3 Tracing ownership networks

Having explained the determinants of collective political action among firms, this chapter examines the emergence of dominant stakeholders in three transition countries, with two goals. First, it observes the historical process by which business networks were created. Second, it explores how the process in each country generated three strikingly different relationships between business networks and political actors. In Poland, the relationship was one of joint problem solving leading to the emergence of a concertation state. In Bulgaria, economic elites used their power in a barren organizational landscape to dominate state institutions and bring about a captured state. In Romania, the lack of strong networks among firms left them at the mercy of strong political actors, who held the reins of what I label the patronage state.

Privatization was an important initial part of the process of creating stakeholders. Yet in seeking to understand what might be called “post-post-socialism” – the period beyond the first phase of economic and political transformation, when markets were already in operation – this chapter goes beyond privatization policy. Ownership changes subsequent to privatization often dramatically altered the initial ownership distribution effects of privatization and promoted a different set of owners from the early stakeholders. Both these moments must be considered in order to understand the development of networks of firms, and thus the different trajectories of institutional development identified in the previous section.

Much research has been conducted on the politicization of the privatization and transformation process in the 1990s. Little is known, however, about the political bases of institution building that have emerged in post-socialist countries. After the political and economic transformations began, various patterns of interaction between political and economic stakeholders took shape that affected the trajectory of the institutional transformation begun after 1989. These patterns of interaction have not been widely explored as a causal factor in the nature of institutional development. Chapter 2 showed that banks and financial firms contribute to broader networks, while industrial and family firms tend to create narrower networks. Narrow networks reduce the likelihood of collective action, while broad networks increase it. This chapter builds on this finding to show the causal processes through which the interaction of networks of owners with political actors shaped institutional development.

The chapter proceeds as follows. The next section identifies the mechanisms by which networks of ownership affect institutional development. The following section shows how different kinds of owners emerged in each of the three country cases – Poland, Romania, and Bulgaria. It then explores the development of firm networks in each country using ownership networks data. In each country, state ownership remained quite prominent until the early 2000s. What differed was the non-state actor chosen as the key vehicle in the transition to the private economy.

I show that banks became the anchors of a network of ownership that joined the 200 largest firms in Poland. Beyond this, political actors encouraged an array of hybrid ownership forms not seen elsewhere. For example, several banks were partially privatized to foreign investors, with the state retaining important shares. These banks held shares in a multitude of firms. In turn, many firms held shares in other firms and banks, creating a web of crossing alliances.

A very different dynamic took hold in Romania. In the first decade state privatization funds remained prominent as owners until they were displaced by domestic industrial firms and individual owners. This strategy generated far less new capital, as it did not produce the financialization of the new private sector that took place in Poland. It succeeded only in attracting foreign capital well into the second decade of transition, when foreign industrial firms acquired stakes in Romanian firms. Few firms created cross-ownership ties. Private individual investors were also key figures. Moreover, the early choice of management/employee buyout as a privatization strategy left many firms isolated, without consolidated leadership, and put them at the mercy of a relatively well consolidated political elite. The resulting narrow networks provided little support for firms maneuvering in a context in which a single political party dominated much of the first two decades of transformation.

In Bulgaria, a third approach to private sector development promoted industrial firms – among which were many state-owned holding companies – and private individuals as owners. The hostile business environment in Bulgaria discouraged foreign firms from taking much of an interest, and Bulgaria remained an unattractive destination for FDI. For different reasons, the resulting network of owners was also narrow.

As I have argued throughout, these three different network structures shaped the preferences and possibilities of elites with regard to the development of fundamental market institutions. That network structure was the cause and not the result of institutional development is also clear from the process tracing carried out in this chapter. The seeds of each network structure took shape early after 1989, well before the large differences in institutional trajectory took shape.

Ownership networks as maps of politics–business relations

Ownership matters because modern states derive a considerable portion of their power from the economic assets that they control directly and indirectly, as well as the assets that they regulate. States build this power by coordinating and promoting sectors and particular groups of firms. In other words, the configuration of ownership ties among firms is a key component of the politics of economic development.

In making this argument, I follow a tradition that has recognized the impact of the configuration of accumulated assets on state capacity and regime type (Moore Reference Moore1967). For Moore, where ownership lies, how it is configured, and the participation of landed and peasant classes explain the transformation of agrarian societies into either democratic or authoritarian (fascist or communist) ones. Moore’s focus is on class conflict, but similar arguments have been used to explain the development of institutions without such a focus on class. The point is that the configuration of assets structures conflict between classes and determines the trajectory of political development.

Carruthers (Reference Carruthers1996) makes a similar point: that elite cooperation on state-building projects is often based on exchanges between elite groups. Thus, as political elites are trying to resolve state-building dilemmas by soliciting support from powerful societal interests, the latter are also seeking to resolve their own institutional dilemmas. These projects can be complementary if the different parties involved are able to make credible commitments, although that itself is a complicated problem of political innovation. Carruthers details how the Crown in seventeenth-century Britain essentially invented the possibility of state borrowing from the public in order to push forward with the project of centralizing and expanding state power. The fundamental puzzle that the Crown overcame was to find a way that the sovereign could credibly commit to the repayment of loans obtained from its subjects. Economic linkages not only solved a financial problem but also served as the glue for a broad exchange of loyalty between different social groups. This resolved a dilemma for both parties by unleashing stocks of capital for productive use in early bond markets and generating desperately needed resources for state projects. What economic actors saw as a struggle to shape the rules of the economic game, the state and its political leaders viewed as the search for extractive capacity and control (Carruthers Reference Carruthers1996).

The British Crown’s success in developing financial markets was not just a result of collaborative bargains between economic and political elites. The period is interesting because the financial revolution was taking place just as political parties were created in the British parliament. Carruthers shows that the new parties, the Whigs and Tories, used the economy for political ends and imposed a political logic on the economy that shaped institutional outcomes such as the development of competitive and efficient capital markets.1

Within these struggles, networks were deployed to offset uncertainty. Stark and Bruszt (Reference Stark and Bruszt1998), McDermott (Reference McDermott2007), and Stark and Vedres (Reference Stark and Vedres2012) have shown that early post-communist ownership reconfigurations were often geared toward achieving political ends, or attempts to recombine elements into new valuable property or to provide protection from external pressures. Network reconfigurations also served as an adjustment mechanism that helped firms cope with changing external conditions, because networks reorganize in reaction to external stimuli such as globalization or economic liberalization (Hamilton and Biggart Reference Hamilton and Biggart1988; Hall and Soskice Reference Hall and Soskice2001; Kogut and Walker Reference Kogut and Walker2001; Stark and Vedres Reference Stark and Vedres2006). These networks also provide support to firms in difficult times. In other words, networks – whether they are based on ownership, membership of boards of directors, or even friendship – are strategic assets, and ties are deployed as a part of the profit-making efforts of individual firms. Whether banks are allowed to merge with each other, and which firms are allowed or encouraged to acquire stakes in other firms, are similarly political decisions.

This chapter observes how ties of ownership between companies took form between 1990 and 2005. Decisions to configure or reconfigure the economy in a particular way and create joint links – to create ownership ties between two firms – are all reflections of the political organization of the economy (Mizruchi Reference Mizruchi1992; Davis and Mizruchi Reference Davis and Mizruchi1999; Uzzi Reference Uzzi1999). As decisions over economic policy were made in the early 1990s, banks, foreign investors, single large private owners, investment funds, holding companies, or large industrial firms began to emerge as more or less prominent stakeholders. These actors acquired different roles in each context. These early decisions, in turn, generated pressure for certain policies that favored the dominant type of stakeholder and thus reverberated through the process of institution building.

The ownership structure is one way of assessing the configuration of interests and their potential for constructive interaction (concertation). Economic transactions took place against the background of a political contest that instrumentalized firms for the sake of gaining an edge in politics. This dynamic also reproduced itself within the market, however, where competitive pressures rose in accordance with the needs of political actors. Firms also were pushed to perform in order to generate profits that were partly used to buy much-needed political capital. Said another way, when political competition was sharp, firms went from being the spoils to generating the spoils for political actors. Market institutions thus served and were shaped by political struggles. In some cases, as in Poland, these conflicts were sufficiently deadlocked to push elites toward the development of more stable rules of interaction. When elites were less balanced, as in the other two cases examined here, institutional outcomes were significantly poorer.

Ownership development in Poland, Romania, and Bulgaria

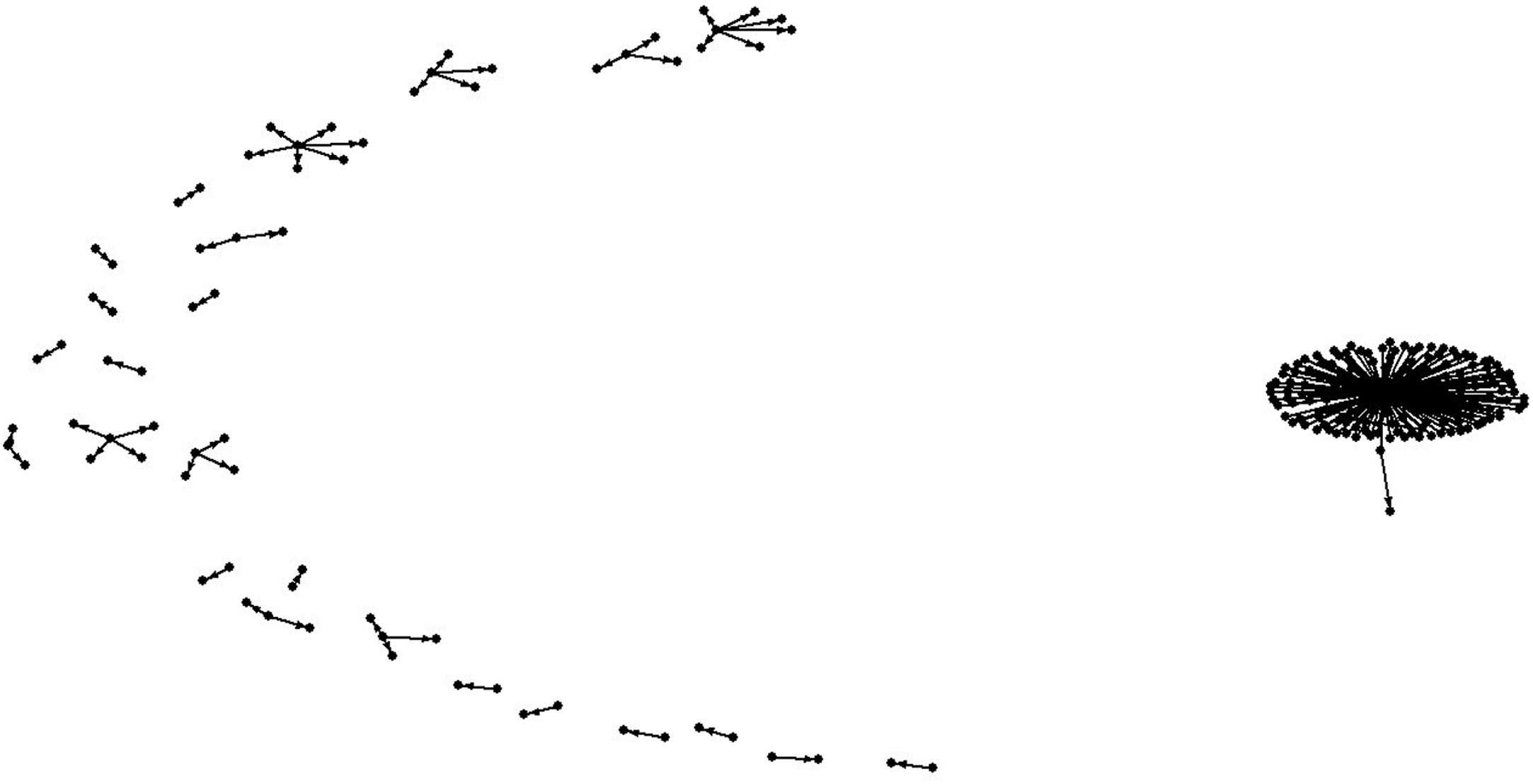

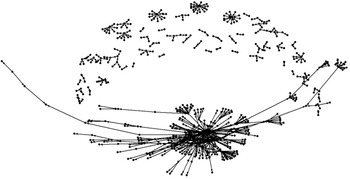

To understand the development of different state–business relationships, two types of data are considered in addition to a historical analysis of business networks: (1) data on the top owners and the number of stakes they hold in the top 200 firms (ranked by revenue); and (2) data on the characteristics of the networks among the top 200 firms themselves.

The following questions are posed with regard to the data. What types of owners have emerged in each country? How did privatization reshape firm networks? What subsequent changes restructured those networks? Are the networks between firms broad or deep? Are cross-holdings between firms common? Do they extend across business sectors? Do these networks include the state? What kinds of actors are the most central owners in the economy? Are institutional investors, banks, industrial groups, or family firms prominent?

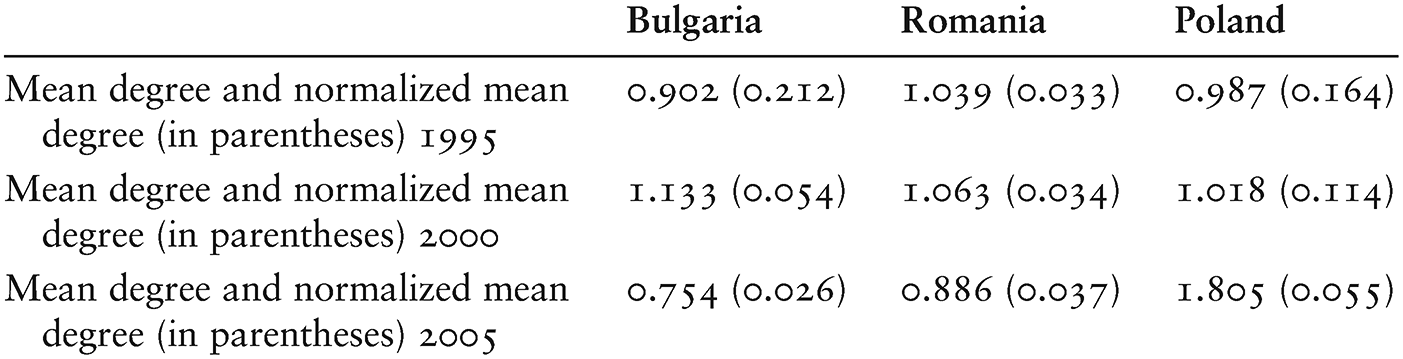

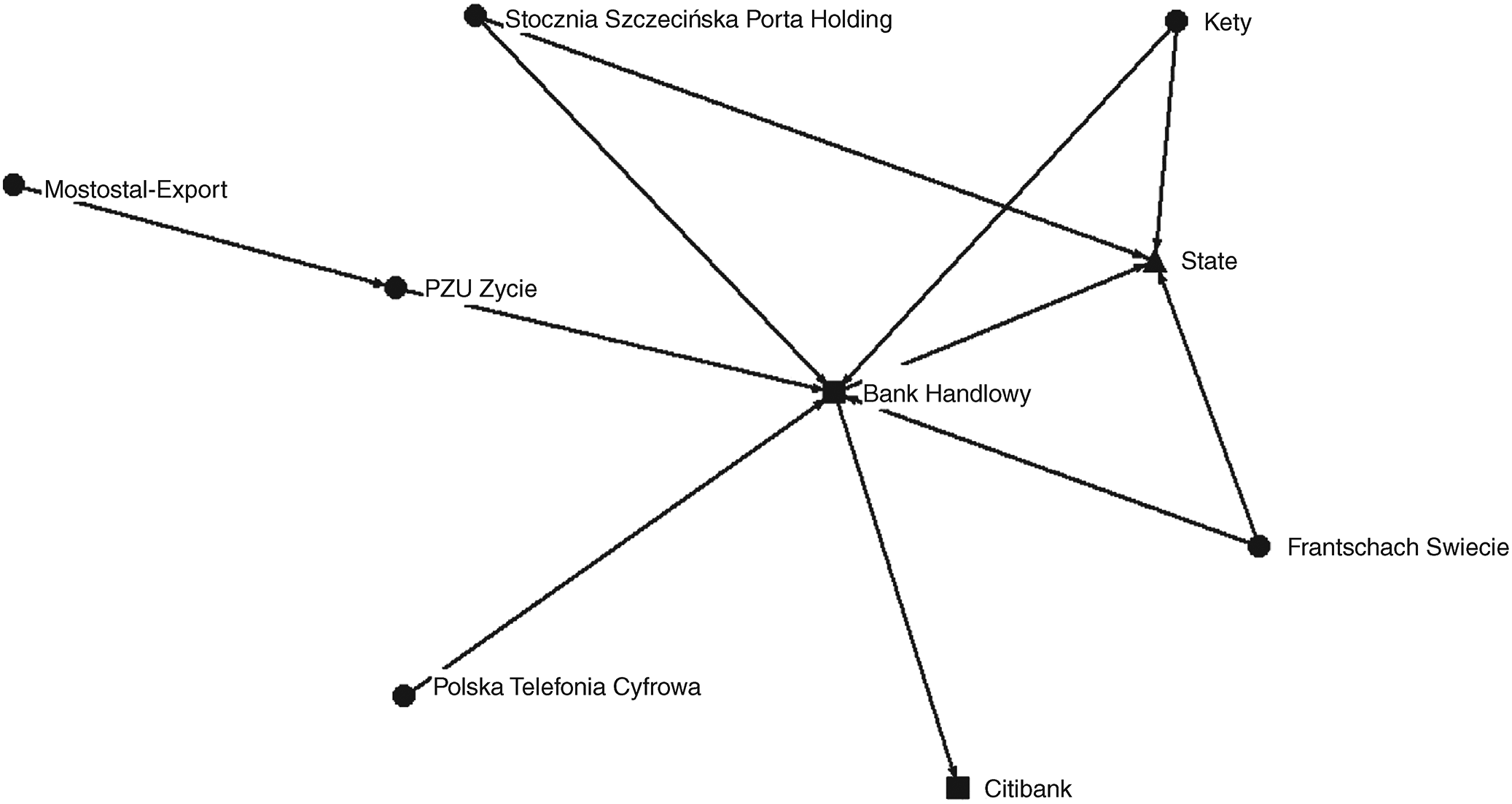

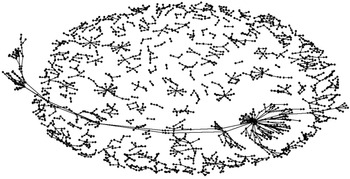

Comparing data on firm ownership networks across countries shows the starkly different paths followed by each country in the political process of creating marketized economies.2 This difference is based not only on the speed of privatization or the persistence of state ownership in particular sectors. In each country, different structural shifts took place across the economy, transferring ownership stakes from the state to different dominant types of actors. The following sections present data on the types of key owners emerging in each country. Table 3.1 shows the changes in the ownership structure of the 200 largest firms by revenue between 1995 and 2005 for each of the three largest categories (by number of ties) in any given year and country. It is compared to the status of the same owner type in the other countries to show how sharply different paths were taken. Examining the ties between the 200 largest firms by revenue and their owners captures the control structure of the powerhouses of economic activity in each country and effectively delivers a picture of the choices about restructuring that each government took. These paths were not the reflection of an unintended choice but largely conscious decisions on the part of policy makers and their allies in the economy. They reflect the dominant alliance between political and economic stakeholders.3

As the table shows, state ownership – unsurprisingly – declined between 1995 and 2005 as a result of privatization but remained a prominent feature in each country until 2000. Partial privatization was a common strategy in the transition economies and was driven by the desire to retain some political control on the part of the state, inadequate capital on the part of new investors, and the division of risk between private investors and the state (Maw Reference Maw2002). The gradual pace of privatization in transition economies was an avenue for states to signal commitment, a logical way of showing that the government was willing to retain a share of the residual risk – that is, “a signal that it does not intend to redistribute value through a future shift in policy” (Perotti Reference Perotti1995). This is particularly important to potential private stakeholders in periods of future policy uncertainty that have the potential to bring about reversals that would reduce the future value of the privatized firm. Such uncertainty could come from the possibility that the party in power could change or simply because an insufficient amount of time has passed to allow investors to gauge the government’s longer-term intentions. All these factors were present in the transition economies, and thus it is not surprising that partial privatization persisted for such a long time.

Although privatization as a broad goal was common to all transition countries, they chose different paths in addressing uncertainty. Comparing the three countries shown in Table 3.1, it is quite apparent that privatization strategies and subsequent policy decisions privileged some potential owners over others, and different types of owners emerged as the largest stakeholders in each country. As early as 1995 state-owned banks were being pushed forward as stakeholders in the Polish network of large firms. By 2000 Poland’s ownership structure was heavily influenced by foreign banks and investment funds. Strikingly, four large banks linked the state to foreign capital, while one linked the state with private domestic capital. By 2005 foreign firms were heavily in control of assets in the Polish economy. This injection of foreign capital was, at least in part, a fruit of the early strategy of placing banks in control of industrial firms as part of the process of restructuring.

Throughout the Polish transformation, financial firms were key owners. The data show that the politics of industrial restructuring privileged the shifting of ownership to state-owned banks, even when these were partially privatized to foreigners, and resisted the transfer of industrial firms to other industrial firms. Later sections of this chapter show that banks held ownership ties both to other banks and to industrial firms. The network position of banks thus made them the decision-making centers for the management of the economy and rendered them influential in the operative decisions of a wide range of nonfinancial firms. Comparison with Bulgaria and Romania shows that this financialization of the economy was a quite peculiar characteristic of the Polish approach and distinguished it from other countries, which chose mass privatization, employee participation, or the creation of industrial groups by sector as their preferred strategies. Instead, the Polish path postponed the transfer of ownership rights in a significant way even to industrial firms until quite late – between 2000 and 2005. Only in 2005 did industrial firms appear as significant stakeholders there.

By contrast, in Romania, management and employee buyouts (MEBOs) and mass privatization funds were the key emergent ownership form until 2000, when industrial companies displaced them. In place of Polish banks, Romanian private owners and family groups, representing the very prominent new economic elite, ranked highly but were not in the top three. Foreign financial firms were present in 2000, but the lack of domestic financial firms meant that the overall presence of finance as an owner was much smaller. Instead, the overwhelming characteristic of Romanian ownership networks was that of direct individual or group ownership of assets. By 2005 private individual investors were the second largest owner type in Romania. Some of these were small stakeholders, but the majority held large stakes in the top firms.

A different strategy was pursued in Bulgaria – perhaps even one that can be defined as the opposite of the Polish strategy. Instead of financializing ownership by transferring debt in exchange for equity to state-owned banks, the Bulgarian state focused on giants in each sector to conduct restructuring. The hope was that agglomerating firms in the same sector under single holding companies would make the assets easier to restructure and more attractive for privatization down the line. Hence, in Bulgaria, state-owned firms actually increased their profile as owners, reflecting this transfer of ownership from the state to state-owned holding companies that took place during the first decade of transformation. The move effected an informal decentralization of power and loss of control of state-owned assets by putting large numbers of firms under the control of holding company managers instead of subjecting each firm to ministerial supervision. Consistent with this trend, management buyouts and mass privatization dominated, together with state ownership until a later period, when individual investors began to emerge.

Consider the contrast with the Polish case. In this, an alliance of financial capital with the state slowly transformed into a union of financial and industrial capital. In Bulgaria, a decentralization of ownership stakes to state-owned firms and employee privatizations transformed into an economy governed by individual stakeholders and industrial firms. Unsurprisingly, these groups had dramatically different interests and time horizons. Polish financial firms and the links they promoted between firms led the network structure of ties to be much more horizontal. As a result, firms were locked into a web of mutual interest with other firms by debt and equity holdings. These allowed information to flow and bound firms into ongoing relationships. They also generated a distributed interest in the performance of each firm. Bulgarian firms had no such ties, and individuals in charge of both state and private property had only their immediate self-interest in view in a highly uncertain political context that offered few incentives to invest in the long term.

To give more texture to this argument that owner types and their networks influence management style, the following sections discuss in more detail the development of the network of firms in each country.

Poland’s path to privatization: banks promote broad networks

In Poland, two features were distinctive in the first period of the transformation. First, banks were a critical part of the post-1989 capitalist development, emerging at the center of clusters of firms. Banks became involved in a series of debt/equity swaps that created broad networks of cross-ownership because of a government preference for workouts. Under the workout procedure, banks could negotiate workout agreements with problem debtors and force them on creditors. This put banks in a position to focus on long-term value and the development of a broad network of firms connected by ownership ties. Second, the facilitation of debt/equity swaps was part of a distinct policy that avoided or delayed the foreign purchase of many attractive firms. This policy delayed the transition of nearly a half of all ownership shares in financial firms until after 2000 and caused the majority of shares in industrial firms to remain in domestic hands. As a result, in the second stage, private entrepreneurs found it difficult to dominate national economic – and hence political – activity. The new Polish magnates were certainly important in Polish politics, but they were as much dependent on political parties as the parties were dependent on them. When asked why his firm had such extensive ties to parties and the state, one business leader commented, “Because the political sphere is so present – in ownership transformation, in regulation. It’s like in business: in the early phase, you look for a partner with whom you can do something together.” The level of political competition raised the stakes for both sets of elites. As a result, a broad horizontal network of ownership emerged in Poland that was distinct from the other countries under comparison.

The initial step in the distribution of ownership stakes was the process of privatization. The most common methods of privatization were: (1) the restitution of property to former owners (this applies only to property existing before nationalization); (2) direct sales of state property, either to domestic or foreign owners; (3) MEBOs; (4) free distribution through a voucher system; or (5) a combination of these strategies (Andreff Reference Andreff2005). Poland largely chose direct sales, with some voucher privatization to legitimate the process (Stark and Bruszt Reference Stark and Bruszt1998), the creation of national investment funds to inject capital (Błaszczyk et al. Reference Błaszczyk, Hashi, Radygin and Woodward2003), and some MEBOs (Svejnar Reference Svejnar2002).

Moreover, privatization proceeded slowly. Indeed, despite being hailed as an example of the success of neoliberal reform, Poland actually proceeded more slowly with regard to the overall reduction of the state sector than did countries such as the Czech Republic (Stark and Bruszt Reference Stark and Bruszt1998). It even lagged behind Hungary, often cited as an example of gradualism, as late as 2000. Progress was halting and largely marred by political infighting and the consciousness that privatized property would be valuable in future political contests. Privatization in Poland, as elsewhere, was also marked by political manipulation. Great lengths were taken by Polish state officials to create politicized spheres of property: firms were privatized to domestic business groups in exchange for future benefits in the form of campaign contributions to political parties. As a former minister of privatization, Janusz Lewandowski, said, “The government has frequently used words like ‘national’ or ‘Polish’ in consolidating state assets in the sugar, power or shipbuilding industries. In the end, however, ‘national’ often turns out to mean ‘partisan’” (Polish News Bulletin 2004). Businesspeople also spoke of the need to shield national entrepreneurs from foreign pressure – a discourse that resonated with broad nationalist sentiments already in the first decade of transition. For example, one business leader, asked to identify priorities for economic policy, stated, “The government needs a system of supporting business – a system of financing, a system of supporting Polish owners [emphasis added].”

Bank restructurings in particular were subject to politicization because of the emphasis on workouts rather than liquidation, as described by McDermott (Reference McDermott2007), and the rejection of bank sale by distributing vouchers to the general public (Balcerowicz and Bratkowski Reference Balcerowicz and Bratkowski2001). At the same time, large privatizations were used as a means of plugging holes in the budget and reducing liabilities for the state. Addressing budgetary shortfalls is a common element of most privatization processes, but the combination of workouts, domestic favoritism, gradual pace, and political competition created ample opportunities for the entrance of politics into the process in Poland.

The system of corporate governance further enforced these trends. Poland adopted a two-level system of corporate governance. This structure was chosen because supervisory boards would act as state agents, doing what was known in Poland as “sanitizing” (bringing to a healthy state) firms without political interference. In practice, this process was heavily politicized (Jarosz Reference Jarosz2001: 47), with the supervisory boards often staffed by political insiders loyal to the then minister of the Treasury (Grzeszak et al. Reference Grzeszak, Markiewicz, Dziadul, Wilczak, Urbanek, Mojkowski and Pokojska1999).

Finally, Poland’s early governments were reluctant to accept foreign ownership, to the point that one early privatization minister stated that he had created as many obstacles as possible to foreign purchases of Polish companies in order to encourage a class of domestic owners (Stark and Bruszt Reference Stark and Bruszt1998; Schoenman Reference Schoenman2005). This last position reinforced the politicization of Polish business.

Altogether, the Polish government’s policy of economic transformation amounted to an attempt to manage the slow combination of private market forces with state intervention in order to retain both political and policy influence. After 1997 economic pressures led governments to look increasingly to foreign investors for injections of capital, but these were still managed and cautious attempts to attract investment without relinquishing control over economic development policy. Throughout, these moves increased the breadth of the network of ownership.

Banks

Banks and funds were a central part of the Polish transformation, due both to the level of state involvement and restructuring that took place instead of liquidation and to their role as anchors of the broader process of property transformation. In transition economies, the short supply of capital and the exigencies of rapid growth placed banks in a particularly important position. In Poland, however, it was debt/equity swaps that drove the initial ties with banks, rather than firm borrowing through credit.

As banks became key owners, they attracted foreign investment through the privatization process. In addition, Poland’s privatization policy established fifteen closed-ended national investment funds (NFIs in Polish), which became publicly listed companies. Ownership of these funds was transferred to the public through vouchers that were convertible into shares, with the NFIs accounting for 60 percent of the shares of 500 state-owned firms slated for privatization (Dzierzanowski and Tamowicz Reference Dzierzanowski and Tamowicz2003).4

In Poland, the banking system privatization began in 1992. At the same time, before 1995, a number of small private banks appeared as a result of a liberal licensing regime that came into effect with the banking law of 1989. Many of these ended in failure, with some generating spectacular scandals. As a result, the Polish government changed the licensing policy in 1992 and ended the period when solely domestic banks were being founded (Balcerowicz and Bratkowski Reference Balcerowicz and Bratkowski2001: 13). The state also chose to privatize some large state-owned banks to Western firms (Svejnar Reference Svejnar2002: 7). The Polish process was eclectic, however, shifting over time between initial public offerings (IPOs), minority stakes, and tender offerings from strategic investors (Bonin and Wachtel Reference Bonin and Wachtel1999).

The privatization of banks can be divided into two periods. The first, lasting from 1992 to 1997, was a period of halting progress. In March 1991 the initial program of bank privatization was approved. This foresaw a period in which nine commercial banks would be “commercialized,” meaning that their legal form would change from that of state bank to joint-stock company, thus preparing them for privatization. The intention was to privatize these nine commercial banks quickly, with the goal of two to three per year until 1996 (Balcerowicz and Bratkowski Reference Balcerowicz and Bratkowski2001). Banks with specialized functions, such as Bank Handlowy SA, PKO BP, and PEKAO SA, would be held for privatization after 1996.

The privatization process did not start properly until 1993. This delay was caused by the poor financial condition of these state-owned banks. In 1991 the government decided to postpone the privatization and to deal with banks’ bad debt portfolios first. In order to do so, some foreign investment was permitted under the condition that it be used to restructure existing small banks in distress. In total, fourteen banks were granted such licenses from 1993 to 1997. Simultaneously, large banks faced a mounting crisis, as their holdings of unrecoverable credits rose from 9 percent to 20 percent in 1990, and by June 1992 they accounted for between 24 and 68 percent of all bank loans (Balcerowicz and Bratkowski Reference Balcerowicz and Bratkowski2001). Against international advice about how to deal with this problem, Poland also undertook a decentralized approach to restructuring both banks and enterprises, with the former leading the way (Kawalec Reference Kawalec1994; Balcerowicz and Bratkowski Reference Balcerowicz and Bratkowski2001). Largely, this was done because of skepticism about the ability of a centralized restructuring agency to resist political pressure, and a belief that bad debt workouts would be most effective if they were initiated and negotiated by the banks themselves. As a result, the “Enterprise and Bank Financial Restructuring Program,” approved by the Polish parliament in 1993, set up a system of incentives so that recapitalized state-owned banks could write off unrecoverable loans and take action against bad debtors. The banks themselves were recapitalized with an issue of state Treasury bonds that obliged restructuring. The argument in favor of this policy maintained that it would simultaneously lead the restructuring of debtor firms and encourage privatization via debt/equity swaps (Belka and Krajewska Reference Belka and Krajewska1997), transforming banks into key national holders of firm equity. This move established banks as the hubs (owners) of large networks of firms, promoting the emergence of broad firm networks.

In April 1993 Wielkopolski Bank Kredytowy (WBK) was privatized, followed by Bank Slaski (BSK) in early 1994. Both banks were sold via IPO, and in both cases a foreign strategic investor became a shareholder (the EBRD and ING, respectively). Yet the strategic investors’ share in stock was limited to 28.5 percent in the former and 25.9 percent in the latter, and the state Treasury retained a vast share in equity (44.3 percent in WBK, 33.16 percent in BSK). As a result, the privatization of these two banks was far from complete, but the initial goal – injecting foreign capital without relinquishing control to foreigners – had been achieved.

In January 1995 a third commercial bank, Bank Przemyslowo-Handlowy (BPH), was sold via a public offering. Because of limited demand, however, the EBRD took over 15.06 percent of the shares according to an underwriting contract, and more than 48 percent of the shares remained with the state Treasury. In December 1995 the fourth commercial bank, Bank Gdanski, was privatized via IPO. Another domestic bank, Bank Inicjatyw Gospodarczych (BIG) (established in 1989 with the former Polish president, Aleksander Kwasniewski, as one of three partners), turned out to be the biggest investor. Together with its subsidiaries, BIG purchased 26.75 percent of the shares. Another 25.1 percent of shares were sold to foreign investors. In the case of Bank Gdanski, 39.94 percent of shares remained with the state Treasury. Thus, by the end of 1995, only four banks had been partially privatized.

Between 1995 and 1997 a period of bank reform took over the push to privatize, driven by the idea that Polish banks were too small and too weak to be competitive. Hence, it was argued, they should be reformed and strengthened through mergers, and only afterward privatized (Sikora Reference Sikora1996; Balcerowicz and Bratkowski Reference Balcerowicz and Bratkowski2001). As mentioned above, the shift in philosophy also reflected a strong dislike of foreign capital by some political parties and a desire to keep banks in national hands (Balcerowicz and Bratkowski Reference Balcerowicz and Bratkowski2001). It was this approach to workouts that sustained many of the state-owned banks (McDermott Reference McDermott2007). At the same time, this route led to a dispersed ownership structure that privileged insiders in the management of the firm after privatization.

While a plan to reorganize and strengthen banks was being developed, two banks, Powszechny Bank Kredytowy (PBK) (one of the nine state-owned commercial banks) and Bank Handlowy, worked out their own privatization plans and successfully pressed for their acceptance by the government. In the first half of 1997 both plans were realized. In the former, the state retained over 50 percent of the shares, operating largely as a passive owner, with the bank management playing the ownership role. Bank Handlowy was privatized to three foreign investors (26 percent), with the remaining shares sold via IPO (59 percent) and the state retaining 28 percent of shares but only 8 percent of votes. According to Balcerowicz and Bratkowski (Reference Balcerowicz and Bratkowski2001), this was an even more sophisticated form of insider privatization, after which the state Treasury had little power, the ownership was dispersed, and bank management governed the bank.

Throughout these initial phases of transformation, the dominant concern was to improve the condition of banks, establish them as key holders of capital, and resist the loss of control to foreigners. The return to power in 1997 of the right-wing coalition of parties affiliated with Solidarity, the Solidarity Electoral Action (AWS), brought about yet another shift in bank privatization, with the minister of the Treasury proposing sale to foreign investors and speeding up the pace of privatization. Despite broad opposition in parliament, and even from within the governing coalition, to the strategy, the remaining state-owned commercial banks and two other large banks were privatized (Balcerowicz and Bratkowski Reference Balcerowicz and Bratkowski2001: 27). Three state-owned commercial banks (BDK, PBG, PBKS) and PEKAO were merged in 1998. Fifteen percent of the resulting Bank PEKAO was sold by IPO in that year, and a 52 percent stake was sold to Allianz Capital and Unicredito Italiano in 1999. The latter was the largest capital transaction in the history of Polish privatization (Dzierwa Reference Dzierwa1999). During the same year 80 percent of the last state-owned commercial bank, Bank Zachodni, was sold to Allied Irish Bank.

At this point, only two large fully state-owned banks remained, and they would soon also come up for sale. In Reference Ikstens, Smilov and Walecki2001 40 percent of the ailing PKO BP was sold via the stock market to domestic institutional investors (13.2 percent), 8.5 percent to foreign institutions, and 16 percent to domestic individuals, with 51.5 percent remaining in state hands. Lastly, 40 percent of the cooperative bank BGZ was sold to a private Polish bank, leaving 43 percent in the hands of the state Treasury.

Although this last phase shifted away from the initial focus of privatization strategy, the overall approach did much more than simply heed external pressure to privatize. An innovative approach to privatization and ownership restructuring established banks as key owners, held by a combination of the state, domestic private investors, and foreign stakeholders in an uneasy strategic alliance. In other words, successive Polish governments did not simply heed the external injunction to privatize at all costs. By navigating this complicated path of banking sector restructuring, banks came to occupy a defining place in the emergent Polish market economy. Through debt/equity swaps and restructuring, banks became major shareholders among the largest firms in the Polish economy, creating a broad web of cross-holdings that persisted long after privatization. Moreover, because of the strategy of gradual privatization, an emphasis on restructuring, and a program of avoiding sale to foreign investors, many banks retained a significant share of state ownership, creating still-prominent finance-based links between industrial firms and the state. Such ties serve to reassure firms that governments will maintain their commitment to a particular policy, because the latter signal that they are willing to retain residual risk (Perotti Reference Perotti1995: 848). The strategy of developing ties between banks, the state, and other firms allowed Polish governments to make a credible commitment to investors about the direction of future policy choice. These ties also aligned interests to the extent possible among such diverse stakeholders.

Business groups

Alongside banks, Polish industrial groups formed early in the process of transition, often the creations of emergent large entrepreneurs such as Aleksander Gudzowaty, Zygmunt Solorz-Zak, and Jan Kulczyk. As in much of the post-socialist world, these businesspeople were responding to opportunities in the privatization process, and they tended not to focus on a particular sector, but they were closely allied to a political party. For example, the group of firms belonging to Gudzowaty, who vied for the title of wealthiest man in Poland, developed out of an opportunity to control and obtain a mediation fee on the transit and import of natural gas to Poland. The group later developed, however, to include a joint insurance venture with CIGNA, develop biofuels that were subject to government subsidy, and build a high-speed telecommunications backbone.

Gudzowaty was closely allied to the left-wing SLD and suffered when the right-wing post-Solidarity coalitions came to power. He was similarly threatened when the Law and Justice Party emerged to take power in 2005. Although it is commonly believed that many socialist-era managers and bureaucrats became wealthy by taking advantage of long-standing contacts with the leftist politicians elected after 1989, in Poland politicians on the right also took advantage of ties to business and cultivated a coterie of closely allied businesspeople. For example, Solorz-Zak, the owner of a satellite television network, was closely tied to center-right coalitions and was able to obtain broadcasting licenses through political contacts. Kulczyk had been involved in the import of German automobiles to Poland since the 1980s, and he controls a group of firms that has been involved in the building of highways across Poland. He was also similarly seen as close to the post-Solidarity coalition. McMenamin and Schoenman (Reference McMenamin and Schoenman2007) find that these businesspeople tended to have relationships with either one or the other political option over time. In fact, throughout the 1990s and until 2005 two loose business coalitions existed, alternating in power and jockeying for advantages when their political allies were in office. The fact that businesspeople tended to hold ties to one side of the political spectrum set up a complex structure that allowed business and political actors to develop long-term relationships.

Romania’s path to privatization: a redistribution of assets to political clients

The Romanian case offers a second path. Here, ownership networks were narrow, and uncertainty was low. Firms had no way to coordinate, as they did not have the broad links that Polish firms could use to share information and mobilize for cooperation. Early post-1989 governments in Romania delayed reform questions, opting in favor of a gradualist approach that was preferred by managers and in the interest of the new political class. Although they began to put the infrastructure of privatization in place by 1991 with the passage of the first mass privatization law, only 260 companies were privatized by 1993, and 92 percent of these were small firms (those with fewer than fifty employees). Only two of the 708 larger companies on a 1990 list of firms to be privatized were actually sold by the end of 1993 (Roper Reference Roper2000: 95). This was a very small number compared to the overall task of privatization. More importantly, the National Salvation Front – a broad coalition of caretakers dominated by transformed members of the Communist Party elite emerging from the second circle around the former dictator, Nicolae Ceausescu – was firmly in control of government.

Hence, privatization took on the form of redistribution to constituents and insiders. Highlighting the flaws of the process in an interview, one official concluded, “It was a fake process of wealth creation by spoiling state property.” The majority of firms that were privatized were actually transformed into joint-stock companies by distributing 70 percent of their capital to state ownership funds and the remaining 30 percent to the private ownership funds that were, formally, owned by the public (Roper Reference Roper2000: 91; Earle and Telegdy Reference Earle and Telegdy2002: 661; Grahovac Reference Grahovac2004: 28, 68). The public received certificates that could be used to purchase the tranche owned by the private ownership funds, thus linking private shareholders with state ownership. This is important in terms of the creation of the network of ownership, because it diluted ownership, granting public participation to a limited extent but without bringing about privatization in any meaningful way (Grahovac Reference Grahovac2004: 28). Further, according to Earle and Telegdy (Reference Earle and Telegdy2002: 661), the private ownership funds remained state-governed, with government-appointed directors who were approved by parliament, and effectively no way for the public to exercise control.

Moreover, all other state-owned enterprises (SOEs) were turned into so-called regies autonomes (RAs), which remained under state ownership and were overseen by the Ministry of Finance. The 450 companies that became RAs were utilities, natural monopolies, or other companies of sufficient interest or importance that they could be deemed “strategic.” The precise motives for placing companies into this group is unclear (Earle and Telegdy Reference Earle and Telegdy1998a). With 450 companies in this group, however, it seems likely that the strategic nature of some firms was largely a function of the number of jobs they provided or the income they generated for political interests. Thus, the strategic discourse became an excuse to shield companies from privatization until an unspecified later date. Within this context, the privatization program began under a dark cloud. The state ownership funds rarely offered shares in the best companies, and those that represented politically powerful constituencies were sheltered from privatization and allowed to continue operating under a deficit (Ahrend and Oliveira Martins Reference Ahrend and Oliveira Martins2003: 333).

By 1992, after numerous splits within the NSF that brought a faction known as the Party of Social Democracy of Romania to power, the government recognized that the economic situation required a reorientation in economic policy and enacted a strategy of price liberalization, wage stabilization, and austerity combined with increased export concessions. The hope of the government of Theodor Stolojan, who replaced Petre Roman as prime minister, was that industries would be able to increase their exports and reduce the large trade deficit, offsetting the difficulties associated with austerity measures. The companies that were encouraged to export did not produce goods that could be sold on the world market, however, and required increasing energy imports, which the government subsidized (Roper Reference Roper2000: 92; Ahrend and Oliveira Martins Reference Ahrend and Oliveira Martins2003: 337). The move was also meant to redirect trade from former Council for Mutual Economic Assistance countries toward the European Union. Although EU trade increased, imports from Europe also rose drastically. According to Daniel Daianu, former minister of the economy, the weak results of the election that brought Stolojan to power over factional rivals prevented the government from pursuing real export-led growth tactics (Roper Reference Roper2000: 93).

Reform continued but took on a stop-go character. In 1995 new measures were introduced to limit inflation, then rescinded after several months, largely as a result of complaints from political constituencies. Government subsidies to the industrial sector persisted. By 1995 only 25 percent of commercial companies identified in 1990, and only 8 percent of large SOEs, had been privatized (Economist Intelligence Unit [EIU] 2001).

Serious economic problems ensued, leading to the creation of another mass privatization program (MPP) in mid-1995. Vouchers were again distributed to the public, but it took until May 1996 for 93 percent of the vouchers to be exchanged for shares. Moreover, this method introduced no new capital into the industries, and none of the important RAs were part of the second MPP. This move also made the network even more disconnected (Earle and Telegdy Reference Earle and Telegdy1998b).

The victory of the opposition leader Victor Ciorbea, head of the Christian Democratic National Peasants’ Party, in 1996 – an isolated instance of protest voting against the poor economic policies of Stolojan – created the chance for a new era of Romanian economic reform. The government passed a set of reforms that gained the confidence of the International Monetary Fund (IMF) and secured a new loan package. The other members of the new Romanian Democratic Convention (CDR) coalition, however, the Union of Social Democrats (USD) and the Democratic Party (PD), opposed many of the reforms promised in the IMF agreements. For example, the USD and PD were closely allied with business interests that rejected the elimination of subsidies to industry (Roper Reference Roper2006). It would also have been difficult to interrupt the supply of credits to industry by banks, a sector that had not begun to privatize. The entrenched interests in the banks and ministries worked to prevent the government from making any progress on the restructuring of firms (Roper Reference Roper2000: 92).

In the end, the Ciorbea government was unable to maintain the pace of reform. Many SOEs were placed on the closure list and then never closed (Roper Reference Roper2000: 102). The same was true of companies slated for privatization. Disagreements continued between Ciorbea and Roman’s USD. The narrowly constructed economic networks allied with the opposition helped prevent any progress in the construction of a new economic framework during this brief window of opportunity. The failure of this potential new force in Romanian politics paved the way for an end to Ciorbea’s short and ineffective disruption of one-party dominance.

The conflicts that had existed during the Ciorbea government continued with the successor government of Radu Vasile, organized under the umbrella of a political alternative. Roman and his political allies from the previous era had little interest in promoting economic reform because of pressure from interest groups allied with the USD. The miners, a potent force that could be brought in to riot in Bucharest, also continued to play a role in Romanian politics. After several violent outbreaks, Vasile’s government came to an undisclosed agreement with the miners’ union, which allegedly postponed or revoked the closure of two mines and brought financial benefits to the miners. Even in such devastated sectors, reform seemed nearly impossible. Ultimately, Vasile’s government was short-lived. Ion Iliescu, the leader of the NSF/PDSR (now renamed the PSD), returned to power by capitalizing on the failures of the Ciorbea government – failures that were largely a consequence of PDSR obstruction.

Business groups

In this context of stalled reform and the lack of a clear political break with the past, two groups came to dominate: industrial state-owned firms, which had preferential access to resources and the state budget, as well as the ability to influence legislation; and an emerging wealthy elite that was drawn mostly from the ranks of the military and the former security service, the Securitate. Both set about creating a hierarchical ownership structure that was well adapted to Romanian politics.

Many currently prominent businesspeople allegedly owe their success to their experiences abroad before 1989 and access to bank accounts belonging to the Ceausescus. Given these political ties, their firms sought the protection of and links to the NSF/PSD. The dominance of the PSD, however, meant that these alliances failed to provide the security that firms sought, because business owners depended more on the PSD than it depended on them. The Paunescu brothers, among the wealthiest Romanians and allies of the PSD, were forced to move their business abroad in order to avoid investigation with regard to a banking scandal under the PSD. They were forced to leave Romania themselves during the period of the CDR government for fear of prosecution. Emblematic of the dominant position of the PSD and the insecurity it brought to wealthy businesspeople, the extremely wealthy formed their own small parties that acted in coalition with the PSD in order to provide the degree of security that comes with political prominence. For example, Dan Voiculescu, president of the Grivco group, is also the founder of the Humanist Party, which was a member of the ruling PSD coalition. Gigi Becali, a beneficiary of insider land deals with the Romanian army, founded the ultra-nationalist New Generation party for the same reason.

Even those businesspeople whose success was allegedly tied to the CDR, such as Ioan Niculae, were ultimately forced to negotiate better relations with the PSD. Niculae’s business began acquisitions during the CDR government, particularly in the period 1996 to 1998. Predictably, Niculae was faced with a series of investigations when the PSD returned to power in Reference Ikstens, Smilov and Walecki2001, related to various acquisitions of privatized property that occurred under the CDR. According to insiders, after some negotiations he managed to improve his relations with the PSD leadership and, in particular, with the influential PSD minister of privatization, Ovidiu Musetescu, and he obtained a majority share in the tobacco company SN Tutunul Romanesc.

In the absence of noteworthy political opposition, firms did not create deep and stable ties with the PSD. Business and the Social Democrats exchanged goods when opportune, rather than operating as identified clients. Thus, none of my informants felt comfortable identifying more than very few firms as “clients of the Social Democrats” or any other party. Pasti (Reference Pasti1997) describes the situation: “Ties with the state are retained through managerial links with high-placed government officials and the prominence of governmental privatization agencies in shareholding. The network between ministries, central departments and large enterprise managers has also reproduced itself. The laws seeking to undo these ties were constantly opposed by ministries and enterprise managers.” A Cabinet member summed this up when he stated that Romania’s leaders “do not want privatization – they want assets for themselves so they can supply their parties with money” (Pasti Reference Pasti1997, cited by Stan Reference Stan2003: 15). This was a dramatically different and much more direct approach compared to the way that politicians formed relations with firms in Poland.

This result reflects the general failure of the government to outline a decisive privatization plan: “Instead of creating the new bourgeoisie, privatization allowed the nomenklatura to obtain de jure ownership rights of assets it already de facto controlled” (Stan Reference Stan2003: 13; italics in original). In other words, it did little to broaden connections between economic actors while doing much to strengthen the narrow, hierarchical nature of ties between the Social Democrats and firms, often by establishing direct party control of firms.

Bulgaria’s path to privatization: the state struggles to control firms

In Bulgaria, ownership networks developed quite differently from how they did in Poland and Romania. First, because of political infighting, there was an inability to commit to a policy of privatization. In this context of political chaos, and because of it, groups of insiders became institutionalized as economic stakeholders and gained an inordinate amount of influence. These insiders even attempted to coordinate so as to prevent the entrance of foreign business. Although banks were politically prominent initially, the spectacular bank failures during the financial crisis of the late 1990s – itself caused by insider dealings – removed them as a viable organizing pole. The network of firms that developed was ultimately narrow in structure.

Privatization in Bulgaria took place under a mix of direct privatizations and voucher privatization. The latter, like most voucher programs, was intended to speed up the process and attract local participation (Prohaski Reference Prohaski1998). The Bulgarian state lost control of the process of economic transformation soon after Decree 56, passed in 1989, allowed for the limited creation of private firms and gave SOEs some autonomy. These were the basic preconditions for the emergence of a private sector that had parasitic relations with the now more autonomous SOEs, given the political context. Radical decentralization of the state banking sector, in combination with liberal licensing policies for private banks, assisted the emergence of large conglomerates of questionable origin.

Efforts at limiting these trends produced weak results. Attempts in 1991 by the then finance minister, Ivan Kostov, failed to reel in the more influential economic agents, who continued to enjoy access to credit. The Privatization Act was passed by the Bulgarian parliament in 1992, allowing privatization of state-owned enterprises to move forward. After February 1993, when the first SOE was privatized, privatization gradually gained momentum.

Proponents of privatization faced serious opposition from entrenched groups, such as SOE managers, government officials, and large banks. State officials, not surprisingly, were generally unwilling to give up their ability to reap personal rewards from the situation. Thus, until 1996 only small privatizations were successful, and practically no progress was made on the privatization of large industry. The situation of enlarged bad debt finally led to massive bank failures in 1996 and stricter conditionality from the IMF, to the point that it became the main factor in the collapse of Zhan Videnov’s socialist government in 1997. A currency board was subsequently put in place, effectively eliminating the possibility of central bank lending.

Bulgaria was also the first country in which the socialists were re-elected to power, in 1994, and it was not until 1997 that a full mandate was given to nonsocialists. The re-election of the Bulgarian Socialist Party (BSP) was taken as a U-turn away from the transition. This gives a sense of the political and ideological tension that emerged in Bulgaria after 1989. In addition, there were widespread allegations of clientele-favoring behavior against the center-right Union of Democratic Forces (UDF) (Stanchev Reference Stanchev1999). Even during the center-right UDF government of Kostov (1997–2001), often assessed as the first government committed to making difficult but unpopular policy choices associated with economic reform, preferential privatizations continued to take place (Stanchev Reference Stanchev1999). An official noted in an interview that this was the product of a broader vision and tolerance for political wealth creation: “There was a popular slogan at the beginning among UDF members: we want to create the blue [right-wing] bourgeoisie, not the red [left-wing] bourgeoisie. But when this happens only by corruption, it creates a corrupt bourgeoisie. It’s very much the official policy of the party and it was defended as appropriate because the Socialists also created their bourgeoisie.”

Throughout the transition period, Bulgarian politics has been marked by the strong influence of economic interests – a dynamic that did not fail to attract the ire of the electorate. Bulgarian frustration with the lack of state capacity and the influence of powerful figures in the economy created a window of opportunity for the return of the former tsar Simeon II, who had been in exile since 1946. Having left Bulgaria as a young boy and worked in finance in Spain, Simeon was seen as a political outsider who would, it was hoped, be able to bring together a group of young professionals with foreign work experience and few ties to the existing networks.

Even Simeon’s government had difficulty sidestepping existing social structures, however. According to political scientist Ognyan Minchev, speaking on Radio Free Europe/Radio Liberty on April 3, 2002, the government of the former tsar (2001–2005) and the new party he created for the Reference Ikstens, Smilov and Walecki2001 election, the National Movement Simeon II (SNM), faced the problem of legislators who did not “work in the interest of the state, but act[ed] as lobbyists for business interests or even on behalf of business groups linked to organized crime, which flourishes under a fragile, powerless government.” In an interview, an official observed, “Big business is happy under SNM because, even though they started as thieves, the new government does not interfere. We cannot get rid of the criminals.”

Business groups and insiders

Business groups and insiders have been a key group of economic actors in Bulgaria since 1989. Until the economic collapse in Bulgaria, semi-criminal business groups with names such as VIS-2, SIC, and 777 dominated the country, struggling to take control of industry, banks, and tourist infrastructure along the Black Sea coast. They represented a dynamic of entrepreneurship that privileged those with access to coercion. In a slow and often brutal process, these groups began to consolidate their hold on regions and certain industries. After gaining regional power, they sought to link regional groups into national players. VIS-2 was one such group, involved in the selling of car insurance and private security; it also controlled a large number of car thieves. Over time, VIS-2 and its leader, Vasil Iliev, managed to co-opt regional groups, and it became the first national-level “business group” that straddled the boundary between legal and illegal activities. The emergence of such large players eventually created a demand for business organizations to attempt to influence politics and obtain preferential policy. The first of these, known as the “Group of Thirteen,” emerged as a lobbying organization in 1993 and dominated the private sector until 1995 (Synovitz Reference Synovitz1996). This group, including subsidiaries, consisted of the largest banks, insurance companies, stock exchanges, large trading companies, newspapers, and private security firms. An official pointed out, however, “Within the G-13 there is no clean businessman because it was generated in a period of semi-chaotic economic rules. For example, one of the most influential, Orel Corporation, he is a wrestler [sic] and was connected to the counterintelligence.” Another official noted, “If you start to investigate the way that those people got their wealth, you simply would not find information about it. These barons are like a parallel state.” The group was formed to protect Bulgaria from the entrance of foreign firms so that member firms could position themselves for big profits. The G-13 did not collaborate with political actors, as firms and business organizations in Poland sought to do.

The lack of an alliance between business leaders and political actors was due partly to the internal dynamic of the group and partly to the difficulty of identifying viable partners for cooperation. The G-13 operated through its own business organization, the Confederation of Bulgarian Industrialists. In 1994 this grouping began to fracture when the chairman, Emil Kyulev (assassinated in 2006), criticized the most powerful company in the group, Multigroup (its chairman, Ilya Pavlov, a former wrestler, was assassinated in Reference Ikstens, Smilov and Walecki2001), for “aggressive and non-market expansion using the Confederation as a cover” (Finance East Europe 1994). Kyulev’s bank, Tourist Sports Bank, left the confederation, and he was dismissed as its chairman when the meeting ended. The powerful group TRON and its president, Krassimir Stoichev, also left at this time. It was more likely, however, that the conflict was over competing bids that group members had made for the purchase of debts owed by Kremikovtsi, Bulgaria’s largest steel and iron works, and Chimco, Bulgaria’s largest producer of urea, to Bulgargas.

Another force that was tearing apart the G-13 was the growing interest of some of its members in conducting business with foreign investors in Bulgaria. This was in conflict with the central purpose of the confederation, which was to obstruct the entry of foreign investors. In fact, the Bulgarian Investors Business Association (BIBA), an organization formed in 1992 to represent the interests of foreign investors, accused the confederation of supporting economically nationalist policies. A clear illustration of the inability of Bulgarian business to collaborate is offered by the duplicitous behavior of Stoichev and his group TRON, which was engaged in a Mobiltel venture that included Siemens and US West as foreign partners. Stoichev was thus going counter to the platform of his organization, G-13, and he approached BIBA. Such individual defections reflected the inability of business to develop and implement a larger framework and longer-term goals, as achieved by its Polish counterpart.

In addition to these dynamics, the Russian financial crisis had a strong effect on the Bulgarian economy. By late 1996 the nine largest banks in Bulgaria had become insolvent. The initial collapse began because the lynchpins of the system, oligarch banks, were failing due to mounting bad debt, which landed some of the directors of the large conglomerates in jail. The grouping of early business leaders that effectively functioned as a parallel state was under siege, and the early winners were rapidly becoming losers because their overindulgent greediness prevented the accumulation of lasting benefits. This first stage of rapid accumulation and then bankruptcy occurred because these firms had inside access to power brokers. The critical choice that many of the leaders of these groups made, responding to political volatility in Bulgaria, was to focus on short-term profits and asset stripping instead of building an organization based on synergies with state leaders.

In fact, the political influence that the G-13 did enjoy ended with the election of Zhan Videnov as prime minister in January 1995, partly because Videnov allegedly wanted to create his own group of firms using contacts in a group called Orion. Commenting on Videnov’s approach, an official observed, “Zhan Videnov ended up complaining publicly about the absolute egoism of business leaders. And he was disappointed by the so-called ‘red bourgeoisie’ because it didn’t support him at all. They just made their business at the expense of the state and carried it out without consideration of the political interests. The so-called allegiance of business to parties did not materialize.” His consequent attempt to create a new elite established a conflict between the G-13 group, particularly Pavlov and Multigroup, and Videnov’s government. In 1996 the downfall of the oligarchs “left Bulgaria in shambles,” with “little national wealth, virtually no middle class and no entrepreneurial elite – only ‘a mafia network thirsty for new victims’ and an impoverished population that questions the merits of democracy” (Synovitz Reference Synovitz1996).

National investment funds

At the same time as the oligarchs were facing their first stumble in 1996, Videnov’s socialist government embarked on a privatization plan that aimed to shift away from domination of the oligarchs and promote the return of political actors. In contrast to the popular Czech model, the Bulgarian government decided to create a series of investment companies that would function as funds for mass privatization (Prohaska Reference Prohaska2002: 3). The intention of this program was to prepare particular sectors for privatization by gathering companies related by sector under one umbrella corporation in the form of a physical or legal person. The method was to create investment funds that functioned in a semi-autonomous fashion. This differed from the Polish and Romanian models, in which the state retained the leading role in the guidance of funds. The main purpose of the funds was to act as an intermediary between enterprises and the investing public. The funds themselves were similar to holding companies, except that they were created with the intention of operating as investment funds. This created a strange hybrid structure, with serious implications for the power structure within the economy.

The move to privatize began in 1996, when eighty-one privatization funds out of 141 applicants obtained licenses from the Securities and Stock Exchange Commission (Prohaska Reference Prohaska2002). The majority of the funds directed their investment strategy toward a specific enterprise or sector, while about thirty of the funds were regional. This was a contradiction in logic of the goal of reducing the risk of these investments, but it led to the hierarchical integration of firms within a particular industry. The initiative for setting up such funds came from the managers of the enterprises on the mass privatization list or from the joint initiative of local government representatives and local business elites.

Once the UDF had returned to power in 1997 under Kostov, the situation changed dramatically. Interviews indicate that the socialists did not manage to profit from the experience of voucher privatization because they had little influence over who ended up acquiring the vouchers and because they presided over the process for too short a time once it started. Once the UDF had gained control of the government, however, it began to privatize companies that were performing well to investors allied with the party. These privatizations were allegedly reserved for investors who made donations to party-allied foundations. One such foundation, the Future of Bulgaria, was headed by Elena Kostova, the wife of the prime minister (Standart 2001).

Once the mass privatization program was in place, the UDF deployed another scheme, to introduce management–worker partnerships (known as RMDs) in the remaining companies. The UDF government managed to change the directorates of a large number of companies. The newly installed directors were party allies or top members of the party, and often these firms were sold to the RMDs. According to an analyst, this further entrenched corruption in Bulgaria: “The UDF was selling to the local UDF members, who were privileged in buying. This was a form of appropriation of state assets for funny money. When nothing happened to the leaders and this was the main scheme of privatization, political corruption became the model.” Many of these firms faced bankruptcy after the UDF lost power, and were not converted into a long-term source of income. Thus, although the process of privatization was politicized, it failed to convert firms into sources of political revenue or to connect political and economic actors in mutually beneficial exchanges.

Struggles for direct control: Bulgartabac, Bulgargas, and the National Electric Company

How these struggles played out is illustrated in the case of Bulgartabac, which highlights the difficulty of establishing networked alliances that link political and economic actors. One alternative in Bulgaria was for political actors to try to retain direct control of property, although this reached an absurd extreme with cases of management by the prime minister, who feared the dangers of delegation. The emergence of the monopolist group Bulgartabac represents the implementation of a broad strategy of firm development by the Bulgarian state. It is reportedly the largest tobacco company in central and eastern Europe, created by the linking of twenty-three subsidiary companies. The structure of the holding includes companies for tobacco buying and processing, the leaf trade, the manufacturing and export of cigarettes, and research and development. It is also a monopolist on the domestic market and the largest taxpayer in Bulgaria. Bulgartabac Holding was of significant structural importance for the Bulgarian economy, generating about 4 percent of budget revenues.

When formed in 1993, the holding had a 30 percent share in twenty-two factories, while the Ministry of Trade and Tourism held the remaining shares. The holding company did not interfere in the operation of the companies but functioned as a trading company, largely in conformity with the socialist model. This lasted until 1997, when it was argued that centralization of the tobacco industry would reduce internal competition and allow for better coordination of the constituent companies (Banker Daily 1997). Such a move was expected to increase the overall performance of the constituent companies, and the scheme was suggested by Bulgartabac’s supervisory board (Bulgarian News Agency [BTA] 1997).

Thus, on December 6, 1997, the state swapped its stake in the subsidiaries for an increased stake in the holding. This added a degree of separation between the state and day-to-day control of the subsidiaries, which now belonged to Bulgartabac Holding but reinforced the state’s control over Bulgartabac Holding.

This approach was seen as reducing the likelihood that the constituent companies would be sold off individually. In fact, the chairman of the supervisory board, Dako Michailov, strongly favored privatization through a foreign stock exchange (Banker Daily 1997). The strategy was widely seen as problematic, because only two of the twenty-two daughter companies, Sofia and Blagoevgrad, had attracted strong investor interest (Capital Weekly 1998b). By May 1998 any agreement on the strategy of privatization was still far off.

This was not only a move to restructure and strengthen the production and marketing capabilities of the tobacco industry. Until mid-1997 several companies, operating through two cigarette distributor associations that they had established, concluded preferential contracts with individual cigarette companies. One such company belonging to Multigroup, BT MG, had negotiated a sole distributorship with the former Bulgartabac bosses and the Blagoevgrad Bulgartabac factory. The two associations claimed to control 80 percent and 50 percent of the market, respectively (Capital Weekly 1998a). Thus, although the subsidiaries of Bulgartabac remained the property of the state, these firms were already operating together with the private sector for the benefit of the latter. This state–private partnership was different from the synergistic forms that emerged in Poland, however, and was more akin to asset stripping.

In this context, the new UDF government that took power in 1998 began to fight for control of Bulgartabac at general shareholder meetings (Mancheva Reference Mancheva1998). The new executive director of the Privatization Agency, Zakhari Zhelyazkov, announced his privatization strategy for 1999 and highlighted Bulgartabac as one of the key companies to be privatized, on a list that included the top companies in the country (BTA 1998c).

This was taken as a sign of a significant turnaround, and there was already talk of a “Bulgarian miracle” based on the UDF’s attempts to take on corruption and tackle the hyperinflation that had wrecked the economy (Emerging European Markets 1998). The UDF’s successes led to statements by the deputy prime minister and minister of industry, Aleksandur Bozhkov, that privatization would be complete by 1999 or 2000 (BTA 1998a; BTA 1998b). By May 1998, however, problems began to arise for the privatization process. In particular, there was widespread disagreement about the choice of an agent for the sale (BTA 1998a). Simultaneously, there was disagreement about whether shares should be sold in the holding company only or in the individual daughter companies. The leader of the Euroleft party, Alexander Tomov, strongly contested the latter strategy because he felt that it would destroy the strength of the sector in Bulgaria (Pari Daily 1998).

A further problem arose when the general meetings of shareholders in seventeen of the twenty-two daughter companies were suspended on May 8, 1998. Soon afterward the boards of directors were dismissed on the orders of the prime minister, Kostov, signaling a conflict between the government and the firms, which were insubordinate to the state (Viktorova Reference Viktorova1998).

This dynamic of insubordination illustrates the centrifugal forces working to disconnect state and firms in Bulgaria, and is in sharp contrast to the deployment of state bureaucrats and party faithful to corporate boards in Poland as a way of propagating policy preferences and keeping firms within the party system. In Bulgaria, the crackdown was an attempt by the government to consolidate a year of achievements in economic reform (Alexandrova Reference Alexandrova1998), and was accompanied by a host of other dismissals in leading state sector companies such as the National Electric Company (NEC) and Balkan Airlines. Among others, Georgi Kostov, the CEO of the Blagoevgrad Bulgartabac factory, which held 50 percent of the domestic market, was dismissed. Kostov had been appointed as a courtesy to Euroleft. As the conflict between Kostov, the prime minister (no relation), and Tomov, the Euroleft leader, developed, Georgi Kostov was removed, demonstrating the importance of controlling economic assets to political coalitions (Ilieva Reference Ilieva1998).

Throughout his tenure as CEO, Kostov remained in the executive leadership of Euroleft, and his dismissal consolidated the UDF’s hold over the powerful tobacco company. It also paved the way for Bulgartabac Holding’s plans to remove private distributors from the market and create a monopoly cigarette distribution company while simultaneously introducing a licensing regime to control wholesalers.

Herein the contrast with the Polish strategy, which relied on network ties for governance, can be seen. Alliances were so fragile in Bulgaria that, even at the level of prime minister, delegation was being undone in favor of direct control. This is an indicator of the extent to which alliances around even state property could not be forged. According to Capital Weekly, this particular sacking fit the pattern followed by all prime ministers: “In the beginning, they delegate powers to their [ministerial] teams. Then, frightened by the minister’s affinity for individual games, [they] start to concentrate power more and more in themselves. A good example is the management of monopoly companies. After two years Bulgaria is back to the ‘Prime minister-head of company model’” (Alexandrova Reference Alexandrova1998). Ivan Kostov himself said, “Officially, this model is explained with the need for the prime minister to personally control the management of individual commercial companies to make them more efficient and to halt corruption and shady dealings. The idea is to make it possible for the Cabinet to directly participate in the management of commercial companies and the distribution of the resources of key industries” (Alexandrova Reference Alexandrova1998). In a related move, in the summer of 1998 Kostov announced that he would take charge of the power industry, meaning that he would supervise the NEC, Bulgargas, coal mining, and the central heating supply companies.

This was not a dynamic established just during Kostov’s government. After taking office in February 1995, the socialist prime minister, Videnov, took over the state monopoly structures in the petroleum and gas delivery industries. When he encountered obstacles to the removal of the energy minister, Georgi Stoilov, because of opposition from coalition partners, he transformed the whole ministry into a government committee, allowing for staff changes without the approval of the parliament. Once this had been accomplished, Videnov put the NEC under the direct control of Ivan Shilyashki. One year later he decided to isolate Shilyashki and the deputy prime minister in charge of the power industry, Evgeni Bakurdzhiev, in order to establish direct control of the energy firms.