resources?

Ms Young: No, although I had expected that because it has been in the media. Some older people did say that it was unfair and it was right that they resent us, but actually, that is not what came across. It felt like this idea of individual responsibility had really been accepted by younger people. They just thought that they had to make the best of it. They would use quite pessimistic terms like “It’s difficult,” “It’s challenging” and “I can’t see when things will get better,” but there was not a sense of older people being responsible. I think that most of the younger people we spoke to had received help from their parents, or sometimes their grandparents, in one way or another. They had a lot to be grateful for in terms of the help they had received, even if that was just advice rather than financial help. So, no, I didn’t pick up on that.

Moderator: Excellent, thank you very much. I will wrap it up there. Shelagh (Young), and Susan (Murray), thank you very much for your discussion this evening and thank you to the audience for participating.